Welcome to Tekedia Institute. We run an amazing business school which has attracted professionals and students from 39 countries. The next edition begins Monday, Sept 13, 2021. It is a great academic festival, and one that is nurturing a generation of leaders, innovators and change makers. Tekedia Mini-MBA is serving Africa through educating on the tenets of entrepreneurial capitalism.

Our Faculty members come from Microsoft, Shell, Flutterwave, Nigerian Breweries, Jobberman, Coca Cola, and other great organizations. Thrice weekly, I personally coordinate live Zoom sessions on the mechanics of business systems. We bring our Faculty and Guests on those sessions, covering industries and business domains.

Our impacts are huge because most young founders are passing through our program. Just today, I connected one with a Mastercard Director to further his vision.

The deadline for early registration with the huge benefits is today. It remains N50k naira or $140. REGISTER today and join us on Monday .

Not quite long after attaining unicorn status, Flutterwave is in the news again for good. The boisterous fintech company, that has taken the world of payment by storm, announced on Thursday it’s partnering with Africa’s largest network provider, the MTN Group, to facilitate mobile payment across Africa.

The partnership will enable Flutterwave to onboard MTN’s mobile money platform, MTN MoMo, which provides consumers and businesses with an electronic wallet, enabling electronic transfers and payments as well as access to digital and financial services.

Besides acquisition, Partnership with existing payments platforms has become another viable strategy for fintech companies seeking to expand to new markets. Many of them in the African market have partnered with mobile network providers who offer mobile money services, as it is an easy way to reach the underserved.

With their customer-base counting to millions of users, mobile money operators offer fintech companies such as Flutterwave, a sort of already-made customers to incorporate into their networks.

This new partnership will enable Flutterwave to offer MTN Mobile Money as a payment method to its business customers, the company said in a statement.

MTN MoMo which had 48.9 million active users and 581,514 merchants as of June 2021, will help Flutterwave to integrate markets in many African countries where MoMo services are operational.

“As we progress on our journey to becoming the largest fintech platform in Africa, we will empower millions of businesses to embrace e-commerce in our markets to accept digital payments from MoMo consumers. We believe this is an enabler to accelerating digitized payments in Africa. Building strong ecosystems through partnerships is central to our platform strategy and we will continue to invest in expanding the reach of our platform to consumers and businesses in Africa,” Serigne Dioum, MTN Group Chief Digital and Fintech Officer said:

The partnership will allow businesses integrating Flutterwave in Cameroon, Côte d’Ivoire, Rwanda, Uganda and Zambia to receive payments via MTN Mobile Money. The company said it will enable them to expand on its previous collaboration with MTN, beyond Uganda and Rwanda – with the potential of deepening adoption of digital payments and e-commerce in Africa.

The fintech and mobile telecom industries in Africa are both witnessing a boom, presenting opportunities for future economic growth that strategic partnership between players in the industries will help to achieve.

This year, Africa is projected to hit the half a billion mark of unique mobile subscribers and the continent will reach 50% subscriber penetration by 2025, according to the GSMA. Data from Statista also noted that Sub-Saharan Africa alone is responsible for more than 45% of the world’s mobile money accounts with the number of account holders exceeding half a billion by 2020.

Flutterwave said its partnership with MTN will positively contribute to this trend by increasing mobile money usage and penetration in Africa to improve local economies and livelihoods as well as create opportunities for individuals and businesses across the continent.

“Africa has one of the highest growth rates for mobile money adoption and e-commerce in the world. It makes sense that we help provide a seamless payment method to support and ensure African businesses reap the full benefits of the e-commerce boom in the region. Our goal has always been to grow a new wave of prosperity in Africa by creating more avenues for businesses in Africa to accept payments. With this partnership, we can achieve this while creating endless possibilities for our customers,” Olugbenga “GB” Agboola, Founder and CEO of Flutterwave, said.

I wrote this article where I noted how an insurance company in Nigeria, Noor Takaful, returns “surpluses” after settling claims to its customers or selected charities, dealing with the insurance business conflict (any denied claim is profit). Ignorantly, I said the company copied US-based Lemonade on the playbook.

But over the last few hours, many people including professionals from Indonesia have educated me that Lemonade indeed copied what has been practiced in most countries under Islamic tradition. Yet as that debate was going on, some traditional insurers have reached out to me that my post could poison their brands (imagine that for a village boy!).

