In a previous article on Tekedia, I laid the foundation for explaining why the Handshake Blockchain is one of the most resilient Blockchains in the world.

Why is that?

Because its got some of the things the Bitcoin ecosystem has which are great and something of what the Ethereum Ecosystem have that are great. It’s the best of both.

The Ethereum Ecosystem has a lot of activity going on. This is mostly on what are called Layer 2’s – such as Sidechains and EVMs (Ethereum Virtual Machines), but they are not hard forks.

What’s good about them?

They are fast. That’s it. They process transactions multiple orders faster than the eth core… and oh yeah… they are way cheaper. That is going to accelerate as a new technology on the system becomes available which is known as ‘sharding’.

The problem is, they are off chain. They are owned by commercial actors… those actors are now under the control of the US SEC (Securities and Exchange Commission) so…

Where have we seen this before? Ultimately, it could be argued they are not decentralized at all.. and that means, to be precise, they can’t even be called ‘Web 3’.

The Bitcoin core is more or less impenetrable. You can’t nuke it, you can’t hack it, you can’t litigate against it, you can’t reverse transactions on it. There is nobody to litigate. You might as well pass a bill that the movement of the tides can only happen by an order of Government, and it is only allowed to rain on Tuesdays and Thursdays late at night. – Notionally amazing, but practically useless.

Bitcoin Blockchain however becomes slow under load, and transaction prices can rise rapidly with demand.

The Handshake Blockchain is a smaller, lighter, ‘hard fork’ of Bitcoin. It has a market cap that is far too small for traders to be jumping in and out of at any volume that could be viable.

It has one big utility – ‘True’ Web 3 domains. These domains are minted to the blockchain core, as the way ENS is to the Ethereum core. They are not off any sidechain or scaling system. Unlike ENS however, which only permits ‘Second Level Domains’ (SLDs) off ‘.eth’ The attraction is that Handshake allows the minting of new TLDs (Top Level Domains).

This has proved hugely popular. There are now 9.7 million domains in existence, and 9ja Cosmos is a significant player, holding about 0.062% of the ecosystem, which is actually quite a lot for a single entity in the community.

I previously pointed out how the handshake token, HNS made multiple performance gains against Bitcoin from the period roughly start of November to end of last month.

But now, we need to move on and talk about a few other new things that happened since, rather than go into great detail about the topic I initially prepared to write about.

That is because three significant things have happened very recently.

- The Collapse of Silvergate.

The collapse of Silvergate came on the back of a lending spree with troubled businesses in the crypto world, such as FTX. Silvergate delayed its annual filing with the Securities and Exchange Commission, warning that it may go out of business. That news prompted the bank’s biggest crypto-industry clients, including Coinbase and Paxos, to pull their deposits.

Most of the cryptocurrencies fell sharply in empathy. This included both Bitcoin and HNS.

- The demise of SVB

Silicon Valley Bank (SVB) was a commercial bank headquartered in Santa Clara, California. SVB was one of the largest banks in the United States and a member of the S&P 500 index. On March 10, 2023, (yesterday) after a bank run on its deposits, it failed and was taken into receivership by the Federal Deposit Insurance Corporation in the second-largest bank failure in American financial history.

Now the thing about this is that the sentiment that followed in Cryptocurrency on SVB was very different to the reaction to Slivergate.

Yes, the public viewed Silvergate as a ‘Crypto Problem’ while it viewed SVB as a traditional centrepiece of a mature US Banking Problem

Both HNS and Bitcoin rallied sharply.

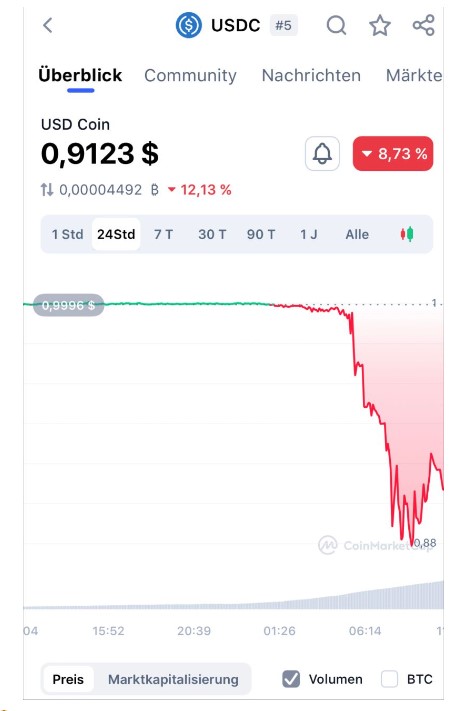

- Loss of Dollar Peg, and slide of the USDC

Today, the Stablecoin, USDC lost its peg to the US Dollar.

