By Chuma Akana

In recent times, the Nigerian FinTech ecosystem has witnessed strong drive and campaign across various frontiers including payments, personal savings, financial services, financial inclusion and mobile lending. This has precipitated the attention on FinTech companies and led to unprecedented growth in the industry in a short period. According to the Nigerian Start Up Funding Report, in 2018, Nigerian technology companies attracted investments of over N42 billion and 73% of this sum was invested in FinTech Companies. Also in 2018, wallet.ng, a Nigerian FinTech company was listed among the Top 100 FinTech companies in the world, in a report published by KPMG and H2 Ventures- the 2018 FinTech 100.

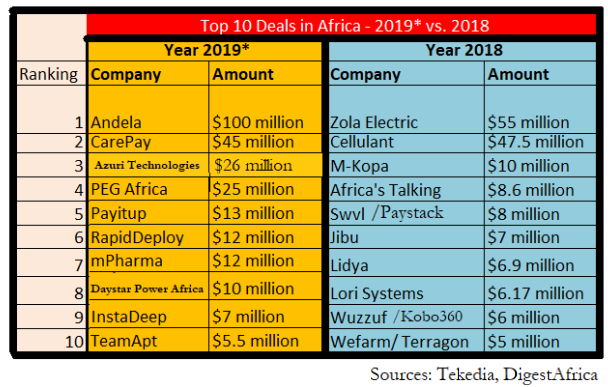

According to the Nigerian Startup Funding Report by Techpoint, Nigerian startups raised $17.6 million in Q1 2019, 8.5% higher than they did in Q1 2018. With the likes of Microsoft setting up digital villages in Nigeria, more Nigerian FinTech startups are leading the drive for financial inclusion in the continent.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Possibly, a large part of the industry growth is directly related to the amount of funding being pumped in by investors in the Nigerian FinTech ecosystem, as it is widely agreed that funding is important for FinTech companies to thrive.

FinTech companies like other companies in Nigeria, can have various sources of funding including debt or equity. With respect to debt, most startups may be permitted by their Articles of Association, to raise capital through debt from banks, financial institutions and the capital market, subject to regulatory requirement.

For a lot of tech companies, funding can be a major challenge at the onset, particularly when the product/concept is novel and innovative. Typically, the founders would raise the initial capital from individuals/family for the first few months or years of the business, before they are able to access external funds through seed funding or series round, to scale their business. This lack of funds or access to credit has resulted in the exit of some promising tech companies in recent years. As mentioned above, equity, debt and mezzanine financing are available funding options for new and growing tech companies, however what we see, is that most FinTech companies raise equity instead of debt, as investments have mainly come from venture capitalists and private equity firms.

These venture capitalist are incentivized to provide these funding, by the provisions of the Venture Capital (Incentives) Act LFN 2004 which provides some tax benefits for the Venture Capital Firms including; accelerated capital allowance for equity investment by a venture company in a venture project for the first 5 years of the investment; reduction of withholding of tax on dividends declared by venture projects to venture companies for the first 5 years from 10% to 5%; export incentives such as export expansion grants if the venture project exports its product; exemption of payment of capital gains tax from gains realized by venture companies for a disposal of equity interest in the venture project; and exemption from companies income tax for a period of 3 years , which may be extended for an additional final period of 2 years.

Most startups would go through a Series A, B and C round, and believe they have gained sufficient funding to grow and scale their business, add new products to their portfolio, and return good profit to investors. Still, there is the option of listing in the capital market and conducting an Initial Public Offering (IPO) to offer shares to the public, and this is not uncommon in international markets. In 2002, Paypal which was founded in 1998, raised the sum of $70.2 billion via IPO, and is presently listed as a Forbes Fortune 500 company. Also Facebook raised $16 billion via Initial Public Offering in 2012, and has become one of the biggest companies in the world. However, raising fund from the capital market seems not to be a popular option for most tech companies, as a result of the perceived difficulties in managing a public company and the stringent reporting requirements.

In recent times, the Nigerian Stock Exchange have indicated that it is planning to reposition the Alternative Securities Market “ASEM” which is the NSE initiative for SMEs as a “Growth Board” that will provide listing opportunities and capital formation for Startups, SMEs and Venture Capital/Seed companies with a keen focus on startups creating value with transformational impact on the market. Basically, the initiative allows the target companies to float shares with a more flexible regulatory system than is applicable to the main board or premium board.

The Growth board has an entry stage which is primarily targeted at startups, tech companies and venture businesses. It is imperative that the company is a public limited company in legal form i.e as prescribed by Section 24 of the Companies and Allied Matters Act. Other requirements include that the company shall have a market capitalization of N50m – N500m and a public float/minimum shareholders of 10% and 25 shareholders respectively. Continuing obligations and reporting include semi-annual and annual company’s statements, while the Nigerian Stock Exchange will provide strong support structures for the company including accounting, audit and legal services at a pre agreed and prepaid rate with the startup.

For these companies, the benefits of listing on the Nigerian Stock Exchange above other funding options include the highly liquid nature of the market, value creation and corporate governance. There is also the issue of optimal price discovery, greater brand profile and visibility for investors, customers and consumers. Through listing, these start ups are also sure of business continuity, recognition in global markets, transparency/credibility and an exit route for private equity and strategic core investors.

The companies listed on the growth board are supported by the 3 pillars of designated advisers, growth ambassador and NSEs institutional services. While the regulatory and governance pillars are designed to facilitate the growth and institutionalization of these companies, the institutional services relate to the NSE’s initiative via partnership with strategic providers to offer companies access to expert services such as leadership development, succession planning and formalization of business processes. This enhances the company’s capacity to define its business model and integrate it with its structures, systems processes and people. Some proponents also opine that accessing funding through the capital market would give these tech companies an easier capital flow while reducing the cost of funding.

It is believed that this option of capital market should be considered by FinTech companies, as it will boost global recognition, ensure customer confidence and good corporate governance which is the hallmark of stable and successful companies.

Chuma Akana is a FinTech lawyer and writes from Lagos.