First, this is it: the Kuda team waited for me for 3 hours in Lagos for a possible small investment in Kuda. In the end, I did not. I had arrived from the US to run a program for some CEOs and they waited patiently for me. Today, Kuda is worth $500 million. If I had invested $100k, that money would have produced at least $7.5 million within less than two years! Kuda has raised at least $80 million in the last 6 months, and now is priced at $500 million.

Do not pity me (I am fine…lol); pity the 99.99% who are disconnected from this new dimension of value creation and capture. It is because of that anomaly that I created Tekedia Capital, to provide opportunities for We The People to co-own the empires of the future.

Interswitch and Flutterwave jointly hold the 3rd position, behind GTBank and Zenith, as Nigeria’s most valuable financial institutions*. I predict that by 2025, Flutterwave will be worth more than GTBank and Zenith bank combined! Kuda today is bigger than many banks in Nigeria!

I missed Kuda but what Kuda could have given me in 24 months, one startup produced the same multiples in 6 months. That one is also from Lagos. People, open your playbook because by 2025, Nigeria would be radically transformed if you check what is happening in these new species of firms.

I am now loaded in close to 40 of them globally; very soon, Forbes will be invited … hahaha. Join me at Tekedia Capital Syndicate and own a part of the new future.

*N500/$

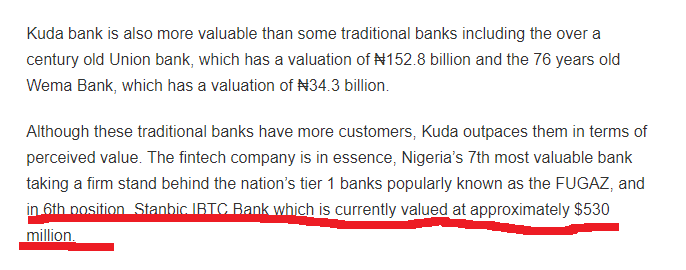

Update: I just noticed that my calculation was wrong. I had used Nairametrics data where it quoted that Stanbic IBTC Bank Plc was worth “$530 million“. But working on a Brief for a client now where I had to compute all the Nigerian bank growth trajectories, perception value, etc, and pulling data from Bloomberg, I noticed that Stanbic IBTC was actually worth N531 billion which is clearly above $1 billion. So, Nairametrics has a big typo there. I have updated the plot accordingly and apologize for the confusion.

Nairametrics data is wrong

Comment on LinkedIn Feed

Comment #1: Well, prof. The takeaway I have from this is to invest in small promising firms. However, let’s not be beclouded with the sentiment of the current fintech valuations and use that as a premise for comparing listed entities such as banks. I sometimes wonder how we value fintechs based on the volume of seed funding they receive. Who uses loan as a yardstick for valuation. I disagree with all these fintech valuation amounts.

We can’t compare a company that is not listed and whose books have not been audited by quality audit firms with banks. Let’s compare apple to apple and if we want to use loan capital as valuation methodology, trust me these fintechs are a far cry from the kind of Tier 2 capital banks receive.

You use the stock exchange shares trading price to value banks and now use loan capital for fintech. That’s misrepresentation of facts. We need to change this current narrative that’s trending in order not to becloud an investors judgement.

My Response: “I disagree with all these fintech valuation amounts.” – that is your right but those sending them money AGREE. I think that is what matters here.

“We need to change this current narrative that’s trending in order not to becloud an investors judgement.” – many said that about Tesla until it went public and many are still confused why Tesla is bigger than all the major car companies combined. Let me say this – people are using expired tools to value empires of the future.

Comment #1b: Ndubuisi Ekekwe “People are using expired tools to value empires of the future” – Banks are valued with stocks while fintechs are valued based on seed capital. The conclusion I can draw from this your statement is that stock exchange is the expired tools. However, I’m aware that the ultimate goal of a private equity is to raise IPO and go public.

“That’s is your right but those sending them money agree” Maybe you can check the balance sheet of banks and see the volume of Tier 2 &3 capital they receive from firms (way higher than fintechs), so I’ll say those sending banks those cash also agree.

I still maintain that we are using different parameters to compares firms and that is not a good yardstick for measurement. Until the auditors show us the true nature of fintechs books, there is an element of bias in those valuations.

Elon Musk company in your example is an outlier as Tesla offered the public renewable energy at a time the world is clamoring for climate sustainability.

Most of these fintechs pretty do same things banks do which is payments and retail lending. Let’s wait till their IPO before we can start doing firm comparisons as you have done.

Comment #2: These valuations of Fintech companies, are they based on current Assets or Potentials of future growth..?

I almost fell into a “hole. “ of selling my Tangible Assets in preference to investing the proceeds into intangible shares and stocks of “ Fancy” companies!

Shortly after, bubbles bursted!

Some of us are traditional investors who belief wholly in Solid Stocks and Barrels! Caution is the Word!

My Response: The challenge is this: it confuses if you use old and expired tools to value these companies. Check the NYSE, all the “fake companies” pop up once they list. So, the problem is not from the companies but lack of people understanding the new economy. Do you know that Facebook can buy close to 8 pieces of IBM, and Paypal can buy 2.5 copies of Goldman Sachs? Instead of caution, ask people to attend modern schools like Tekedia Mini-MBA where we educate people correctly! Yes, I said so. Lol.