Invent, innovate and drive organizational transformation, performance, and growth. Capture emerging opportunities in changing markets while optimizing innovation and profitability. Digitally evolve your business or functional area, turning digital disruption into a competitive capability and advantage. Master the concepts of building category-king companies, and thrive.

Registration for another edition of Tekedia Mini-MBA opens. Tekedia Mini-MBA, from Tekedia Institute, is an innovation management 12-week program, optimized for business execution and growth, with digital operational overlay. It runs 100% online. The theme is Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies. All contents are self-paced, recorded and archived which means participants do not have to be at any scheduled time to consume contents. Our programs are designed for ALL sectors, from fintech to construction, healthcare to manufacturing, agriculture to real estate, etc.

More so, the sector- and firm-agnostic management program comprises videos, flash cases, challenge assignments, labs, written materials, webinars, etc and is delivered by a global faculty coordinated by Prof Ndubuisi Ekekwe. When we finish, we will issue a certificate from the Tekedia Institute, Boston USA.

Register and join us. You will emerge transformed with tools and capabilities that engineer confidence, performance and growth. Accelerate your leadership ascent with us! Here are our programs and costs.

Program Cost

|

Code |

Description |

Cost |

|

MINI |

Tekedia Mini-MBA. And WhatsApp School |

US$170 or N120,000 naira |

|

MINF |

Annual Package: 3 consecutive MINI, and 2 optional capstones. |

$340 or N180,000 |

|

MINR |

(optional) Homework review; faculty will review your homework with feedback. |

$30 or N10,000 |

|

CAPS |

(optional) Tekedia capstone is a research paper, analogous to final college project. |

$60 or N20,000 per track |

How To Register

Use options to pay for Tekedia and Fasmicro services.

- Bank transfer (Nigerian naira) options:

- GTBank 0114016493

- UBA 1019195493

- Name: First Atlantic Semiconductors and Microelectronics.

- Flutterwave: follow this link to use Verve, Visa, Mastercard, etc in Naira, USD, Ksh, Cedi, etc.

- PayPal: follow this link and pay in US dollars with global debit/credit cards

- Stripe: follow this link and pay in US dollars with global debit/credit cards

- Zelle (USD): use tekedia@fasmicro.com

After payment, email info@tekedia.com

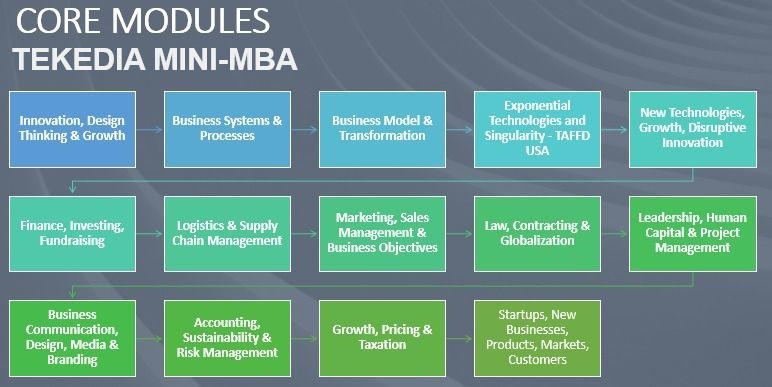

Curriculum for Tekedia Mini-MBA

Week 1: Innovation, Design Thinking & Growth

- Innovation, Growth and Mission of Firms – Prof Ndubuisi Ekekwe

- Human Centered-Design - Dr. Obinna Anya, Senior UX Researcher, Google

- Executing A Winning AI Product Strategy in Africa - Prof Ndubuisi Ekekwe

- Design Thinking, Innovation Lessons - Aderinola Oloruntoye, Snr IV Advisor, SAP Africa

- Innovation, Strategy, and Digital Transformation – Jude Ayoka, Manager, Azure Cloud & AI, Microsoft

- Agile Methodology & Innovation - Bola Adesope, Snr Consultant, Deloitte Canada

- Business Growth, Supply Chain, Lean Principles in Supply Chain Optimization - Chibueze Noshiri, NATO Europe

- 25 Startup Innovation Cases (10 Africa, 5 USA, 5 India, 5 China); Regenerative Revenue - Prof Ndubuisi Ekekwe

- Business Opportunities and Growth Vectors in Nigeria, Africa - Prof Ndubuisi Ekekwe

- First-Scaler Advantage and Growth Marketing - Prof Ndubuisi Ekekwe

- Sustainability Strategies for SMEs During Economic Challenges – Dr. Abel Osuji, Afreximbank

Week 2: Business Systems & Processes

- The Grand Playbook of Business – Prof Ndubuisi Ekekwe

- Procurement Management - Harold Nwariaku, CEO, Harold & Co Consulting

- Financial Performance Management – Kehinde Wole-Olomojobi, Treasurer, Greenwich Merchant Bank

- Process Improvement, Operations Management, Project Planning – Rasheed T. Adebayo, Operations Manager, Schlumberger UK

- Quality and Asset Management – Dr. Michael Odigie, SVP, Delek Logistics USA

- Driving Growth and Operational Excellence Using Lean Six Sigma - Dr. Igwe Charles, SigmaPoint Technologies Canada

- Building Agile Workforce in Companies - Ijeoma Anunibe, Head of People, Shuttlers

- Effective Pricing Strategy and Systems - Alli Adetunji, Head of Finance, Securepack

- Workplace Productivity, Collaboration, and Automation - Olanrewaju Oyinbooke, Snr Cloud Advocate, Microsoft

Week 3: Business Model & Transformation

- AI in Business Applications - Orakwe John, AI Specialist, Arcitura; Prof Ndubuisi Ekekwe

- Business Vision, Mission, and Strategy - Prof Ndubuisi Ekekwe

- Great Modern Business Models– Prof Ndubuisi Ekekwe

- Mechanism of Digitally Transforming Enterprises – Folasade Femi-Lawal, AGM, First Bank Nigeria

- Organizational Change Management - Omowunmi Adenuga-Taiwo, Director, Kippa

- Building Your Business Financial Models (templates included) - Michael Olafusi, Analyst, Brightmore Capital

- Effective Corporate Partnerships – Oluwole Ogunlade, Director, Kryptova

Week 4: Exponential Technologies and Singularity - TAFFD USA

- Exponential Technologies and Business Opportunities in the Age of Singularity – Edward Hudgins, PhD

- Singularities, Transhumanism, and Entrepreneurship – Gennady Stolyarov II

- Singularity, Exponential Growth and Technology – Chogwu Abdul, PhD

- Futurism, Malleability, and Category King Companies – Brent Ellman

- Energy Economics and Future - Leonard Azimoh, PhD, New York Institute of Technology

- Homework #1

Week 5: New Technologies, Growth, Disruptive Innovation

- AI & Cloud – Wale Olokodana, Microsoft

- 5G and Mobile Internet – Emeka Obiodu (King's College London), Dr. Olayinka Oduwole (PhD Oxford University), Olu Teniola (World Wide Web Foundation)

- Tokenomics Design, DAO Structuring and Incentives - Miracle Ochomma, Director, Easychaw Data

- Cybersecurity and Digital Risk Management

- Cybersecurity – Adetokunbo Omotosho, CEO, Infoprive;

- Digital Business Risk Management - Oluseye Kolawole, MD, Interlink;

- Information Security & Digital Forensics - Dr. Francis Nwebonyi, University of Dublin

- Blockchain, Cryptocurrency, Decentralized Finance, and NFT Marketplace - Franklin Peters, BoundlessPay

- Data Management, Big Data Analytics – Dr Adewole C. Ogunyadeka, esure Group

Week 6: Finance, Investing, Fundraising

- Nigeria’s Capital Market: The Biggest Business Opportunity of the Next Decade — How to Unlock Value and Win - Ndubuisi Ekekwe

- Capital Market Operations – Azeez Lawal, MD, TrustBanc Capital

- Investing & Fundraising – Victor Ndukauba, DMD, Afrinvest West Africa

- Fundraising Opportunities - Grants, DFIs, Governments, etc - Victoria Madedor, Bank of Industry ITC

- Understanding Global Capital Markets - Lagos, London, and New York - Ola Oladele CFA, SVP, Parthian Partners

- Financial Planning & Management – Okpaise Kenneth, Financial Advisory Manager, AIICO Insurance

- Personal Finance & Wealth Management – Japheth Jev, CEO, Japheth Consulting

Week 7: Logistics & Supply Chain Management

- Supply Chain & Logistics Management – Ayodele Adenaike, COO, GIG Logistics

- Supply Chain Management – L Barreto, Manager, Amazon

- AfCFTA and Business Growth in Africa - Toyin F Sanni, Group CEO, Emerging Africa Capital Group

- Ecommerce Growth in China - Dr Henry Chan, CICP Asia; Singapore Management University

