The Theranos trial kicked off recently with Elizabeth Holmes at the risk of facing more than a decade in prison. For those who don’t know Theranos; Theranos was a health tech company founded by Stanford University dropout Elizabeth Holmes, Elizabeth Holmes claimed that the technology Theranos was building could drastically reduce the amount of blood needed to perform blood tests on a patient, and the turnaround time required to get results.

Holmes claimed that with a single drop of blood pricked from a finger, her technology could run more than 240 different blood tests on a patient. This was, however, a flat-out lie – her technology didn’t work, patients got inaccurate lab test results, and on the occasion the person taking the test was influential (i.e board members, etc) she would send blood samples to a normal lab with normal equipment for testing.

The purpose of this post is not to throw shades at Theranos, the purpose of this post is to highlight that with less than a thousand employees and without a working product, Elizabeth Holmes was able to raise more than US$720 million, and Theranos was valued at US$9 billion. For contextual purposes – a company without a working product in 2016 was worth 6 times what Zenith Bank is worth today, almost 2x the market capitalization of MTNs MoMo business, and about US$2 billion more than Dangote Cements market capitalization (a company doing about N690.5 billion (US$1.3 billion) in half year revenue). When you realize that all this is magic money that never existed, you’ll realize how crazy this is.

SUBJECTIVE VALUATIONS

The past couple of months has seen a plethora of technology companies here in Africa raise capital from various sources, and as expected the arguments over who is overvalued and who is not has come up.

Kuda raised US$55 million in August and is now valued at US$500 million. While I believe Kuda is a great product (I was just encouraging a friend of mine to switch his savings from FirstBank who according to him turned his N100,000 in 6 months into 98,880 to Kuda), I do not believe they are worth US$500 million.

Valuations are largely subjective – spending roughly US$70 for show tickets to attend a music concert is largely a complete waste of both time and money to me, this is however not the case for a lot of people, and while spending a similar amount of money on a training program may be more meaningful to me as a person, there are others who will scoff at such a choice (which is also reasonable).

WeWork was worth US$47 billion in 2019, then in a bid to go public in September 2019, they released their S1 filings and when the world saw how badly the firm was being run – Adam Neumann (Founder/CEO) was fired (with a nice US$1 billion compensation package off course), more than 8,000 people lost their jobs (without a nice US$1 billion compensation package off course) and the company slimmed down its valuation to a now modest US$9 billion. Why was WeWork valued at US$47 billion? Because the almighty Masayoshi Son (CEO of SoftBank) thought it was and putting his money where his mouth is subsequently pumped more than US$18 billion into WeWork.

SoftBank led OPay’s recent US$400 million raise that valued OPay at US$2 billion. I expect a couple of OPay executives to change cars these coming weeks, as far as I’m concerned, the reward for hard work is no longer more work, the reward for hard work is now a brand new Mercedes Maybach, a couple million dollars in vested sweat equity, and a nice 5 bedroom duplex in Banana Island, but I digress.

THE INFORMAL MARKET

The biggest opportunity to create wealth in Africa is in the informal market, the biggest opportunity to create wealth in the fintech space in Nigeria is by enabling financial inclusion.

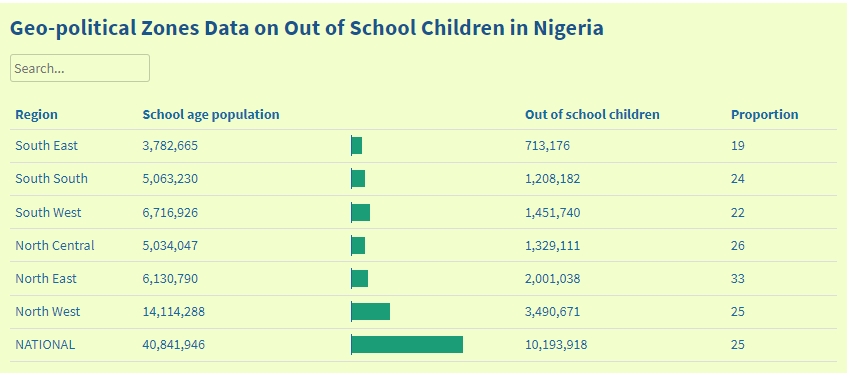

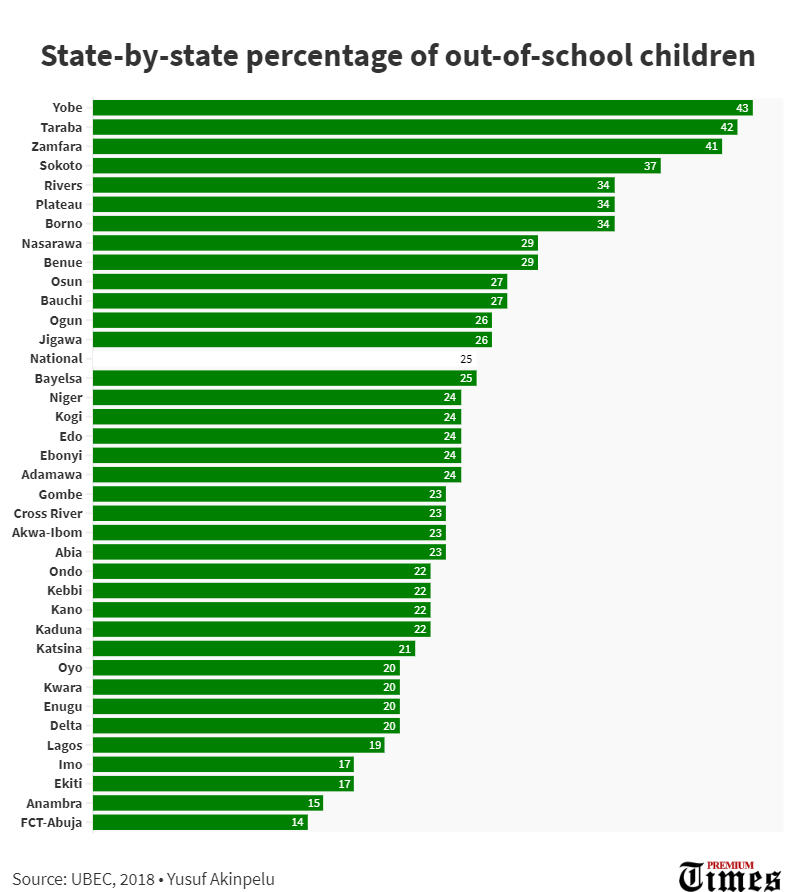

According to data from EFInA, more than 35% of the Nigerian populace is financially excluded. One of the core goals of the Central Bank Of Nigeria apart from its drive to stabilize the naira (a drive that has seen it collide with and knock out cryptocurrency startups, Bureau De Change operators, and the four main wealth tech startups in Nigeria) is to increase financial inclusion.

Increasing financial inclusion through digitization is a great opportunity to increase (and/or justify) the market capitalization of most fintech players in Nigeria.

Jumia’s elevator pitch (or part of its elevator pitch) is a page on the Jumia group website where it outlines the vastness of its opportunity – a total addressable market (TAM) of 600 million people of which it has already captured 6 million people – just 1% of its TAM, which is enough data to give any investor Goosebumps.

According to the IMF, the Nigerian informal market makes up more than 65% of the total GDP of the nation, in other words, almost 65% of the WTBM (Wealth to be made) in Nigeria is with the people who are off-grid, partly or fully financially excluded and are definitely not on Twitter.

The biggest companies operating in Nigeria and Africa understand this and are taking cognizance of these opportunities. Dangote Cement released its H1 2021 unaudited financial results, and its H1 2021 Revenues were at N690.5 billion (US$1.38 billion), a 44.8% YoY increase from H1 2020. For context purposes, this is more than half the Federal Government’s allocation for the Ministry of Defense in the 2021 budget.

Dangote Cement is used by both firms building multi-billion naira projects across Nigeria and Africa, and individuals building small roadside stores. The value of the business is its ability to create value for all market classes and sizes in the Nigerian economic strata. You can read my article on Market Sizes and Classes for more information on this.

Dufil’s group Indomie Noodles (who I have once referred to as the real ’30 billion for the account’) recorded 2020 revenues of N226 billion (US$452 million). Indomie makes up more than 55% of Dufil groups business and is a great example of a business that touches all economic strata. Aje – Butter kids in Lekki phase 1 eat Indomie (the one that resembles the image on the pack), the same way Aboki’s on the Lagos mainland eat Indomie (Mishai).

MultiChoice’s GOTv is another great example of this; with less than three thousand Naira a month you can watch Prashant from Zee World Break Rashni’s heart and walk away in slow motion while an action movie-themed soundtrack plays in the background and everyone throws suspicious glances at each other. When I was at the university, I had a neighbor who was an elementary school driver while his wife sold kerosene. They had GOTv in their house – fortunately, his wife didn’t watch Zee World. Multichoice recorded N221.3 billion (US$442.6 million) in revenue from its Nigerian division alone in 2020.

MTN Telecommunications license is more than just an operating license, it’s a license to print money, and this is exactly what MTN is doing. With revenue of N1.346 trillion (US$2.6 billion) in 2020 alone, MTN is one of the largest firms operating in Africa. MTN serves a broad market segment, consisting of Naira multi-billionaires driving sports cars to church on Sunday morning to village farmers riding bicycles to the farm on Tuesdays. MTN serves a very large market segment, and this is one of the reasons they’ve been able to extract so much monetary value from the markets they operate in.

So while most of the largest companies in Nigeria and Africa have been able to build and design systems and products that allow them to create value for a huge and wide segment of the market, most core technology firms have not.

In most of the developed world, technological innovation is designed to make life easier and simpler for people. It is this mindset that gives birth to solutions like Bird (scooter hailing company), Clubhouse, Peleton, and the likes. These are companies that make life easier for people as against solving critical and life-changing problems for people.

A good number of technology startups in Nigeria today are doing almost the same thing. The lofty valuations most African startups command today is based largely on the market size premise that permeates the African narrative (Africa is a huge market), however, most of these businesses do not make the most of these market size by targeting those indigent communities where the majority of these opportunities lay, most are fine with targeting more urban confines where technology innovation is more quickly and easily embraced, and profits can be generated much more quickly as against where the real numbers lie, and the reasons aren’t far-fetched; it’s usually expensive to serve this specific market class, so what technology startups do is when they’re done with Lagos, they expand to Ghana, and then to Kenya and maybe South Africa. In other words, they taste the frothy foam at the top of the soda but are too afraid or cautious to go into the depth of the bottle itself.

FINANCIAL INCLUSION AND INCENTIVES

When I was growing up, my mum would incentivize us to help around in the kitchen by promising me and my younger brother pieces of meat if we helped her grind tomatoes in the kitchen. We didn’t like it, but considering we’d get a free piece of meat for doing less than five minutes of work, it wasn’t a big deal. Incentives are powerful.

The problem with financial inclusion in Nigeria isn’t a lack of technology, the problem with financial inclusion in Nigeria is a lack of incentives. The Central Bank herald’s financial inclusion as one of its key missions, however, the DMBs (Deposit Money Banks) its core partners on this vision couldn’t care less.

Banks have little or no incentive to push for financial inclusion, and there’s a very good reason for that; because while banks can talk about being mission-driven and focused, and Fidelity Bank says “we are Fidelity, We Keep our Word” – of which their word is only kept if they keep your money, the real truth is that the banks are in it for the money, and if it isn’t making money to a bank, it isn’t making sense to the bank. On average, Nigerian banks make a good majority of their income from their corporate customers, and while the top 5 banks in Nigeria (FUGAZ) made more than N67 billion (US$134 million) from their internet businesses in H1 2021 alone, it still dwarfs what they cumulatively made from their corporate businesses, primarily servicing loans and the likes.