USDC is the second largest stablecoin and boasted a $43 billion market cap (at least before substantial outflows surrounding the SVB concern). Other stablecoins even have exposure to USDC, with both FRAX and DAI using USDC for significant portions of their collateral.

Circle is a peer-to-peer payments technology company that manages USDC, It was founded by Jeremy Allaire and Sean Neville in October 2013. Circle is headquartered in Boston, Massachusetts.

Silicon Valley Bank is one of six banking partners Circle uses for managing the ~25% portion of USDC reserves held in cash. While we await clarity on how the FDIC receivership of SVB will impact its depositors, Circle & USDC continue to operate normally.

Circle is currently protecting USDC from a black swan failure in the U.S. banking system.

SVB is a critical bank in the U.S. economy and its failure.

Stablecoins are effectively like the services of a CBDC contracted out into the public sector, They are extremely heavily regulated and are anchored in a sovereign currency.

When a stablecoin gets in trouble it has huge implications for CBDC’s, and other sovereign instruments as its more closely associated with traditional sovereign instruments than it is with cryptocurrencies.

There may be a cue to the e Naira here.

The Circle website says:

‘USDC is a digital dollar, also known as a stablecoin, that’s available 24/7 and moves at internet speed. USDC lives natively on the internet, running on many of the world’s most advanced blockchains. Billions of USDC change hands every day, and every digital dollar of USDC can always be exchanged 1:1 for cash…..’

Well, apparently, not today!

A verdict on a US Stablecoin is effectively a verdict on the Dollar.

I watched a video earlier today which explained the UK cumulative degradation of the Defence Budget over multiple governments since the end of the previous cold war and the collapse of the Soviet Union,

Suddenly thrust into a situation of needing to support Ukraine, and with a threat of direct action from Russia entirely possible, UK no longer has sufficient air assets to now successfully pull her weight on the Polish border assisting Ukraine, and simultaneously have sufficient Typhoon coverage to protect against air or sea launched Russian cruise missiles.

We are seeing potentially seismic shifts in international relations that have a strong potential to reposition the US Dollar from being a single dominant global currency.

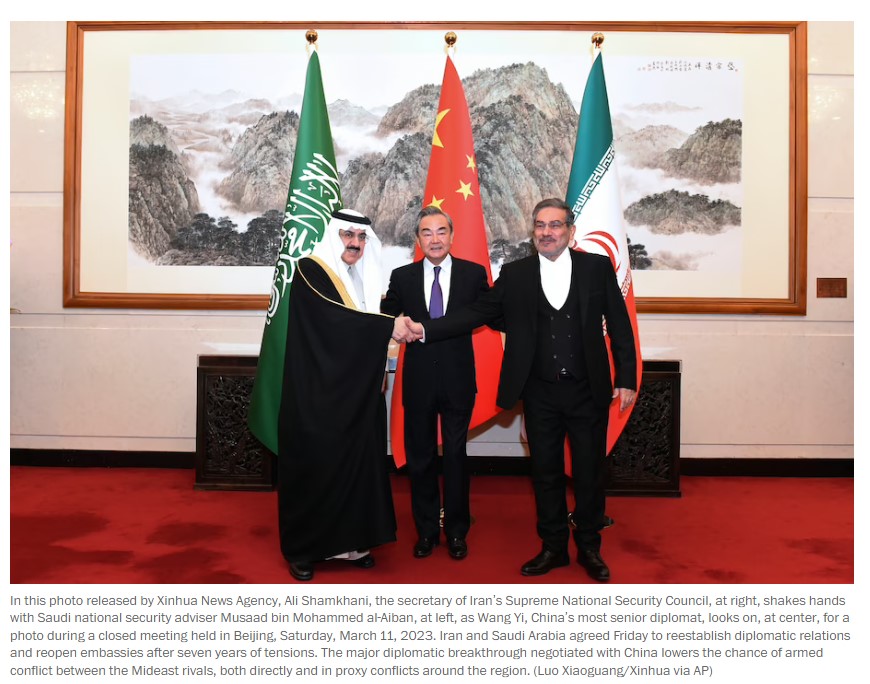

Most of these changes are happening in the Middle East, where firstly, last year, Chinas’ Xi came away from Saudi Arabia from a much more successful visit than US’ Biden. China is doing an oil deal that won’t involve USD. Recently Iran and Saudi Arabia met to agree re-establishment of diplomatic ties. Talks are underway for both countries to be admitted to BRICS.

