I have read Jumia Form F-1 which it filed with the U.S. SEC as part of the process of becoming a public company in America. What we knew as Africa Internet Holding GmbH transmuted into Jumia Technologies AG in January 2019. Certainly, it is a better branding since most know Jumia and the obscure AIH would have confused many in the market.

We have historically conducted our business through Africa Internet Holding GmbH and its subsidiaries, and therefore our historical consolidated financial statements present the results of operations of Africa Internet Holding GmbH. On December 17 and 18, 2018, our shareholders resolved upon the change of our legal form into a German stock corporation (Aktiengesellschaft) and the change of our company name to Jumia Technologies AG. The change of our legal form and company name became effective upon registration with the commercial register of the local court (Amtsgericht) in Berlin, Germany, on January 31, 2019.

Here are the major sections for players in the African ecommerce space to read very well. Largely, what Jumia is saying is this: we have incurred significant losses since inception and there is no guarantee that we will achieve profitability in the future. But over the years, because we have consistently raised external capital, we have been moving forward but where we are unable to bring more external capital, there will be huge risks. Jumia in this section makes it indirectly clear that old Konga investors just gave up on Konga by not injecting fresh capital as that is what everyone is doing. Naspers which founded Kalahari had given financial sustainability as a key reason whenever it closed any of its ecommerce platforms in Africa. The decision to close is based on deciding not to inject new capital into the business.

Explaining further, Jumia notes thus – our markets pose significant operational challenges that require us to expend substantial financial resources and we have no reason to think these challenges will disappear. It then listed a laundry list which mirrors a piece I wrote in Harvard Business Review where I made it clear that winning the ecommerce sector will involve losing tons of money as there is nothing electronic in the sector. Yes, the marginal cost paralysis does not reduce with scale and until we have a solid logistics system, it will be a hard business. You come and lose money, and then you exit.

Risks Related to Our Business, Operations and Financial Position

We have incurred significant losses since inception and there is no guarantee that we will achieve or sustain profitability in the future.

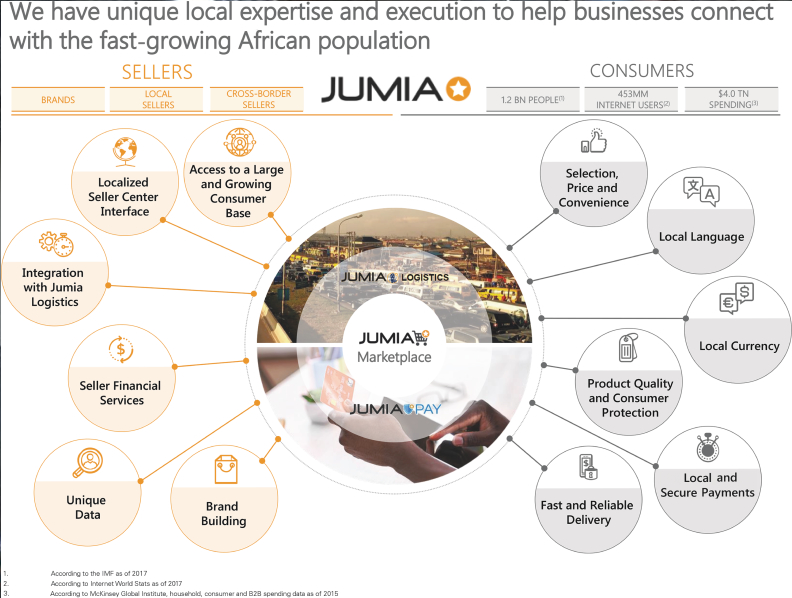

Jumia operates a pan-African e-commerce platform. Our platform consists of our marketplace, which connects businesses with consumers, our logistics service, which enables the shipping and delivery of packages, and our payment service, which facilitates transactions among participants active on our platform. We primarily generate revenue from commissions, where third-party sellers pay us fees based on the goods and services they sell, and from the sale of goods where we act directly as seller. Our revenue is, however, not sufficient to cover our operating expenses. Accordingly, since we were founded in 2012, we have not been profitable on a consolidated basis. We incurred a loss for the year of €165.4 million in 2017 and a loss for the year of €170.4 million in 2018. As of December 31, 2018, we had accumulated losses of €862.0 million.

There is no guarantee that we will generate sufficient revenue in the future to offset the cost of maintaining our platform and maintaining and growing our business. Furthermore, even if we achieve profitability in certain of our more mature markets, where e-commerce is growing rapidly, there is no guarantee that we will be able to break even and achieve profitability in other markets, where e-commerce adoption is slower. We expect that our operating expenses will continue to increase as we intend to expend substantial financial and other resources on acquiring and retaining sellers and consumers, growing and maintaining our technology infrastructure and sales and marketing efforts and conducting general administrative tasks associated with our business, including expenses related to being a public company. These investments may not result in increased revenue growth. If we cannot successfully generate revenue at a rate that exceeds the costs associated with our business, we will not be able to achieve or sustain profitability or generate positive cash flow on a sustained basis and our revenue growth rate may decline.

If we fail to become and remain profitable, this could have a material adverse effect on our business, financial condition, results of operations and prospects.

- We rely on external financing and may not be able to raise necessary additional capital on economically acceptable terms or at all.

- Our markets pose significant operational challenges that require us to expend substantial financial resources.We operate in emerging markets in Africa. While we believe that our markets offer opportunities for an e-commerce company, they are also characterized by fragmented and largely underdeveloped logistics, delivery, and digital payment landscapes, which can differ significantly in the consumer markets in which we operate. This underdeveloped infrastructure restricts and complicates the movement of people and goods, which may make our delivery service too expensive or our delivery times too long to effectively compete with offline stores, in particular outside of main urban centers. Underdeveloped infrastructure may also limit our growth prospects by obstructing access to potential consumers. Lack of an established, secure and convenient cashless payment system in many markets also poses significant challenges for sellers. From our experience, we believe that a large percentage of our consumers either do not have a bank account or do not trust online payments, which is why cash on delivery is still the preferred payment method used by our consumers.

In order to overcome the challenges posed by our markets, we have had to develop significant logistics, delivery and payment infrastructures, which include, for example, the operation of warehouses and drop-off centers, the integration of third-party logistics providers, the establishment of our own delivery and last-mile delivery fleet in certain cities, the design of our independent technology platform and the provision of unconventional payment options. These factors make our operations more complex than those of similar businesses in more developed markets and may place a higher risk on us, for example, due to a higher number of failed orders, the risk of fraud or otherwise. The costs incurred by us to meet these challenges have, and may continue to, put a strain on our financial resources, may be unjustified in light of the benefits they bring us and may make it challenging for us to reach profitability. In particular, there is no guarantee that the markets in which we currently operate will prove to be as attractive as we currently believe them to be, which could have a material adverse effect on our business, financial condition, results of operations and prospects.