Crypto investors are bracing for another explosive year as Solana (SOL) continues to strengthen its position among the market’s top performers. With institutional capital flowing back into high-speed blockchains and new developers flocking to the ecosystem, Solana’s fundamentals are aligning perfectly for a potential rally toward $500. But as impressive as Solana’s forecast appears, analysts say the next massive gainer might not be an established network—it could be an emerging AI-driven project known as Ozak AI, which combines blockchain and artificial intelligence to target a potential 100× upside in the coming cycle.

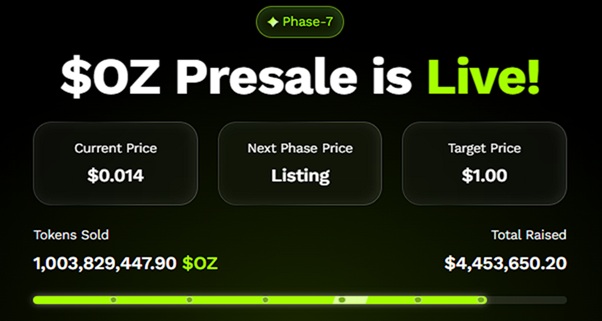

Currently in Stage 5 of OZ presale at just $0.0014, Ozak AI has already raised over $4.4 million and sold 1 billion tokens, signaling that early investors are positioning themselves before what could be one of the most transformative launches of 2025.

Solana (SOL)

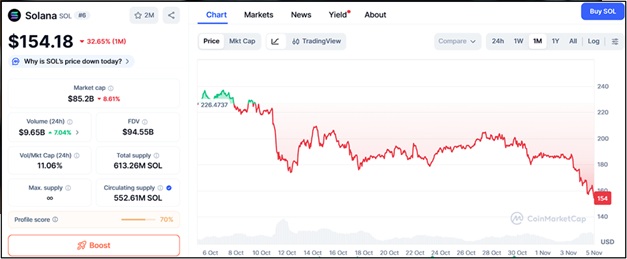

Solana, now trading around $154, continues to stand out for its speed, scalability, and ecosystem depth. Its expanding DeFi and NFT infrastructures, combined with growing institutional integration, are solidifying Solana as the leading smart contract platform behind Ethereum. The recent surge in on-chain volume and stablecoin activity demonstrates growing confidence in its network’s resilience and cost efficiency.

From a technical perspective, Solana shows resistance at $165, $178, and $196, while support levels lie at $142, $130, and $118. If SOL breaks above $178 and maintains momentum, analysts see a clear path toward $500—a level that could make it one of the best-performing large-cap assets of the next cycle.

However, even with a potential 3× rally, Solana’s massive market capitalization limits its explosive upside compared to smaller, early-stage projects. Investors seeking exponential gains—the kind that can turn thousands into millions—are increasingly looking toward innovative, utility-driven presales like Ozak AI.

Ozak AI (OZ)

While Solana focuses on scalability, Ozak AI is revolutionizing how intelligence interacts with blockchain. Its ecosystem is powered by AI prediction agents, machine-learning models capable of analyzing massive amounts of blockchain data, social sentiment, and price movement in real time. These agents identify predictive patterns that give investors and traders a significant advantage in spotting trends before they develop.

What makes Ozak AI so attractive is that it represents the fusion of two of the most powerful narratives in technology—AI automation and decentralized finance. The project’s partnerships with Perceptron Network, HIVE, and SINT enhance its scalability, speed, and interoperability. Together, they enable Ozak AI to leverage over 700,000 AI nodes, integrate real-time blockchain signals, and even connect voice-activated AI systems with Web3 applications.

In terms of credibility, Ozak AI’s CertiK and Sherlock audits set it apart from the average presale, giving investors assurance of security and transparency.

At its current presale price of $0.0014, even small investors can secure large positions before listings. For instance, a $2,000 investment today would buy approximately 1.43 million tokens—worth $1.43 million if Ozak AI reaches $1, marking a 100× return that could easily outperform even the strongest established cryptos like Solana.

Why Analysts Say Ozak AI Could Run Higher

While Solana’s growth is tied to blockchain infrastructure and DeFi demand, Ozak AI’s potential stems from AI adoption, one of the fastest-growing global industries. The 2025–2026 cycle is expected to be dominated by projects that combine AI and blockchain utility—and Ozak AI sits at the core of that convergence.

The project’s predictive AI layer could soon power smarter decentralized applications, automated trading strategies, and real-time blockchain insights. Analysts argue that this technology gives Ozak AI a competitive moat that traditional layer-1 networks can’t match. With a lower market cap and massive innovation potential, Ozak AI’s growth ceiling is far higher than most altcoins entering this bull market.

Solana’s Strength Meets Ozak AI’s Explosive Potential

Solana is undeniably strong—its path toward $500 looks increasingly realistic given its momentum and developer traction. Yet, Ozak AI represents a different kind of opportunity—one that mirrors the early days of Ethereum or Solana before they became household names.

With its blend of AI-driven intelligence, verified audits, and presale-stage entry, Ozak AI offers investors a rare combination of innovation, scalability, and accessibility. In short, while Solana’s growth story impresses, Ozak AI’s trajectory could run much higher, giving early adopters the kind of life-changing upside that only comes around once per market cycle.

About Ozak AI

Ozak AI is a blockchain-based crypto project that provides a technology platform that specializes in predictive AI and advanced data analytics for financial markets. Through machine learning algorithms and decentralized network technologies, Ozak AI enables real-time, accurate, and actionable insights to help crypto enthusiasts and businesses make the correct decisions.

For more, visit:

Website: https://ozak.ai/

Telegram: https://t.me/OzakAGI

Twitter: https://x.com/ozakagi