You are invited to 2021 Tekedia Innovation Week (Nov 22-27, 2021 ). The sub-theme is Growth Makers, and it is packaged within the Tekedia Mini-MBA theme of Innovation, Growth and Business Execution. All participants of Tekedia programs (mini-MBA, CollegeBoost, advanced diploma, etc) in the year 2021 qualify to attend free.

For Zoom links, login with your registered email for access.

Theme: Growth Makers

Date: Monday – Saturday (Nov 22-27, 2021 )

Time: 7pm – 8pm WAT daily

Venue: Zoom Click here https://school.tekedia.com/updates/2021weeks/

Here are our Faculty members; they will be speaking on different topics, covering many domains of innovation, and innovation cases. It’s always an amazing academic festival in our Institute.

Schedule/ Faculty (Nov 22-27, 2021):

Mon –Aderinola Oloruntoye, Dean, Workforce Group

Tue – Olanrewaju Oyinbooke, Head, DMO, AXA Mansard

Wed – Seun Ayegbusi, CEO, Insurpass

Thur – Dotun Jegede, Partner, Dee Bee Consulting

Fri – Emeka Obiodu, Manager, NVIDIA

Sat – Ndubuisi Ekekwe, Tekedia Institute

To register for the next edition of Tekedia Mini-MBA or other Tekedia programs, go here.

We put the Igbo Apprenticeship System into the pages of Harvard Business Review as a framework within the global construct of stakeholder capitalism. From BBC to Economist, we have put efforts to inform global leaders that Africa has what they are looking for. In 2022, Tekedia Institute will unveil a new course with focus on learning, developing, mastering and understanding the Igbo Apprenticeship System (IAS).

Yes, we have developed manuals, cases, and videos to help practitioners and business leaders to understand what drives the Igbos, and how any participant can master the heritage and advance the wealth in communities.

Simply, while you master the Adam Smith-inspired current economic system, you must also pay attention to the Umunneoma (“good brethren”) Economics-anchored IAS. IAS has a promise to usher a livable future of shared prosperity at scale.

The Igbo Apprenticeship System is a business philosophy of shared prosperity where participants co-opetitively participate to attain organic economic equilibrium where accumulated market leverageable factors are constantly weighted and calibrated out, via dilution and surrendering of market share, enabling social resilience and formation of livable clusters, engineered by major participants funding their competitors, with success measured on quantifiable support to stakeholders, and not by absolute market dominance.

This course will advance Tekedia Institute’s mission: “to discover and make scholars, noble, bright, and useful“.