Meanwhile Israel is courting the establishment of ties with many Arab and Muslim nations.

With the US Debt/GDP running at 120.36%. USD position as the defacto international trade medium is critical to its stability, and the life of the US economy.

There is a fight the USD now feels it has to wage, not only against a diversification away from the dollar by sovereign actors, but also by increased interest in cryptocurrency payment media by global corporations and domestic individuals.

The US is increasingly seeing a world not transacting in dollars, and doesn’t like it.

Conclusions

Sovereign nations have military and economic deterrents both independently as a nation and through collective power built on agreements and treaties. Certain minimal levels of autonomy need to be preserved because the global political landscape can change. Today’s allies and partners can become tomorrow’s adversaries and competitors.

‘Crypto Nations’ (yes I call them that) cannot build physical defences and cannot build assault weapons and go on the offence. But what their makers can do is create them with imperviousness, immutability, self-propagating autonomy, and, post creation, no human with accountability retention. Nobody to be targeted by sovereign law, nobody to be targeted by statutory compliance. Nobody to be targeted with taxation.

The Ethereum ecosystem is very like the UK’s defensive dilemma. It’s lulled itself into a sense of false security, going 100% for speed and flexibility, bad at the core since PoS (proof of stake), and even worse at the EVMs and L2s/sidechains. Sharding will make it worse still.

With the US policy the way it is going, and with projects exhibiting problems more typical of non-blockchain solutions, I don’t see a good future for it.

Outside the Ethereum ecosystem, where ‘design defence’ features are better, Crypto Nations’ need to build their own GDP profile.

The days of a blockchain just having a coin are gone. So are the days when a blockchain could be built around a series of collectibles. The blockchains of the future need to be dynamic, interactive, and drawing human beings into their system by amazing things and amazing ways to be involved as a creator, as a vendor, and as a consumer.

Yes, they need to exhibit all the properties of a real world nation with functions that create Gross Domestic Product (GDP)

You should be able to ‘go japa’ there, without even physically moving from where you are!

As we look back on the impact of both Silvergate and SVB how they pulled the whole cryptocurrency markets one way, and then another, this should not be possible.

In a new world where Blockchains evolve to have a combination of the right levels of secure autonomy, and (Blockchain Asset 3) BCA 3 – unbound tokenized utility with self sustaining GDP, a coin will stand on its own, just as sovereign FIAT.

No more ‘pack’ performance. No more ‘group sentiment’ from investors!

9ja Cosmos is here…

Get your .9jacom and .9javerse Web 3 domains for $2 at:

All reference sites accessed between 08-11/03/2003

linkedin.com/posts/john-mc-keown-nigeria-expert_how-9ja-cosmos-can-bring-bca-3-status-utility-activity-7026341390162776064-V97A?

linkedin.com/posts/john-mc-keown-nigeria-expert_the-value-trilemma-of-fiat-bitcoin-and-ethereum-activity-7038628934606811136-izqR?

bloomberg.com/news/articles/2023-02-15/brics-debates-expansion-as-iran-saudi-arabia-seek-entry

middleeastmonitor.com/20230216-brics-discussing-decision-on-saudi-arabia-iran-memberships-this-year/

nytimes.com/2023/03/11/us/politics/saudi-arabia-iran-china-biden.html

circle.com/en/usdc

edition.cnn.com/2023/03/08/business/silvergate-winds-down-crypto/index.html

en.wikipedia.org/wiki/Silicon_Valley_Bank

web3isgoinggreat.com/?id=usdc-loses-peg-to-the-dollar

reuters.com/world/chinas-xi-starts-epoch-making-saudi-visit-deepen-economic-strategic-ties-2022-12-07/

usdebtclock.org/

logo")