Zenith Bank has made a 30% loan loss provision on its loan exposure to 9Mobile (formerly Etisalat Nigeria). I do think, the next step will be to convert all the loans into equities in 9Mobile. I do not think anyone will expect 9Mobile, as #4 telecom operator in Nigeria, to have the capacity to pay any of the loans in the next five years. That is impossible considering the level of competition in the market. So a 30% loan loss provision is just for the books. There is risk the other 70% could also be provisioned if the issues are not well managed.

Nigeria’s Zenith Bank has made a provision on 30 percent of its loan to 9mobile, the country’s fourth largest telecoms group formerly known as Etisalat Nigeria, the bank’s chief executive said on Monday.

“We have taken about 30 percent … as a provision which we believe is very prudent as the company is undergoing restructuring … to prepare for a new investor,” CEO Peter Amangbo told a conference call.

Nigerian regulators stepped in last month to save Etisalat Nigeria from collapse and prevent lenders placing the country’s fourth biggest telecoms group into receivership, prompting a board, management and name change.

9Mobile had taken out a $1.2 billion loan four years ago from a consortium of banks but struggled to repay it due to a currency crisis and a recession in Nigeria.

Zenith Bank is the largest lender to 9Mobile, one source familiar with the matter said. The bank has declined to disclose its total exposure to the telecoms group.

My recommendation for the telcos will be to convert all their loans into equities, consolidating the total loans within 49% equity and then help 9Mobile to raise new capital at the remaining 51%. That way 9Mobile will have capital to run its operations. By doing that, provided the banks can go long, they can recover the money. If they do not do that, it is possible 9Mobile will struggle since it still needs capital, and having the huge loan exposure in its books will make it extremely challenging to find investors. The loan line has to go, turning it into equity, and then help the telecom operator to raise fresh capital, offering the risk taker the majority ownership at 51%.

We all know that being a #4 telecom operator is not a strong position. Only the top two operators matter. The #3 operator is also there, but #4 is never a factor. So, 9Mobile needs a real risk taker to come and pump capital into it. Only the banks can help to make that possible.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

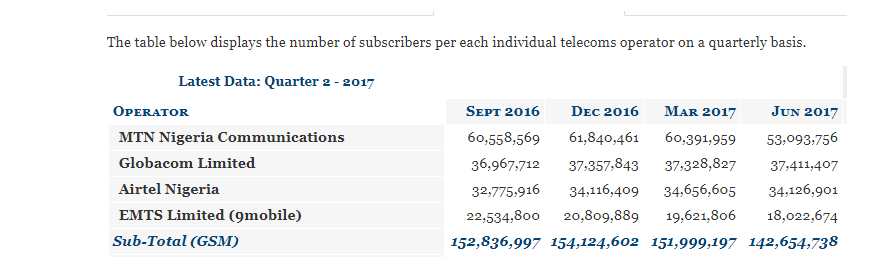

What The Data Shows

From the NCC data, it seems many Nigerians are even dropping their phones. Except Glo, all the telecom operators lost users between May and June 2017. So, the industry is experiencing negative growth, implying that you cannot practically expect 9Mobile to magically make money to pay the loans. That is a reality the banks already know.

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube