Former Central Bank of Nigeria Governor, Prof CC Soludo, noted in a new speech in Lagos that Buhari’s Administration may be unable to return Nigeria’s GDP (in US dollars terms) on where it met it in May 2015:

Let me make a point that most analysts miss namely, that in domestic currency terms, the economy is in a recession, but that in US dollar terms, the economy has suffered massive compression. Depending on the exchange rate used, the size of Nigeria’s GDP has shrunk from about US$575 billion when the current government took over to anything ranging from US$354 to US$232, and Nigeria has again lost the first and second positions in Africa’s GDP ranking. At the interbank rate of about N375 per dollar, the GDP is probably around US$288 billion but if we use the parallel market rate of about N465, then we are closer to US$232 billion. Think about this: in the previous 16 years, Nigeria’s GDP more than doubled in US dollar terms. In less than two years, the current government has managed to reduce the size of GDP in dollar terms to about 50% of what it met. We will get out of the recession any moment from now— with oil price and output rising—but it will be a miracle if the government can return the GDP in US dollar terms back to the level it met it even by 2023!

That the economy of Nigeria is deteriorating is no news. In local currency, it is recession. In US dollars, it is a major compression since the dollar-naira conversation rate has changed dramatically.

The implication is that Nigerian banks are suffering, and investors are punishing them despite the fact that an average bank customer in Nigeria may not notice the dire positions of these banks. The banks still have nice looking offices and their officers drive good cars. They rarely lend, so for most customers, provided they can get their deposited monies out whenever they want, all is well!

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

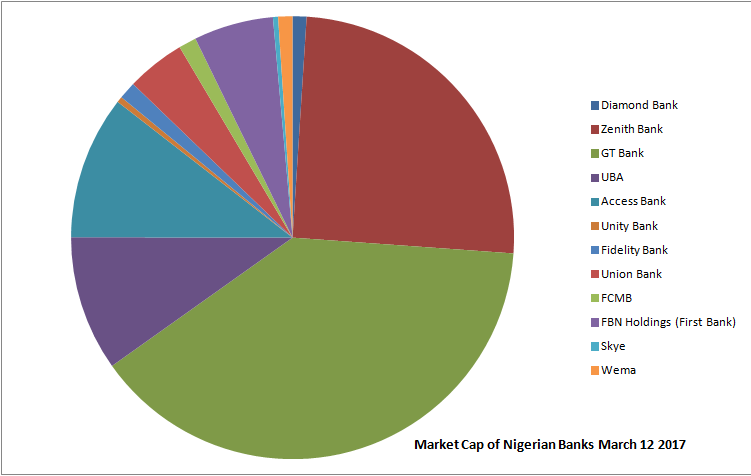

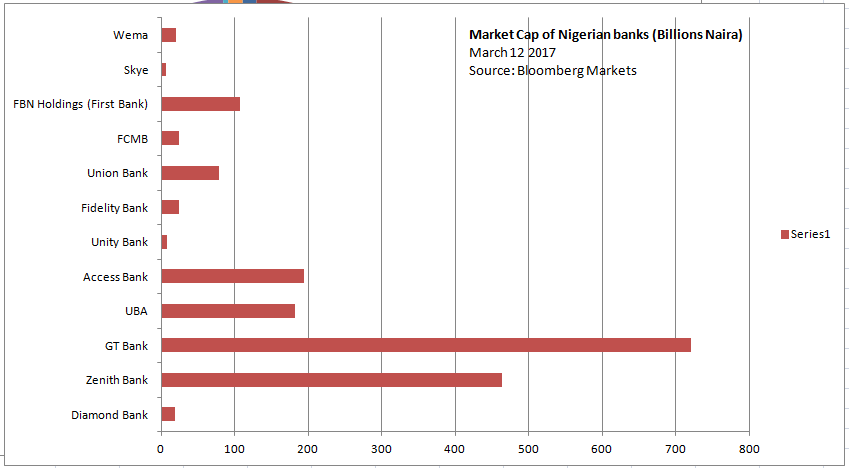

Market Capitalization

Using Bloomberg Markets, the following is the summary of market cap of major Nigerian banks in Billions of Naira, as of today:

- Diamond Bank – 18.760

- Zenith Banj – 464.040

- GT Bank – 721.064

- UBA – 182.123

- Acess Bank – 193.528

- Unity Bank – 7.832

- Fidelity Bank – 23.470

- Union Bank – 79.090

- FCMB – 23.763

- FBN Holdings (First Bank) – 107.327

- Skye – 6.940

- Wema – 19.287

If you convert the above figures to US dollars, most of the banks have no value, when you look from outside. They appear exceedingly cheap. However, foreign investors are not bouncing to claim them. The total value of most cannot pay a top American banker’s annual salary.

The only reason they have positive numbers (i.e. not negative market cap) is due to their real estate holdings. For example, Wema Bank has a strategic Head Office in Marina, Lagos. That building may cover most of the valuations investors are giving the bank. This means that in the core banking operations, Wema Bank has no zero value and its operation negligible in terms of creating value.

Growth Opportunities

The first thing is that these banks just have to hope that our economy will improve. And that means oil will flow and the militants will allow us to pump and sell them. That is the Nigerian way.

It is not likely they will do well if the economy continues to contract. Nevertheless, the following are potential opportunities in the local and African markets

- Collaborate and challenge the Fintechs

Most banks will not notice it yet, Flutterwave and Paystacks are processing more electronic payments than them. This trajectory is expected to continue and if the banks cannot find a way out, they may be unable to change the trajectory of doom. Paga is making more money than Wema Bank. The lesson of U.S. banks on Venmo where they came together to challenge the Paypal company is a good recipe for Nigerian banks. They need their own fintech fast.

- A totally single local currency-agnostic system

Africa is a very complex place to do business. It has multiple jurisdictions requiring visas. But payment must not be that way. One has to find a way for someone in Kenya to pay for goods in Nigeria without even thinking it was using the Kenyan currency. At the Kenyan interface, it sees the Shillings while the Nigerian counterpart sees the Naira. Everything is wired seamlessly underneath and it happens in real time. Nigerian banks with their tentacles in Africa have opportunities here.

- Make it easier for other African businesses to do business in Nigeria

Nigeria is Africa’s most populous country and most ambitious African entrepreneurs are always thinking of Nigeria. Yet, Nigeria is not an easy place to do business. So must of them are skeptical. Nigerian banks could simplify that process and make it easier for banks to do business in the country. They could borrow the Stripe Atlas model.

With Stripe Atlas, entrepreneurs can easily incorporate a U.S. company, set up a U.S. bank account, and start accepting payments with Stripe. Starting today, it’s available to developers and entrepreneurs globally.

The promise of the internet is that location matters less. However, geographic barriers and associated complexity make it difficult to start a global business in many parts of the world.

Nigerian banks may have to do the equivalent which is centered on Nigeria for African companies.

Necessity for New Capital

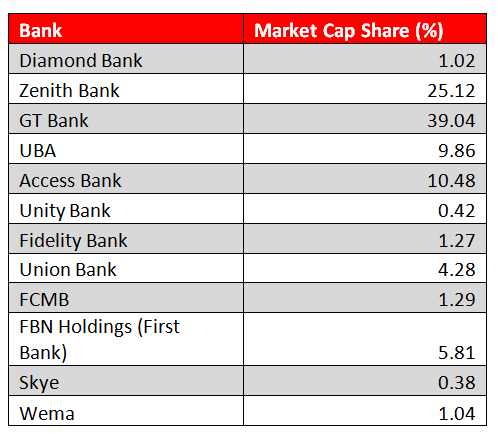

Most banks in Nigeria are seriously under-capitalized. GTBank and Zenith Bank account for more than 64% of the total market capitalization of the banking sector. (We have excluded ETI (Ecobank Trans) in this analysis since it is not really wholly Nigerian.) This presents these banks as clear leaders. Diamond Bank, Unity Bank, Skype and many others are rounding numbers. In short, GTBank can buy all the banks in Nigeria (with shares) with the exclusion of Zenith Bank. Government may have to think how to strengthen the sector as it is obvious that some cannot survive in an era of fintech which has brought erosion of bank fees.

Banks need new capital because they are not just competing with other banks in Nigeria. The ecosystem of competitors are huge and they include telcos (Airtel Money via Access Money), e-commerce companies (Konga Pay), tech companies (Flutterwave) and more.

Rounding Up

It will be extremely challenging for most banks in Nigeria to continue to operate. Some of them could better pivot at this time or merge. That pivot could be redesigning their operations to be digitally driven. Unfortunately, that may mean closing branches and firing staff. Without that paradigm, it is not just clear how most of these bottom banks will survive in the next five years.Their problems are huge – they lack the capital to invest in new sources of growth and they will struggle to have scale to reduce cost which is very critical in the new banking era.

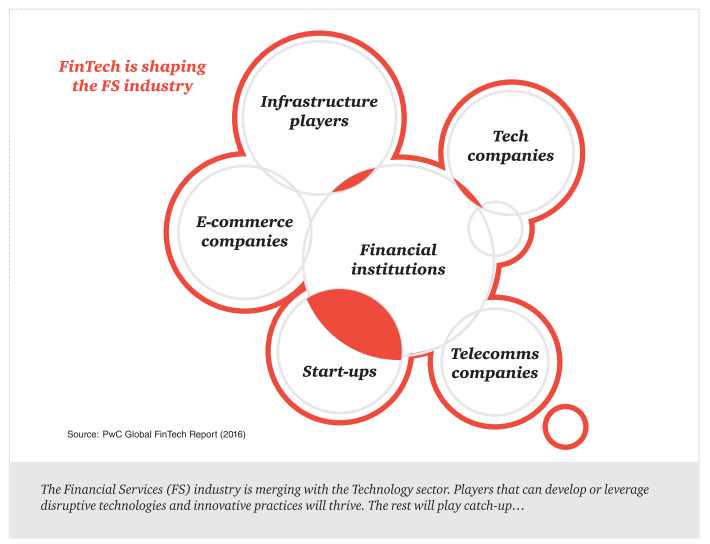

FinTechs are redrawing the competitive Financial Services landscape and blurring the lines that define players in the sector. Their offerings range from competing financial services such as alternative lending, to additive solutions atop existing banking services, to enabling technologies for the banks themselves. Capitalizing on the latest mobile, cloud and digital technologies, Nigeria is increasingly becoming home to many FinTech firms who are trying to shake up and be accretive to the banking value chain.

Findings from the survey by PwC also reveal that Nigerian Financial Services players see changing customer needs as the top impact FinTechs have on their business, with up to 60% of respondents indicating that up to 40% of financial services business will be at risk of standalone FinTechs by 2020.

There is never a time in Nigeria’s banking history for the Central Bank of Nigeria to demonstrate leadership. We are in a heavy banking crisis since without improving market caps, these banks will be timid in the markets. You cannot be talking of a deal of N10 billion as Unity Bank when your whole market cap is less than N8 billion. We are in economic stasis and banks need to move fast to avert a major crises in the nation.

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube