Two cases:

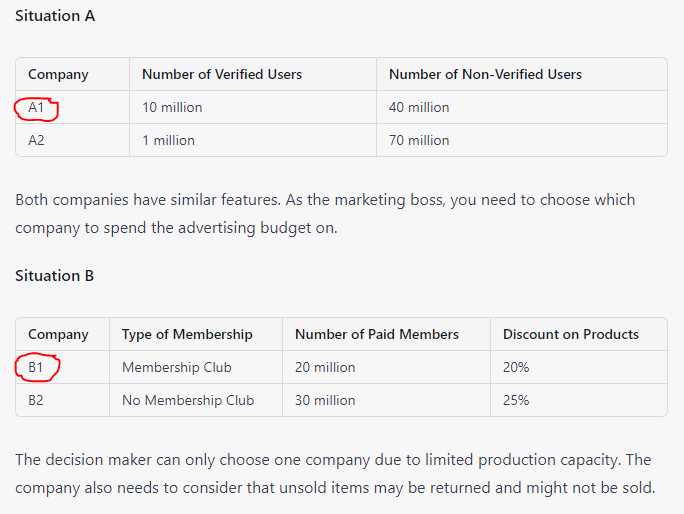

Case A: Company A’s chief marketing officer has to make a decision on how to spend a company’s advertising budget. Here are the two shortlisted companies, presented by her analysts. Company #A1 has 10 million verified and 40 million non-verified users. Company #A2 has 1 million verified and 70 non-verified users. Other indicators are similar.

Case B: Company B’s Head of Partnership has received two proposals from two companies, and each has offered final terms. The company can only pick one company due to its near-term production capacity. Company #B1 has a marketplace membership club where users pay to shop with associated benefits (like Amazon Prime) and is asking for 20% discount from Company B; total paid members are 20 million per annum. Company #B2 does not have any membership club but claims it reaches 30 million shoppers yearly, and is asking for 25% discount from Company B. Any item unsold is returned to Company B in both scenarios.

As we discuss Facebook’s decision to ask users to pay for verified badges, if you are the chief marketing officer, what would you do for Case A? Indeed, which one is a better deal to spend your ad money on?

I wrote about this when Elon Musk pioneered it, noting that it would be a good feature for Meta (Facebook parent company) and LinkedIn. Today, it has been adopted: “‘Meta Verified’ will give you a blue badge along with several other benefits, including increased visibility, protection against impersonation, priority customer support, and more” for $12/month.

For Case B, what would be your call considering that any unsold item is coming back and you’re unlikely to sell it.

In the WhatsApp Group sub-categories, discuss with others. During Tekedia Live on Saturday, we will spend a short time on this, and will examine the implications as we focus on this week’s module of Business Model and Strategy.

Note: Any variable or factor not included is assumed to be similar to Companies A1 and A2 and should be treated as non-factors. The same applies to Companies B1 and B2. What that means is this: they have similar credit rating, payment history, return ratios, etc. The only factors to consider for these distinct cases are those noted and their direct implied implications.

Source: extracted from Tekedia Mini-MBA courseware

Comment on Feed

Comment 1: A1 and B1. This sounds like we even try to do these things with Facebook ads when creating audiences and targeting. (e.g Engage shoppers and look-alike audiences.)

Comment 2: For Case A the advertising budget would go to Company hashtagA1 – it has 10 million verified and 40 million non-verified users, and the verified users are more likely to be genuine, active users who are more dedicated and interested in the company’s products or services. Also, having higher number of non-verified users may not necessarily translate into more ‘customers’.

For Case B I would partner with Company hashtagB1. Although having a smaller reach, its customer base is more committed with 20 million paid members. The committed members of the membership club could potentially increase odds that they will make purchases as they have already invested in the service. Also the 20% discount can be used as an incentive to retain those customers and hopefully attract new ones through time.

Great exercise Prof.

Comment 3: With the info given and given that every other indicators are similar for Case A, I am under the assumption that company A1 and company A2 have the same advertising budget.

For the same level of advertising budget, the better deal for case 1 would be company A2 for these reasons:

Non-verified users make up 0.07% of verified user compared to 400% for company A1. A2 has smaller target audience who are able and willing to pay for membership and make for lesser advertising stress and spending. The marketing agency gets to make more profit from company A2. This is when compared to running an advertising campaign for company A1 which has larger audience who may likely be unwilling to pay to be verified users and therefore require more thoughtful and high impact strategy which would be relatively more costly.

This is all assuming both companies are operating under similar budgets.

For Case B: A partnership with B1 is considered the best option compared to B2 for these reasons:

While B1 has only 20million members per annum compared to the 30million shoppers claimed by B2, those 20million are certain, so are the revenue per annum, unlike B2. Also, their discount rate of 20% seems more favorable.

My Response: great insight. Would your call on Case A change if the CMO works in Company A. In other works, there is no advertising agency. In other words, there is no middleman, referring to your “The marketing agency gets to make more profit from company A2.”

Also, for Case A, is there a consideration that being verified provides a small level of “certainty” (i.e. they are real accounts, not bots)? Thanks for the contribution.

Comment 4: Case A = #A1 has 50 million users ( 10 million verified users and 40 million non-verified users)

#A2 has 1,000,070 users (1 million verified users and 70 non verified users).

As a Chief Marketing Officer, I would ask my non verified users to verify their accounts by promising them some perks( for every verified account, the user gets 1$ bonus)

After I’ve got the users to verify their accounts. I would spend on users with more subscriptions.

Company #A1 is a better company to spend on because they have more subscribers/ users.

For Case B =

#B1 has a verified members with a credible platform .

#B2 doesn’t have a verified members and their claims are based on assumptions.

As the Head of Partnership for Company B, I would rather work with Company #B1 because of its production capacity, quality and credible products. “When you have a quality product, it reduces the risk of returning items back to the company .”

Comment 5: For case A, I will go with #A1 because 25% of the company’s users are verified. I’m certain that my products will be shown to at least 10 million persons.