According to them, there is an inherent risk if people expect that surpluses on premiums could be returned to them or distributed to chosen charities under all scenarios. To provide a balanced perspective, I call everyone’s attention to this comment by “Babatunde” who submitted it in thecomment section.

The comment provides a balanced and nuanced perspective which makes it clear that even the Noor Takaful playbook may not be without cons just as the traditional insurance playbook has its own cons. That is the beauty of free markets: may the best idea win!

—–The Comment from Babatunde——

Dear Prof.

Thank you for your article on the Noor Takaful profit sharing playbook. I have chosen to respond via inmail here rather than on the comment section to avoid the controversial reactions my review may bring, and most important, to avoid being seen as attacking the strategy of Noor Takaful by some onlookers.

Having reviewed some comments from the readers it shows that their might have been some gaps in the article that they do not take into consideration or do not know at all before providing their comments. Hence, this my review.

While the strategy of Noor Takaful sounds great they aren’t practicable in the conventional Insurance companies. Do not forget that Noor Takaful is strictly an Islamic based organization which is guided by the business ethics of Sharia laws.

For one, Noor Takaful does not provide coverage for all types of risks which the conventional insurance companies do. Noor only deals in risks which are supported by the Sharia laws. For instance, Noor Takaful can’t write risks from a Tobacco company or some none approved business concerns. Hence this has limited the options available to the buyers.

Two, I supposed some of the fundamentals on which Noor pays out the profit-sharing were on the premise that there could not be some long-tail claims which may likely be reported months or year after the profit sharing.

I am saying these simply to ensure that the ordinary buyers (who were probably unwilling except for compulsory insurances) do not assume that they were being shortchanged by their present (conventional) insurers who do not participate in the surplus sharing playbook.

As I have indeed mentioned in one of your posts about insurance operations in Nigeria, the fundamentals of pricing for the insurance products, as it with most public goods in Nigeria, are wrong. Let’s example some of the issues here.

First, most consumers of insurance products see the product from the perspective of prices rather than, as it should always be with insurance products, the scope of coverage. The buyer looks into the cheapest insurance products to buy and on the basis of whether it’s compulsory to buy not necessarily because he/she values the benefits being purchased. That’s why you see ordinary Nigerian purchasing a TPO policy from the licensing office for even a lower price than the regulated price of the TPO Insurance coverage. Most of the insurances sold at the licensing offices are either complete fake or issued by insurers who had no plans to honour any resulting claims from such products. They expect that those who bought such products have no intention to make claims on the policy or do not have adequate knowledge of the benefits derivable from the product purchased. The mainstream insurers have long ceased issuing/selling their insurance coverage through those licensing offices due to extreme chances of issuing fake. My point, such buyer of the TPO have no intention of making use of the benefits of the insurance products purchased but just to pass the police checks whenever demanded on the road. Hence, this category of buyers would never buy a comprehensive insurance policy on their vehicle as they do not see the need for it!

Two, the insurance products pricing in Nigeria is fundamentally wrong! I believe we do not charge appropriate rates for the level of risks being carried. For instance where the level of claims on a risk portfolio or from a particular client is high it’s more difficult for the insurers to charge higher rates at the next renewals. This is due to many factors. You are blackmailed with the relationship with the client. Your competitors are lurking around the corners just to take over the business at a lower rates not with or without the knowledge about the performance of the portfolio with the existing insurers. Hence, the insurer is yet forced to maintain the existing rate even on a bad portfolio. If the managing broker on the account is only about the business rather than the mechanics of pricing, then the woes of the insurers are compounded.

The fluidity at which market can adjust its rates is much lower compared to reducing the rates at the request of the client or broker. In the international market which I also have substantial knowledge of how they operate, the mere fact that a loss incident was reported on a major insurance policy is sufficient enough to justify increase in the rates and review of the coverage terms at renewal. It doesn’t matter whether the loss incident eventually leads to a successful recovery or not! The fact that an incident related to the insured risk was reported was enough for the market to react with hardening of the terms. It doesn’t matter whether a particular client has ever made a claim or not. It’s a market portfolio that counts not individual client’s claims activity. I hope we get there quickly in Nigeria. In Nigeria, despite the humongous claims paid so far arising from the #EndSars violent protests of 2020, the market rates are yet to adjust so much/that’s if at all to this losses. So that’s the kind of market an average insurer operates in here in Nigeria.

As an international broker of repute and one who believes in data, I know which insurer I dare not approach to place a business of my client. I know the insurers that I can hold to their words when a claims occur to pay. I know insurers that I would have to threaten or support with prayers to get my client’s claim paid.

