Artificial intelligence has rapidly evolved from a niche technology into a central feature of digital entrepreneurship. On Facebook, AI educators, digital marketers, and business coaches increasingly present AI as an essential business companion rather than an experimental innovation. Their posts do more than introduce new tools. They shape how entrepreneurs understand technology, opportunity, and success. Examining these messages through the framework of the AI we use, the AI we gain from, and the AI we discard reveals not only the technologies being promoted but also the values, assumptions, and business practices that accompany the growing AI economy.

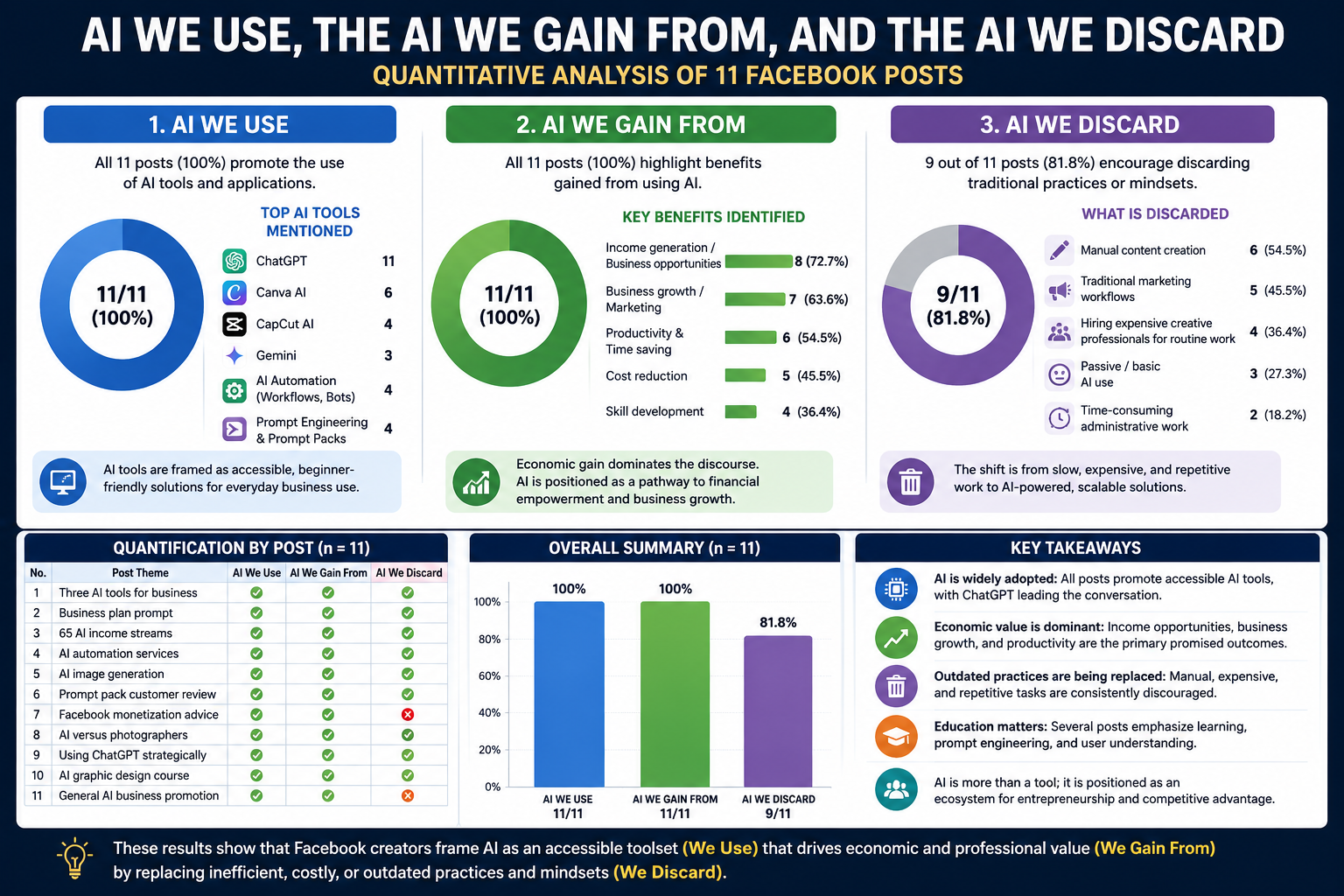

The first dimension, the AI we use, focuses on the technologies that creators encourage their audiences to adopt. Across the Facebook posts, accessible applications such as ChatGPT, Canva AI, CapCut AI, and Gemini dominate the conversation. These tools are recommended for writing marketing copy, designing promotional materials, editing videos, developing business plans, generating realistic product images, and automating routine business activities. Rather than emphasizing technical complexity, creators consistently portray these platforms as beginner friendly solutions that anyone with a smartphone or laptop can start using immediately. The message is reassuring. AI is no longer reserved for software engineers or technology companies. It has become a practical resource for small business owners, freelancers, and aspiring entrepreneurs.