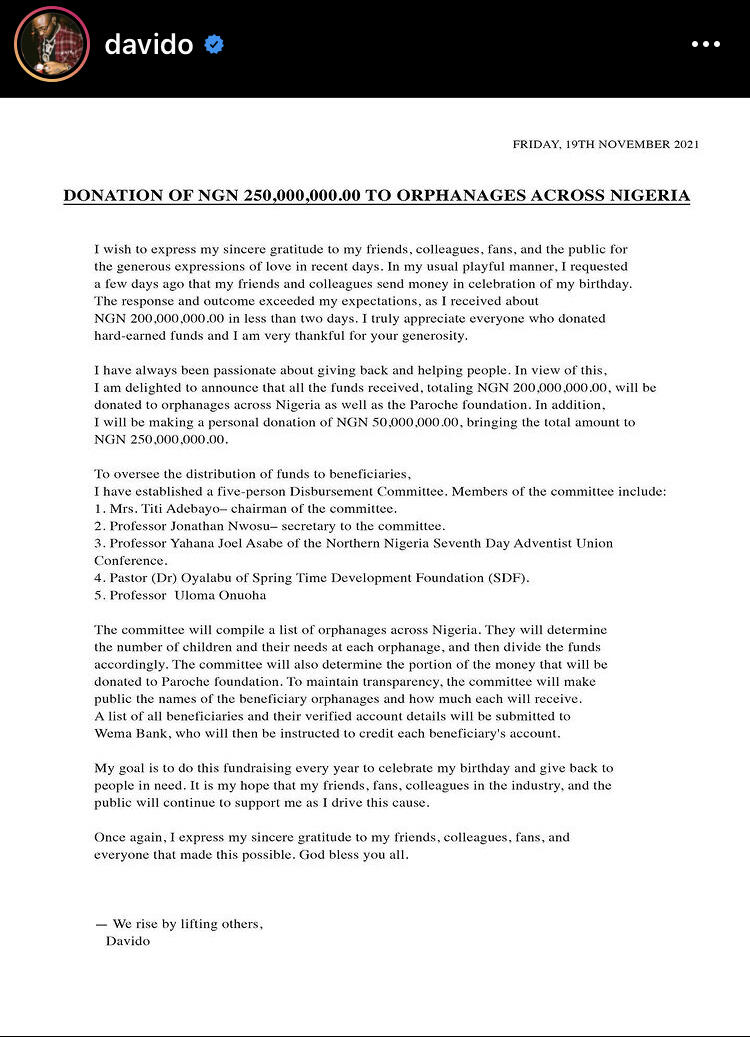

The African superstar David Adedeji Adeleke Aka Davido who just turned 29 years of age turned his pre birthday activities to fund raising. He jokingly asked his friends, fans and well wishers to send him at least 1 million naira each so he can gather enough funds to clear his new car from the wharf. Immediately he made that request, it became wild like a money rush, money started rolling over each other, People started sending money and it was as if it’s a competition of who can send first or send the most money to the Music Taliban.

Some sent out of love and admiration for the craft of the Music mega star while some sent theirs in order to place the artiste in their debt but whichever the motives were, millions of money were gathered; Millions upon millions cried and rolled over each other into the Wema bank account of the singer which he said was opened specifically for this purpose. A whopping sum of about 30 million naira was gathered in the bank account of the Fem crooner in less than one hour after which he made the request.

Not just money, cryptocurrencies were sent to him too. He shared his cryptocurrency wallet addresses where he asked people who prefer to send cryptocurrencies like bitcoin or ethereum to send the value of 1 million naira instead into the wallets for the sake of convenience.

Naira, dollars and cryptocurrencies were sent to the man loved by all with joy in the heart of the friends and fans; the senders and in less two days, about 200 million naira was realized surpassing his initial target of 100 million naira.

Judging from his antecedents, people placed a bet with each other that Davido being a humanitarian and philanthropist who have been ruled by his basic philosophy of ‘we rise by lifting others’ which he always find time to categorically emphasis that it is what motivates him to help people and putting smiles on faces of people; almost everyone predicted that he will give all the money out. Well, the bet was right as he gave out all the 200 million naira raised for him for his birthday celebration to charity and even added an extra 50 million naira of his own money totaling 250 million naira given out by him to the orphanage.

David Adeleke aka Davido has clearly written his name in the sand of time as the most philanthropic Nigerian entertainer ever lived as it is the record that nobody in the entertainment sphere has given that much to charity as a philanthropic gesture.

He has earned different good titles for himself because of these good deeds out of which the most befitting is: A David with a heart of king David.

Adam Smith Economics taught us the power of Capital as a factor of production. Musician Davido has provided a case study for Social Capital as an enabling tool in this age of social media virality.

The Igbo Apprenticeship System has validated the thesis of Communal Capital through the ubuntu philosophy of shared prosperity.

From social to communal to big tech aggregation, this is the age of grand unification. Find ways to connect into your world because it has all that you need, to thrive.

Tony O. Elumelu, C.O.N's Heirs Holdings bought most of the holdings of Shell

NOT AN ‘OILMAN’

First off, I’d like to clarify, I’m not an ‘oil man’, never have been.

A long time ago, I had overall responsibility for a section of NAPHTA (natural gas) pipeline which was landed off the south coast of Ireland, near a place called Kinsale. I was involved in an on-land section of the pipeline (Main contractor, Kellogg).

That phase involved four termination/ingress points, one at Cork City, to supply an existing piped city gas network, a second at a urea/fertilizer plant at Cobh, a third at a generating station at Aghada which had just been rekitted with triple turbine gas generators. The final point was an AGI at Midleton, which was intended to serve a planned extension to Dublin.

I was live on that for about two years after which I was teaching Maths, The Sciences and Engineering Drawing for a few years in a secondary school in Trinidad.

On the success of a construction ERP in London, I was brought to see Shell in PHC in 2006 by Brunel. That didn’t work out because MEND were on the move, and Shell was locked down. I spent the first week doing an acquisition appraisal for a hotel chain, and spent the balance of my visit as a ‘guest’ of Netcom Africa in Lagos.

Working for Netcom later I developed a strong appreciation of site regulations. Pitching to O&G wasn’t just about a solution architecture offering performance at a cost, but also had to show our Field Operations had intimate grasp of how to behave on site, and respond to various eventualities. Once on an O&G site, everyone is the employee of an O&G Major by proxy.

Around ten years ago, I did engineering services advisory to a condensate pipeline in Delta State terminating at Ughelli. Line subcontractors involved were Zahchem and DeltaAfrik.; Main client: TOTAL.

You won’t find selfies of me with Oil Derricks in the background, or onboard an FPSO, simply because they never existed. My exposure scratches the surface of those industries and there is an enormous amount I simply don’t know.

That said, I DO get a lot of engagement on LinkedIn that even know an awful lot less than me, and yet choose to speak on the O&G sector in Nigeria with this sense of misguided confidence

THE ‘HERE, READ THIS’.

The worst of all, is when I see people say: NIGERIA IS AN OIL ECONOMY.

This is particularly true when people drop it like a bomb on a prevailing post or discussion, as if it is expected to explain everything. It is a sort of ‘go to’ statement that is expected to serve as an instant and final conclusion. Banking, Finance, and Shipping/Logisitics leaders tend to be frequently guilty of this, and they are often not Nigerians.

And this is where I like to have something saved as a URL that I have written before, because I can just say: ‘Here read this’.

I suppose everyone is entitled to their opinion. But I’m sure many reading this can identify with this experience… Someone is there, dropping something as if they are having a ‘Eureka Moment’ or they have just found the ‘Holy Grail’, and we are there having divergent ‘moments’ – the exasperated ‘no its not’ moment or the ‘no **** sherlock’ moment… or the moment when someone feels they are completely enlightening you through an expression of thought leadership by Steve Jobs…Elon Musk…Bill Gates… Richard Branson … (non exhaustive list)… which you are seeing for the thousandth time.

So let’s unpack this ‘Nigerian Oil Economy’ (I will try to keep it simple, and won’t mention the challenges and narratives of all players).

THE STARTING POINT

Shell first came to Nigeria in 1933 but didn’t find commercial success until 1956 at Oloibiri, Bayelsa State. Other foreign companies to pile in the initial wave were Chevron, ExxonMobil, Texaco and TOTAL.

Nigeria joined OPEC in 1971 and created NNPC in 1977.

THE FOREIGN ENTOURAGE

Moving on, we had a development in both the specialist security space and the specialist recruiter space. Risk and personal safety indices were developed globally by so called International Security Experts.

These usually overplay or embellish risk. How often have you been going about your daily life as normal with nothing happening, but you turn on a global media channel and you hear all this ‘stuff’ going on, and you wonder… is there a parallel universe these people are reporting on? .. because I am here, and I am not seeing this thing they speak about.

Understand that security services don’t make money guarding high value installations in safe countries. It is in their interests to talk-up risk.

On the back of security risk, recruiters in the O&G sector created a phenomenon known as the Expatriate Hardship Rating System. This numbers countries from 1 (lowest hardship) to 4(highest hardship).

For sure, instability in Nigeria has risen significantly over the last few years, however, Nigeria has always had an Expatriate Hardship Rating of 4.

If any O&G expatriate specialist recruiter active in Nigeria, up to around 2010 is asked…and they are honest… they will concur this system existed. Brunel, ECL Global, NES Global, Orion Engineering, RHL, Swift, TED Recruitment and TRS were all around for the period.

Though not significant at the time because expatriates as a percentage of the total O&G workforce was extremely low, this was the start of a rising overhead dynamic for the Nigerian O&G Sector.

Tony O. Elumelu, C.O.N’s Heirs Holdings (see lead photo) bought most of the holdings of Shell

NAPIMS and NIGERIAN CONTENT LAW

When the Nigerian Content Law was being formulated in the mid 2000’s expatriate numbers in the industry were low. It seemed that FGN did not have the political will to deal with the biggest equality issue in the industry, that of tribalism.

Nigerian Content Law was a distraction.

They didn’t want to deal with the biggest elephant in the room. Resources are limited to land, or coastal waters of specific states, however a large number of the Nigerian employees given jobs in the industry were not native to the states producing fossil fuels.

The main bone of contention in equality in O&G employment is tribal proportional representation in individual local areas on land or in offshore extractions based on which state holds the closest shoreline.

The Ijaw tribe which is primarily in Delta State but also has some presence in Bayelsa, Edo, Cross Rivers, and Rivers states feel particularly aggrieved. They form the mainstay of the paramilitary group known as the Reformed Niger Delta Avengers.

