Some cities in Nigeria are experiencing acute fuel scarcity. It does happen in our great nation. It is a reminder that our systems are still at infancy. If not, there is no reason to run into troubles distributing fuel when the citizens are ready to pay. And the problem is not necessarily pricing: some are ready to pay at any price. The problem is Distribution & Logistics. Yes, the same issue that causes problems for ecommerce companies in Nigeria.

For ecommerce, you look at the marginal cost driven by geography. That marginal cost is composed of transaction and distribution costs. But transaction cost is typically negligible since it cannot be eliminated, and is not tied to distributive geography. But distribution cost is where the game is won, and it requires having a great process with solid pillars.

Though operationally it is at the lower phase of the chain, distribution in Nigeria is the upstream because that is where the knowledge base is uppermost, and the highest value could be created in ecommerce. The ecommerce portal is downstream; anyone can make a fancy site with nice SEO. The man that builds the best logistics system for the ecommerce companies would have more leverage than the sites.

The lesson: you have the goods in the warehouse but you cannot deliver to the customers because the distribution is broken. You cannot leapfrog that challenge. You have to solve it to have a great ecommerce operation.

That is the same issue with fuel scarcity. Fixing this must be uniquely Nigerian, and it would require a new architecture. I would be speaking in NNPC this week as we work on how to fix this national challenge. My focus would be looking at technologies that would enable our leaders to solve this problem. Please be guided on what you share; I am good in picking ideas from comments.

There is something I like about most U.S. banks: they combine retail and advisory services in branches no matter how small the branch is. When you walk in, you get a picture of a bank that is ready to collect your deposit and also discuss mortgage, lending, education funding, savings, etc right before you. The tellers are there while the advisors are in their cubicles talking to clients.

Sure, we do that in Nigeria in many ways, but the advisory part does not seem to be what any client can have access to. In other words, we make it look like you just come here to make deposit, and unless you have truckloads of cash, the advisory aspect would be away from you.

In my opinion, that is wrong. If branch staff members are not looking at how to help clients deepen their businesses and lives through advisory services, they would not strengthen the relationships necessary for future growths.

I recall a call I got from my U.S. bank many years ago. We had done a project for a Swiss businessman in Africa. They paid to my U.S. firm. The next day, the bank sent their staff to meet me, to understand how they could help the business, and if we plan to keep the cash, how the bank could make it work for us. As we discussed, they presented scenarios based on cashflow in our business. I was impressed that they did not see us as a number, but a firm, they could develop deeper relationships.

Till today, none of my Nigerian bankers have come to us with any conversation of such services. The message has been “the account is doing well” which means that inflows are coming. There is a service gap in our bank and we need to fix that.

Imagine if we can have in each mega bank branch a Future Bar (think of 9Mobile Geek Bar or Apple Genius Bar for dealing with your phone issues), but here the focus would be to discuss investments and advisory services available to young professionals, as they begin their careers. Yes, we are not in the phase to use AI to drive such processes online. But we can build structures to get the young people excited to have financial plans.

Many people in Nigeria especially in the informal sector usually begin great but some run into troubles due to lack of financial planning. Visit your village and you would see people that started great businesses, post-apprenticeships from their masters, but today are struggling in villages. Their banks could have helped them when their failed businesses were booming. Yes, besides the retail-first strategy, we must add advisory services to create more values for clients.

In a short entry by Guardian NG, a Google engineer explains the key challenges before Nigerian startups. The list includes the usual factors plus an important one: scalability, mentorship, finances, connectivity, market size and changing consumer needs. That last one – changing consumer needs – is the most important factor for any startup. Indeed, for you to create a new basis of competition, i.e., to become disruptive in your sector, you must invent a new demand system.

For technology startups coming out of Nigeria, and Africa, the challenge of lack of product scalability, and poor mentorship may continue to pose serious limitations to their growth. These are aside others, including access to finances, connectivity, market size, and changing consumer needs.

As identified by Google chiefs, on Wednesday, at the ongoing Global Accelerator and Launchpad Programme, in San Francisco, United States, startups needed to change the way people consume products and services.

