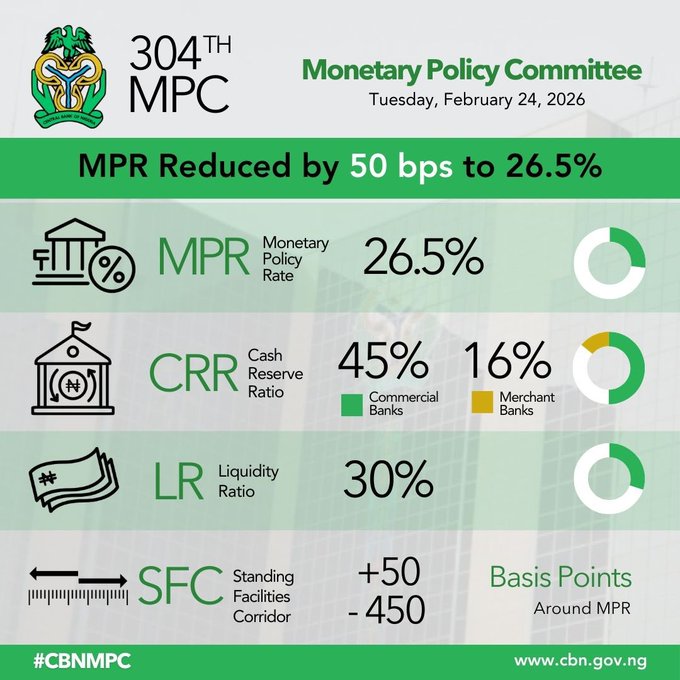

The Central Bank of Nigeria has reduced the Monetary Policy Rate (MPR) by 50 basis points to 26.5 percent from 27 percent, marking its first easing move after an extended tightening cycle.

The decision was taken at the 304th meeting of the Monetary Policy Committee (MPC) in Abuja, with Governor Olayemi Cardoso announcing the outcome. Eleven members were in attendance.

The rate cut comes against a backdrop of sustained moderation in inflation. Headline inflation declined for the eleventh consecutive month to 15.1 percent in January 2026, down sharply from 34.6 percent in November 2024 — a 19.5 percentage-point drop in fourteen months. By conventional monetary policy standards, such a disinflation trajectory creates room for a recalibration of interest rates.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Register for Tekedia AI Lab.

Although the benchmark rate was lowered, the MPC retained other key parameters, underscoring a measured approach to easing:

The Cash Reserve Ratio (CRR) was left unchanged at 45.0 percent for commercial banks and 16.0 percent for merchant banks. The Liquidity Ratio remains at 30.0 per cent. The Standing Facilities Corridor was fixed at +50/-450 basis points around the MPR.

By maintaining tight liquidity conditions through a high CRR, the CBN is signaling that while inflation is easing, risks have not fully dissipated. The CRR remains one of the highest globally, effectively sterilizing a significant portion of bank deposits and limiting the volume of lendable funds in the system.

This balancing act reflects the central bank’s attempt to anchor inflation expectations while cautiously supporting growth. The new MPR of 26.5 percent is the lowest since May 2024, when it stood at 26.25 percent, but policy remains restrictive in real terms given prevailing macroeconomic uncertainties.

Disinflation and Credibility Questions

Nigeria’s inflation descent has been unusually steep. The decline from 34.6 percent to 15.1 percent within just over a year has prompted debate in some quarters about the underlying drivers and statistical base effects associated with rebasing and food price normalization.

The disinflation narrative strengthens the case for easing, yet it also raises questions about sustainability. If price moderation has been driven partly by exchange-rate stabilization, improved FX liquidity, and base effects rather than structural productivity gains, inflation could reaccelerate under renewed fiscal or external pressures.

Ahead of the MPC meeting, analysts were split between a hold and a cut.

Asimiyu Damilare, Head of Research at Afrinvest West Africa, argued that recent macroeconomic developments had strengthened the case for easing. In contrast, the Managing Director of Arthur Steven Asset Management Limited suggested it might be premature to expect a significant move given the limited year-to-date data.

The MPC’s decision represents a middle path: a modest 50-basis-point reduction rather than a more aggressive unwind of prior tightening.

At its 303rd meeting, the committee held the MPR at 27 percent, reinforcing its inflation-fighting stance. The latest move, therefore, marks a pivot in tone, even if not yet a wholesale shift in policy posture. But many analysts had expected a significant basis point reduction that would be commensurate with the decline in the inflation rate.

Will Borrowers Feel Relief?

The more fundamental question is whether the rate cut will materially lower borrowing costs in the real economy.

The Centre for the Promotion of Private Enterprise (CPPE) welcomed the cut but warned that monetary transmission remains weak. According to the think tank, lending rates to businesses remain elevated due to structural constraints, including the high CRR, elevated deposit costs, macroeconomic risk premiums, government borrowing pressures, and high banking system operating costs.

In effect, the MPR functions as a signaling rate, but actual credit pricing is shaped by broader structural factors. When the CRR locks up 45 percent of commercial bank deposits, liquidity conditions remain tight regardless of marginal policy rate adjustments.

The CPPE notes that crowding-out effects from government domestic borrowing further complicate transmission. If banks can earn relatively attractive returns on sovereign instruments with minimal credit risk, incentives to expand private-sector lending weaken.

It added that unless complementary reforms address these rigidities, manufacturers, SMEs, and agricultural producers may see little relief from the 50-basis-point adjustment.

The rate cut also has implications for exchange-rate management and capital flows. Nigeria has relied heavily on tight monetary conditions to support the naira and attract portfolio inflows. Easing too quickly could reduce carry trade attractiveness and introduce volatility into the FX market.

However, if disinflation remains entrenched, real yields may stay sufficiently positive to retain foreign investor interest even with a slightly lower benchmark rate.

For domestic growth, the cut may signal the beginning of a gradual policy normalization cycle. Nigeria’s economy has been operating under historically tight financial conditions, with credit expansion constrained and corporate financing costs elevated. A sustained easing trajectory could improve investment sentiment, provided macro stability holds.

A Gradual Pivot

The MPC’s decision reflects a cautious pivot rather than an abrupt turn. Inflation has moderated significantly, justifying a policy response. Yet by retaining other tightening tools, the CBN is keeping liquidity conditions restrictive.

The CPPE notes that the effectiveness of this easing phase will depend less on the headline rate cut and more on structural reforms that improve monetary transmission, deepen credit markets, and reduce fiscal crowding-out.

The tightening cycle has peaked, but the path toward a meaningfully accommodative stance remains measured and conditional on continued macroeconomic stability.