Let me make two analogies quickly. One, in the London market when a broker presented a broking slip (that’s the document that contains the details of the risks to be insured and presented to insurer/s for their review and terms) to one underwriter and gets a quote, do the same thing to a second insurer, then a third insurer. After the third insurer such broker or any other broker who presents similar risks (whether using same slip or a different one) would never get terms from any other insurer. They would tell him the risks details are already in the market and refer him to the previous insurers who had presented terms on the risk. If the broker insisted that the new insurer make a quote, such insurer would never quote lower or better than the previous insurers. However, in Nigeria the information sharing is so poor that you can easily set off a pricing war among the insurers with one slip! Two, due to the recent violent uprising in South Africa, in July precisely, the market had so much reacted to the losses that all the risks presented for renewals as at that period were adequately marked-up to reflect the existing market situations. Even a major Nigerian Telco with presence in South Africa took in a large increase in property and cyber renewal premiums even though the risks are here in Nigeria but because the insurances are priced centrally. The Nigerian market is yet to have the nerves to take such bold steps!

The purpose of my thesis above is to show that Noor Takaful isn’t playing the book on the same data as its other competitors in the Nigerian market and it’s important to review it’s business model to avoid providing skewed views to the Nigerian insurance buyers.

Ndubuisi Ekekwe i read your initial post subject matter.

E.g Both Noor Takaful Insurance Limited insurance and the traditional insurance companies under the comprehensive motor insurance ask that the insured pays an annual premium. The insuring public therefore usually ask we sales people the question of “what happens to my money if I don’t have an accident in an entire year”…..this question got answered by the Islamic insuring model by way of returning whatever is left in the portfolio after all associated cost is deducted which includes claim payment.

This question from the insuring public is out of the sense of filling that they are wasting money on motor insuring when they don’t claim over a period of time,well the discount for not claiming is insignificant.

Here is the fair solution to both the insuring public and the insurers, Pay-U . This insurance mobile App charges a user per minute,hence you pay for what you use and you don’t end up filling you’ve thrown away money.

So if you drive a NGN2,000,000 car,you’ll pay less than 2naira per minute while driving and 70kobo while parked,you have the option of turning OFF your insurance when you’re parked.

I have no political party card. And on that, I call it the way I see. I want to congratulate the governor of Imo State for bringing the President to Ala Igbo. Yes, you can throw verbal insults; fine. But fact be fact, disconnecting when you are not disconnected will not serve you any purpose.

If the southeast continues to pay taxes to Nigeria, we need to engage with Nigeria. So, it is good the Imo State Governor was able to bring the president to Imo state. Hopefully, he will visit Ebonyi state next month.

Then, the President spoke like a politician when he said “‘the evidence is there for everyone to see that Igbos are in charge of Nigeria’s economy” in Imo State. I think every part of Nigeria is in charge of something; those varying capabilities are things we can deepen as a nation. We need to show civility and decency with power. The way the President spoke today will bring many friends to him. I challenge him to modulate his policies and be a leader for all Nigerians.

Then, next time there is a state visit, Nigeria needs to showcase our women leaders. This is not 1960!

—–press release on below

THE EVIDENCE IS THERE FOR EVERYONE TO SEE THAT IGBOS ARE IN CHARGE OF NIGERIA ECONOMY PRESIDENT BUHARI TELLS SOUTH EAST LEADERS

President Muhammadu Buhari Thursday in Owerri said that he would want to be remembered as the President who stabilised Nigeria in the area of security, economic prosperity and triumph over corruption.

The President, who spoke at a town hall meeting with South East leaders during his one-day official visit to Imo State, said with less than two years left in his eight-year tenure as President, security still remains a major priority for his administration.

‘‘If there is no security, there is nothing anyone can do no matter how much you try or the initiative you have.

‘‘Security is number one priority and then the economy. When people feel secure they will mind their own business,’’ he said.

The President told South-East leaders that while fighting corruption in Nigeria had become very sophisticated and difficult, he would continue to strive to leave a lasting legacy of integrity and accountability in the system.

‘‘Nobody can accuse me of having companies or mansions anywhere in the country and I thank God that I try to keep myself as clean as possible, so that I cannot be taken hostage.

‘‘I will do my best to ensure that Nigerians that try hard, succeed in their efforts,’’ he said.

On the forthcoming 2023 elections, the President reaffirmed his commitment to free, fair and credible polls, urging the leaders to honestly educate their constituencies on the need to hold their elected representatives accountable.

Acknowledging the resourcefulness and enterprising spirit of Igbo people, the President said:

‘‘The fundamental thing about the Igbo people is that there is no town you will visit in Nigeria without seeing the Igbos being in-charge of either infrastructure or pharmaceutical industry.

‘‘Therefore, it is unthinkable for me that any Igbo man would consider himself not to be a part of Nigeria.

‘‘The evidence is there for everyone to see that Igbos are in charge of Nigeria’s economy.’’

Noting that no country can make any meaningful progress without the development of infrastructure, the President expressed regret that successive governments at the Federal level contributed to the decay of critical infrastructure in the country.

He promised that the Federal Government would complete ongoing key projects in the South East, including the 2nd Niger Bridge as well as the railway lines and routes linking the region with other parts of the country.

‘‘I firmly believe that when you get infrastructure right, Nigerians will mind their own businesses,’’ he said, adding that as a group, the Igbos stand to benefit more from the ongoing development of infrastructure in the country because ‘‘they are more enterprising.’’

President Buhari had earlier commissioned four projects executed by Governor Hope Uzodinma, including the Naze/Ihiagwa/Nekede/Obinze link road, the Balloon Driven/Flood Control drainage at Dick Tiger Road, the Egbeada Bypass road and the New Exco-Chambers, Government House, Owerri.

Addressing Imo residents at the commissioning of Egbeada bypass named after a prominent son of the State, Chief Emmanuel Iwuanyanwu, the President said he was very impressed with the level of work done by the State government.

‘‘I am very pleased with what I have seen and I assure you that I will support Imo State within the Constitution of the Federal Republic of Nigeria,’’ he said.

In his remarks at the town hall meeting, Governor Uzodinma said Ndigbo believe in a united Nigeria predicated on ‘‘justice, equity and fairness.’’

He thanked the President for addressing the interests of Ndi Igbo through deliberate policy initiatives designed to give the people a true sense of belonging, including the ongoing construction of the 2nd Niger Bridge, among others.

Governor Uzodinma said the people of South East would remain grateful to the President for approving the establishment of a Naval Base in Oguta Local Government Area of the State, adding that as time unfolds, the economic benefits of the base would manifest.

The Governor also commended the President for strongly supporting the appointment of two prominent Igbos into two key international organisations-Dr Ngozi Okonjo-Iweala, Director-General of the World Trade Organisation (WTO) and Dr Chikwe Ihekweazu, Assistant Director-General of Health Emergency Intelligence, World Health Organisation (WHO).

In his remarks, the President-General, Ohaneze Ndigbo Worldwide, Prof. George Obiozor assured the President of the continuous support of Ndigbo.

‘‘Ndigbo are committed to Nigerian unity and there is news for those trying to push us out of Nigeria.

‘‘Ndigbo in Nigeria are like fish in the ocean and no matter how rough the storm is, it cannot drive the fish out of the ocean.

‘‘Mr President, it is in this context, that we see a new dawn in your distinguished presence in Igbo land and believe that on your return to Abuja the significance and substance of this visit will form new foundation of a platform for meaningful dialogue on critical issues of concern to the Igbo nation,’’ he said.

Femi Adesina

Special Adviser to the President

(Media & Publicity)