Yet these creators rarely stop at demonstrating how AI works. Their central message quickly shifts toward the second dimension, the AI we gain from. In these posts, AI is presented as a pathway to economic opportunity, increased productivity, and business growth. Followers are encouraged to see ChatGPT not simply as a chatbot but as a virtual business assistant capable of writing proposals, creating content, generating business ideas, and supporting strategic planning. Canva AI becomes more than a design platform because it promises to eliminate the cost of hiring graphic designers for routine marketing materials. Similarly, CapCut AI is framed as a way to produce professional video content without investing in expensive editing expertise.

Economic empowerment is the dominant narrative. Several creators promote AI as the foundation for entirely new careers. Posts advertising AI automation services argue that businesses are actively seeking professionals who can build automated content workflows, customer support systems, email sequences, and data reporting solutions. The emphasis is not on replacing human workers entirely but on positioning AI knowledge as a premium skill that organizations are willing to pay for. In this narrative, financial success depends less on simply using AI and more on understanding how AI can solve real business problems.

The same perspective appears in promotions for prompt engineering, AI image generation, and digital products. Instead of selling software, creators increasingly sell knowledge about how to maximize AI tools. Prompt packs, AI courses, and automation training become products in their own right because they promise to transform ordinary users into professionals capable of generating income. AI therefore becomes both the product and the mechanism through which new products are created. Knowledge of AI is treated as an economic asset that can be packaged, marketed, and sold.

The third dimension of the framework, the AI we discard, offers perhaps the most revealing insights. These Facebook messages consistently encourage audiences to move away from traditional business practices that are portrayed as slow, expensive, or inefficient. Hiring photographers for every marketing campaign, paying graphic designers for routine promotional materials, manually responding to customer inquiries, and spending hours drafting business documents are all presented as practices that AI can significantly reduce or replace. The creators argue that businesses can achieve similar outcomes more quickly and at a fraction of the cost by integrating AI into their operations.

However, what is being discarded extends beyond specific business activities. Many of the posts challenge a mindset rather than a technology. Several creators criticize those who use ChatGPT only to answer simple questions or generate generic social media captions. Instead, they encourage audiences to think strategically by viewing AI as a business system capable of creating long term value. Success, they argue, belongs to those who integrate AI into their workflows rather than those who treat it as a novelty. This shift reflects a broader transformation in digital entrepreneurship where competitive advantage increasingly depends on combining AI with business strategy instead of relying on AI alone.

Despite the optimism that characterizes these posts, the discussions reveal important limitations. AI is consistently portrayed as a source of efficiency, creativity, and financial opportunity, yet relatively little attention is given to its risks. Questions surrounding data privacy, copyright ownership, algorithmic bias, misinformation, platform dependency, and workforce displacement remain largely absent. Likewise, the continuing importance of human creativity, ethical judgment, critical thinking, and industry expertise receives limited discussion. The impression created is that technological capability alone is sufficient for business success, even though sustainable competitive advantage often depends on qualities that AI cannot fully replicate.

One post provides an important exception. A creator recounts how a customer left a negative review after purchasing an AI prompt pack, only to discover that the customer misunderstood the nature of the product and did not know how to access or use it. Rather than blaming the technology, the creator recognized that the problem lay in inadequate user understanding and responded by developing a step by step tutorial. This episode highlights an often overlooked aspect of AI adoption. Technology alone does not create value. Users must also possess the knowledge and confidence to apply it effectively. AI literacy therefore becomes just as important as AI availability.

Generally, the Facebook posts examined reveal far more than promotional tactics. They demonstrate how artificial intelligence is being constructed as a symbol of entrepreneurial ambition, economic mobility, and digital transformation. The AI we use reflects the growing accessibility of intelligent technologies. The AI we gain from captures the financial and professional opportunities that creators associate with these tools. The AI we discard illustrates the gradual replacement of traditional workflows and outdated assumptions about how businesses should operate.

As AI becomes increasingly embedded in everyday business practices, the conversation must evolve beyond enthusiasm alone. Business leaders, educators, and policymakers should encourage not only widespread adoption but also responsible and informed use. The future will not belong simply to those who embrace AI. It will belong to those who understand where AI creates value, where human expertise remains indispensable, and how technological innovation can be balanced with ethical responsibility.