[…]

While stressing that Google currently focused on startups from emerging markets such as Nigeria, he noted that the next target for the firm was to reach the next billion people with technology.

[…]

To Luke Wroblewski, also a Product Manager, startups must measure the kind of design that works specifically for the task; focus on core features, grow critical engagement and ensure adequate ergonomics.

Wroblewski advised startups to stake a balance between quantity and quality to create a lasting solution.

For companies like Google, they understand that they would be unable to have next billion users if they continue focusing on already met (or known) needs. So, what Google has to do is to invent a new demand system where customers have new needs (think of googling over going to Library). And once those needs evolve, meet them as a category-king entity, enjoying the first to market (yes, the first mover advantage) benefits.

How do you change consumer needs? You create products which serve users at the levels of expectations or perceptions, with perceptions being better. In other words, you create products which stimulate new needs in the lifestyles of users. Things they never thought they needed, but when they see your products, they would quickly activate a latent (existing) need which that product would solve.

Steve Jobs, Apple Founder, was legendary for stimulating demand. He worked without surveys or focus groups. He was a genius, peerless in his generation. He saw an unborn future many years ago. He was an icon, who changed his world. He developed a good design paradigm of working at the perception of customers, beyond their needs and expectations. He found glory and Apple triumphed with iPod, iPhone, iPad and more.

I discuss why organizations must focus on developing products and services that go beyond the needs of customers to their expectations and perceptions. Focusing on the needs of customers is a recipe for disaster. The whole desire must be to deliver products and services at the level of customer perception where they are offered products and services which they might not have even imagined would be possible. But the day they see the products they will say wow: That is the thing I have been thinking. This also explains the limitations of focus groups because focus groups are tethered to what the customers think they need. Perception of customer level service is offering something which could not have been requested during focus groups, because such products will not come into the imaginations of the people being studied.

Simply, we have a challenge in Nigeria: we cannot be solely building products for needs which are already met by products in the markets. For us to have millions of users, we must make products in Nigeria that can stimulate new needs which do not currently exist, and then serve them efficiently.

Great Comments from LinkedIn

Comment 1: A tough one, in a country where lots of people are still struggling to meet the basic needs, without much success ofcourse. While they try to run away from their problems, it becomes more apparent that their intended destinations even have more problems.

In the middle this challenge, startups now have to make products at perception level. But there’s an impediment: how affordable would those products at perception level be? If they fail the affordability test, everything goes back to purchasing power conundrum; which oftentimes makes great products more or less appear useless.

It’s a big challenge, investing the energy, intellectual and financial resources, and after coming up with such a great product, only to be hit by that ultimate reality, which is: consumers LOVE your product, but CANNOT afford it. The Google guy talked about achieving the right mix between quality and quantity, and in our case; you still have to figure out those who can afford.

Perhaps it could be the reason why everyone is almost doing the same thing: from telecom to banking, and everything in between; because those who tried to be different have practically gone out of business. All the troubles in the land are closely related, startups facing same.

Comment 2

Two things.

1. Nigeria is a peculiar market. Very peculiar that when you intend to wow your customers sometimes, you wow no one – only dwindling sales. As mentioned by Francis Oguaju products borne out of the perception construct tend to be high-end and rarely affordable at scale.

Changing consumer behaviour/ needs is largely identified by data. At startup level, you either don’t have the scale or the data to draw insights on consumer behavioural patterns.

Therefore, generally speaking, my take is let startups even get the rudimentary very right. Let them even stay in business n turn in a profit first. Let the business environment be enabling and at ease first. Then they can start thinking of wowing their customers.

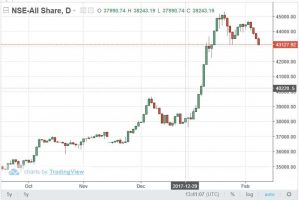

Many have contacted me for some perspectives after I posted something on the stock market. I had noted that loss of value may happen, and suggested that people may need to leave instructions with their brokers, to pull the triggers, if the mayhem should continue. I am not sure what would happen. And no one is ever sure. Just as in politics, I like the stock market because there are always hard outcomes: elections come with winners and losers, and stock prices rise and fall. So, any statement can be tested and benchmarked with real results, unlike say approval rating and popularity of leaders which provide no definite outcomes to validate them.

Now, are you on alert in case this sell-off continues? If you have equity anywhere, please do not be far from your broker. Have an outstanding instruction to pull the trigger if the mayhem continues. We may be in for market correction, but it is too early to talk that.

I explained to the people that checked that it would be premature to start making decisions because of few isolated bumps. The key is making sure that it is not yet a negative pattern that is sustained. At this point, nothing has happened to trigger that tsunami of fear which can move markets at unprecedented level within a very short time.

Yes, I explained that I had personally gotten out of stocks few days after President Trump passed his tax law in the United States. I was a banker; I continue to work with leading bank clients on strategies. As an entrepreneur, I practice what I teach.

Nigerian Stock Exchange Chart

One thing I know is that inflation is always fought vigorously by any government. If Trump Tax Law makes U.S. firms to bring money home, they would pay dividends to shareholders. Also, they would give out a lot of money to their workers. Possibly, they would invest here and there. Those are all great stuff. The economy would horn and people would have great Christmas, and Black Friday would become Spend Friday. The consumer confidence would be huge and general business sentiment would accelerate.

However, as government begins to fight inflation, many things would happen. The Federal Reserve of U.S. would hike interest rates. When it hikes rates to curtail inflation, the cost of capital would go high. Then, immediately, many companies would start watching their shoulders. So, borrowing would become a little more expensive and spending would become more managed. Stock market traditionally does not always perform well in that domain as bond market would become more attractive since high rates would favor it for investors. Besides, if rates are high, savers would have alternatives as they can make money by saving. Right now, there is no value in saving because rates are artificially low. But if rates go high, saving would improve. That means, saving becomes an option besides investing in stock markets.

In Nigeria, specifically, I do not expect a lot of contagion from foreign markets to affect us, since at the moment, most of the funds in the Nigerian Stock Exchange (NSE), are indigenous. So, anything that happens in countries like U.S. would have marginal impacts in our stock market. Sure, there would be impacts, but only minimal. It is unlike 2008 when foreign investors were heavily invested in the NSE, and when they pulled money to cover losses in their home countries, they triggered local dominos largely driven from the fall of Lehmann Brothers. This time, it may not be so since the roughly $40 billion market caps of the Nigerian Stock Exchange are mainly local capital.

Uber has settled the lawsuit which Google sibling, Waymo, brought against it on trade secrets related to Lidar, a key component in autonomous driving vehicles. This has long been expected: Waymo may have a better technology, but Uber has the best product. Uber is light years ahead of Waymo on transportation which is what all these technologies are designed to advance. So, Waymo cannot afford to damage Uber to the extent that it cannot find a path to become a future partner. Alphabet, Waymo (and Google) parent, is an investor in Uber.

“We have reached an agreement with Uber that we believe will protect Waymo’s intellectual property now and into the future.” Waymo statement

“To our friends at Alphabet: we are partners, you are an important investor in Uber, and we share a deep belief in the power of technology to change people’s lives for the better.” Uber CEO

Uber was expected to lead the way for Alphabet, and that was why Alphabet invested in Uber. See it this way: if Waymo invents this great technology, it would need a global transportation company to monetize it. Uber is well-ahead of other American companies in that space. Even though the lawsuit pushed Alphabet to invest in Lyft, most analysts believe that Lyft has no global future. With Didi already causing havoc around the globe, the only way Waymo can play a role is to see a strong Uber in the world. After all, Uber is partly owned by Alphabet!

According to TechCrunch, “The agreement also comes with a financial settlement of roughly $244 million in stock (that is 0.34 percent of Uber’s equity, valued at its Series G-1 round, which gave the company a $72 billion valuation)”. That is not close to the $1 billion Waymo has expected. It is also good the settlement is coming as stocks which ensures that Uber does not have to spend its cash on this.

I think everyone won by settling this case: Alphabet needs Uber to go after Didi which is now the hottest startup in the world. This lawsuit is a huge distraction to Uber. Now it is over, they would begin to plot how to handle their Chinese competitors who are also moving into making driverless cars with their own partners.