September 9, 2021

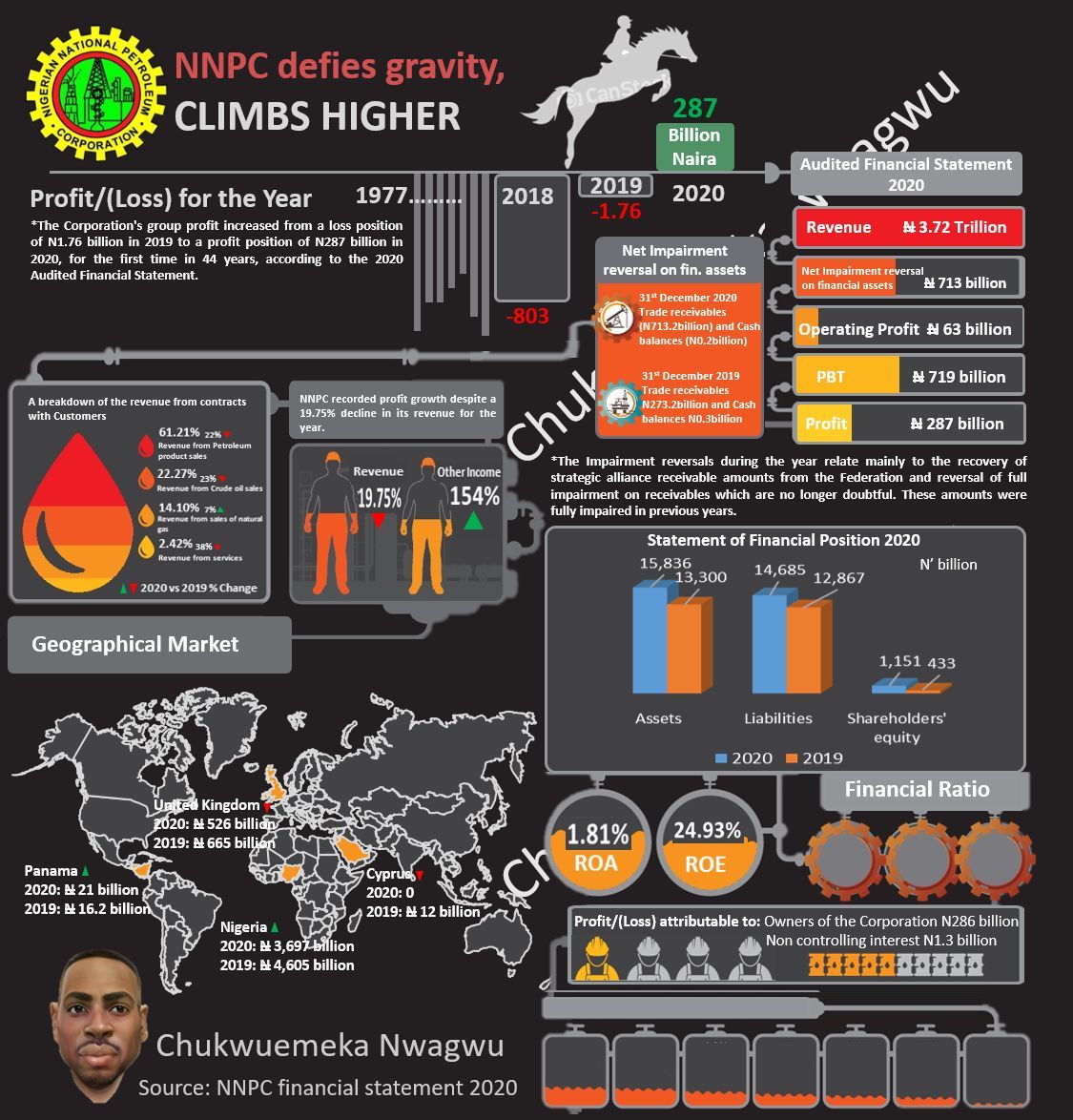

Nigeria is a special place. The nation was celebrating amagical profitability of NNPC only for us to just notice that the profit was indeed “technical” (not driven by the usual common demand and supply equilibrium pricing movements). Yes, some movement of funds from the federal government made the Nigerian National Petroleum Corporation (NNPC) whole. It is indeed a very crazy one for the nation; many have challenged the validity of that profit!

Hoping that audited statements when released would provide clarity, the auditors ramped up the high voltage searchlight, revealing something frightening : “The group reported a net profit of N287.2 billion (Corporation: N235.3 billion) during the year ended 31 December 2020 and, as at that date, the current liabilities exceeded it current assets by N4.6 trillion (Corporation: N729.1 billion)…These events or conditions, along with other matters as set forth in Note 42, indicate that a material uncertainty exists that may cast significant on the group and corporation’s ability to continue as a going concern.” the auditors PricewaterhouseCoopers (PwC) said.

Now, are you going to buy the shares of NNPC? I have explained my experience with Transcorp Plc here.

Yes, NNPC could be teetering on the brink of bankruptcy as the liabilities outweigh its assets by as much as N4.6 trillion. Of course, Nigeria will say nothing to worry because it is Nigeria.

Please, can someone email the full audited statement to us here; I need to spend time and read the revelations well ahead of the 2024 planned IPO, since it is evident that the Corporation will need to go public to raise money, and improve its balance sheet.

Nonetheless, commendation to the current leadership of NNPC for going that close to reveal these then-“classified documents”. Now, we know where we stand in this country: the temple which feeds the nation may need more sacrifices!