While over time, some expatriate positions have been weeded out of the system causing overhead savings, unfortunately the NAPIMS structure and its impact on the sector over time, including political appointments to NNPC and NLNG have resulted in deadweight roles ballooning costs and many positions being retained close to, and some even exceeding expatriate rates although there is no ‘hardship rating’ argument to support this. O&G parastatal employees in Nigeria are paid 4-5 times the salary of their counterparts in military, educational, health care, civil service and other parastatal organisations.

Since their sector is actually making a loss a lot of the time, there is absolutely no justification in their pay being enhanced over that of comparable state employees in different sectors.

They also tend to get paid promptly, unlike their military, civil, state health care and parastatal counterparts who are often waiting months for pay and in a few cases years in arrears.

NAPIMS, Nigerian Content Law and NNPC/NLNG in the NAPIMS-NCL era have risen the overhead of extraction rather than reducing it, while the Ijaw and RNDA don’t feel any less aggrieved than they did before these changes were introduced.

Should this get ported to LinkedIn, it may attract some dissenters. Should that happen, I will make a ‘wild prediction’ they won’t be Ijaw.

SHIFTING SANDS AND GLOBAL DEMAND

As early as 2009, something new was happening in the global energy business. The Canadians developed new fracking techniques which can translate low quality primary extraction product…certain Oil Sands, Shale types, and some heavy oils and bitumens, into secondary high value raw material for further refining.

This is generally product that is cheap to extract, fairly abundant and hitherto ignored for higher value deposits. The technology has been licensed widely to other countries and companies and has been partly responsible for translating North America from a net importer of fossil fuel to a net exporter.

Operating costs are low though initial investment is high, but this is continually being improved. Progress has taken some years to filter down to market impact.

By comparison, Nigerian Crude is generally high value product at inception. Extraction is expensive however and when the overall cost of sales associated with sidestepping industrial disputes, localized terror groups, political activists, ‘inducements’ needed to avoid political/tribal obstruction, logistics, legal and other services, then the cost of getting it to market is high.

Professor Pat Utomi relates an experience where an Oil Company could not get the building of a free school accepted, without additionally ‘greasing other palms’

Separately, there has also been a huge surge in the use of renewable energy, which is now establishing itself as a real and credible alternative to fossil fuels. This is not just happening in mature economies. This is happening in Africa!

Kenya’s public power generation already produces 76% of all national grid power from renewable sources – being 73% hydro and 27% Geo Thermal. Its Civil Leadership in state use of renewable solutions far exceeds that of the top four leading countries by GDP on the continent. .. Nigeria produces only 21% while South Africa is a paltry 1%; nevertheless, energy from renewable sources is causing real reductions globally in the need for fossil fuels.

The ‘mood and appetite’ for continued investment in O&G extraction in the last decade outlived the business case for doing so. Now various businesses having weathered the storm are on the precipice of a bull market in Nigeria but some have not the mood, appetite, nor perhaps the funds to invest.

All conglomerates with a heavy exposure to O&G have experienced major contraction – Orlean Invest and Jagal have experienced difficulties.

MPH Global, an oil services multidisciplinary consultancy and recruitment agency of French origin with strong exposure to Jagals’ partner, TOTAL, dropped its workforce by about 75% and sent almost all its expatriates home in 2016. It did this across some other emerging markets as well, a few years later, it was gone.

There is the well known story about Femi Otedola, the former CEO and Owner of Zenon Oil, who had vessels filled with diesel at sea before the crash in retail product, having only a fraction of its value when decanted at Nigeria. He is said to have undergone extensive liquidation including selling off holdings in Cadbury, Coca-Cola, Nigerian Breweries, MTN, Unilever, Nestle and Guinness, and after a restructuring plan, started Forte Oil.

Everything seems so easy in hindsight.

There will always be some market for fossil fuels but it is likely to be a see-saw market.

Artificial intervention directed at Oil Price management when attempted is short lived and largely ineffective.

Global primary extractors were once prepared to lose money on the downturns that particularly depressed Nigeria based viability purely to control capacity to strengthen their position on global markets.

With the advent of North American self sufficiency and renewable technologies, they are not willing to do this anymore.

Some primary extractors have been driven out of the Nigerian market, with only hire services, port based reserve services, and port management services remaining. China’s Sinopec Group has already hired BNP Paribas to sell its oil business in Nigeria and Gabon.

With Chinese investment dominating the new 20m draft deep port at Lekki and the two planned ones (18m and 16m) in the South East, it’s probable that Oil Majors will not stay in charge of port activities long term.