Chasing financially excluded people makes little or no sense to a DMB (Deposit Money Bank), because even if a hitherto financially excluded person were to open a bank account, the account really just becomes a collection account (an account that receives money and has a sizable amount of its content withdrawn in a short period of time), and used primarily for collecting money and withdrawing the money to be used in cash. So, if the bank can’t make any serious money from this person because they aren’t a corporate client, and they do not subscribe to their electronic business, then it makes no sense to spend marketing dollars and resources to bring these people into the fold. When Zenith Bank (or any other bank I bank with) looks at me, what they see is N600 a month they can make in cumulative bank charges of all kinds, including the N50 they charge me for card maintenance quarterly (a card that I keep in my wallet and maintain myself).

Fintechs also have very little incentives to push for financial inclusion, because while the banks may see it from a profit point of view, fintechs think differently; while having a huge number of financially excluded people looks nice on a pitch deck and indicates a huge market opportunity, the fact that KYC standards require fintechs to verify users with BVNs and only DMBs can issue BVNs means that most fintechs cannot bring people directly into their folds as they may have to pass them through banks first (who may likely take a cut of their users). Even MFBs like Kuda can’t offer BVNs to their users, so going through the stress of bringing people on the grid only to have a bank capture some of your customers doesn’t really sound like a smart idea.

CBN AND TELCOS

Last week I was privileged to be in a session with one of the ladies that kick-started MPESA. Before this I knew very little about MPESA, except that MPESA was the leading mobile money operator in Kenya, however, after that session, I realized that while MPESA has played a huge role in contributing to Kenya’s 82.9% financial inclusion rate, MPESA is such a monopoly that even Safaricom (Owners of MPESA) operate under a special license from the CBK (Central Bank of Kenya). MPESA is more powerful than a large number of Kenya’s banks and is an overarching monopoly that can stifle innovation in the Kenyan mobile money space.

So while everyone keeps criticizing the Central Bank of Nigeria for not adopting a telco-led drive to boost financial inclusion, avoiding the occurrence of an MPESA like monopoly is probably one of the reasons they have decided not to do so.

However, CBN doesn’t hate telcos, so they decided to give them a leg in the race by creating a PSB (Payment Service Bank) license they could use to offer some degree of financial services. To the best of my knowledge, only 9mobile (9PSB), Glo Mobile (Money Master PSB), and Hope PSB have PSB Licenses.

However, PSB license privileges are so terse that PSBs aren’t allowed to offer loans. Loans are one of the easiest ways to bolster financial inclusion because while excluded people may not necessarily see the need to adopt a new payment system besides cash, they’re more likely to adopt digital methods to access credit. So while the CBN has given the telcos a leg in the race by creating a PSB license category, by withdrawing their ability to grant loans, the CBN has essentially broken that leg.

CONCLUSION

If the regulatory environment can incentivize more fintechs to actually take it upon themselves to bring more excluded people into the fold, as against not caring and leaving it to the banks (who also do not care and are not doing anything about it), with the over 38 million financially excluded people in Nigeria alone and over 90 million financially excluded in Africa, chasing these financially excluded people may turn out to be a game-changer and end up justifying, and even elevating the market valuations of a good number of fintech players in Nigeria.

Inspired By The Holy Spirit

P.S. Wave just announced its US$200 million Series A raise giving the start-up a Post-Money Valuation of US$1.7 billion. For contextual purposes, both Facebook and Google cumulatively raised less than US$50 million in their Series A rounds (Facebook raised US$12.7 million in its Series A, while Google did US$25 million). Wave is a Senegalese-based fintech in the Mobile Money space. One of Wave’s core goals is to bolster financial inclusion. As long as Wave is targeting the financially excluded to bring them on the grid, I do not think Wave at a US$1.7 billion valuation is overvalued.

Like this:

Like Loading...

")