THE INTERMEDIATE GOODS EXPORT MIRACLE

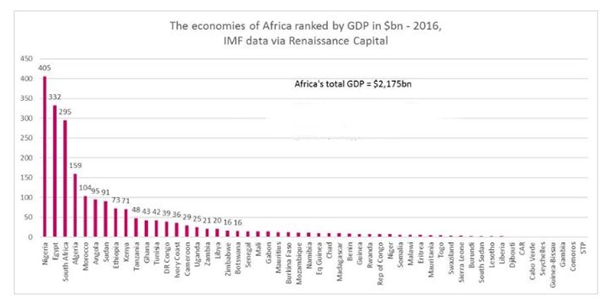

Despite the difficulties and market challenges, Nigeria is the biggest country by GDP in Africa and 78% of GDP of its economic union ECOWAS, a dominance unequalled by any single country in any economic union in the world.

This leadership has been sustained though all challenges since first achieved in 2014.

The midst of Nigeria’s last decade oil downturn… 2016. It’s lead against other African Nations was buoyed by its Intermediate Goods Exports. Saying Nigeria’s Economy is dominated by O&G is being simplistic.

The traditional heartlands of Lagos industrial activity, typically the ‘mainland’ areas of Oshodi, Orile, Isolo, Muchin, Apapa, Agege, Ikeja, Ilupeju, Ajegunle etc, have become congested and there is insufficient ‘brownfield’ sites available for modern industrial expansion and new projects.

Since the turn of the millennium, and with gathering pace in the last decade almost all new industrial projects for West Nigeria have been built on ‘greenfield’ sites in the most northerly reaches of Lagos State, Badagry, Abeokuta and Ibadan expressways and up into Ogun and Oyo states.

Nestles ‘Flowergate’ factory at Sagamu inaugurated in 2011 is over twice the size of its facility at Agbara. Unilever has just completed a massive extension project to its existing facilities also at Agbara. Proctor and Gamble, which already has two facilities at Ibadan have also opened a new factory two years ago at Agbara.

Though what is even more profound is not the progress with mature MNC Conglomerates of European or North American origin, but the myriad of smaller but significant operations being started up by entrepreneurs from other emerging markets and Nigerians indigenes in Edible FMCG, Household Goods, Pharmaceuticals and Plastics.

In anticipation of increased business from some of these industries the #1 Flavour and Fragrance House in the world, Givaudan has expanded its Lagos operations, while the #2 Firmenich last year ended its long history of working with locally established partners such as the Turkish, Orkila Chemicals, and the local group, Mikado, and established their own state of the art R&D and production.

Intermediate Goods exports built on the back of light manufacturing growth kept Nigeria going through the loss making years of the O&G sector.

However since then, unfavourable unpegging against the dollar, distribution and storage disruption on the back of #ENDSARS, and a clash of FOREX policy with disintegrating local backwards integration partnerships due to rural terrorism and unrest, has all but wiped out the intermediate goods export profile.

Femi Otedola, who rose a new O&G fronted conglomerate out of the ashes of the one he lost, and made it all look like a Sunday afternoon stroll.

IS THERE A SOLUTION FOR O&G ?

I’ve written at length about the need for Nigeria to change things that influence its FDI (Foreign Direct Investment) success, especially improving its ‘Ease to Do Business’ ranking.

It’s not the 1960’s anymore. investors don’t need to physically spend time and effort on ground in a distant market to gather data, and there are infinite sources of data and informed opinion accessible fairly cheaply online. This allows investors to shortlist different countries creating a quite narrow group of global finalists without first setting foot on ground anywhere.

At the moment , if Nigeria PLC was a job applicant, it isn’t even getting past the ‘ATS’.

‘Dangote Refinery. Dangote Refinery…. It is looking like a very bad call. Yes, unborn tomorrow but died yesterday!’ – Ndubuisi Ekekwe – With the refinery in financial trouble and the looming threat of administration before it goes live, it makes Emefiele’s justifications for the end of fuel subsidy next year seem like a fairy tale…. But would Dangote really have got the largest single train column in the world, made by SINOPEC if they were still contesting exploration in the Group’s backyard? hmm

It’s a real problem when foreign entities cant even give something away for free, without them costing them money.

Strong local arms and shoulders, however, sometimes have ways of getting things done foreign O&G cannot.

With Tony O. Elumelu, C.O.N’s holding company having bought much of Shell, and if other big Nigerian names can follow suit, there is a good chance that we will have a group of strong willed individuals with enough muscle to cut through some negative cultures that surround the business, so that it can at least break even amidst the worst of down turns in the future.