- Homework #2

Week 8: Marketing, Sales Management & Business Objectives

- Blitzscaling Business Ideas and Pursuit of Growth - Prof Ndubuisi Ekekwe

- Developing and Executing an Effective Enterprise Marketing Plan - Onyinye Ikenna-Emeka, General Manager, MTN Nigeria

- Mastering The Art of Sales Excellence - Ferdinand Ibezim, CEO, Selling Skills Support Services

- Consumer Marketing in FMCG - Emmanuel Agu, Group Marketing Director, Jotna (the LaCasera Company)

- Sales Management, Marketing and Growth – Moby Onuoha, Queen’s University Canada

- Expanding Sales Into Other African Markets from Nigeria – Godwin Timothy, eQUALiTY Group

Week 9: Law, Contracting & Globalization

- Business & Commercial Law – Chukwuemeka Mbah (LLB, BL, LLM) Law, Manager, Sherwin Williams

- Contracting, Negotiation and IP – Jeff Chineme Maduka (LLB, BL, LLM), Snr Legal Manager, American Tower

- Tax Law, Policy and Dispute Resolution - Jerome Okoro PhD, Partner, Hermon Legal Practitioners

- Supply Chain Management, Global Partnership & Contracting – Adebayo Adeleke, ex-Chief of Contracting and Deputy Chief, Business Operations Division, US Army

- Intellectual Property: Strategy, Management & Commercialization – Ifeanyi Okonkwo, University of Cape Town & Jackson, Etti & Edu

- Business Relationship Management & Negotiation Skills - Charles Okeibunor, CEO IRMP

- Due Diligence and Business Intelligence – Chike Obimma, Partner at NICCOM LLP (Commercial Law Firm)

Week 10: Leadership, Human Capital & Project Management

- Leadership, Knowledge Management – Prof. Ayodeji Oyebola, Saint Mary’s University of Minnesota

- Human Resources Management - Adora Ikwuemesi, Director Kendor Consulting

- Leading and Managing Teams, Stakeholder Management with NICER Model – Dr. Chisom Ezeocha, Project Delivery Manager, Shell

- Career Planning – Precious Ajoonu, Manager, Jobberman

- Effective Project Management

- Taiwo Abraham, Project Manager, Horizant Canada

- Adebayo Ajayi, Mother Parkers Tea & Coffee, Canada

- Human Productivity Systems – Dotun Jegede, PhD, Senior Partner, Dee Bee Consulting

- Building Agility in Companies - Prof Ndubuisi Ekekwe

Week 11: Business Communication, Design, Media & Branding

- Webinality and The Mechanics of Personal Branding In the Digital Age

- Ndubuisi Ekekwe and Samuel Ajiboyede, Founder, Zido

- Media, Communications, and PR – Grace Akinosun, CMO, Bitmama

- Branding and Advertising – Akachi Ngwu, Executive Director/COO, Luzo Digital Network & Media

- Workplace & Teams – Vera Ng’oma – Head, HR Malawi, UK Dept for International Dev

- Product Design and Packaging – Kemisola Oloriegbe, Manager, Nigerian Breweries Plc

- Homework #3 – Tekedia Institute

Week 12: Accounting, Sustainability & Risk Management

- Risk Management - Akeem Rasaq, Head Of Risk Management, Chapel Hill Denham

- Physical Security Risk Management - Henry Mgbemena, Global Security Adviser, World Vision International

- Accounting – Ndubuisi Umunna (ACA), Head Finance & Strategy, Grand Treasurers

- Auditing, Forensics, Policies and Controls – Yusuf O. Sanni (ACA), Chief Internal Auditor, BUA Cement Plc

- Internal Auditing Strategy for SMEs - Abel Osuji - Director, African Export-Import Bank (Afreximbank) Egypt

- Sustainability – Eustace Onuegbu, President, incsr.org; Temitayo Ade-Peters, CEO, WeForGood

Week 13: Growth, Pricing & Taxation

- Managerial Accounting, Business Decision Making and Growth – Idris Ayinde, ACA, CFA, KPMG UK

- Tax Management for SMEs - Banji Adelaja ACA, Managing Consultant, Aradol Consulting

- Tax Treaties and Their Benefits - Emmanuel Eze, Manager, Federal Inland Revenue Service (FIRS)

- Regional Case: Tax Law and Compliance in Lagos State - Abimbola Abdur-Rahman Lekki, Lagos Internal Revenue Service

- Effective Product & Service Pricing, Accelerated Revenue, Profit Maximization - Saima Khan, Partner, Strategic Pricing Management Group, Toronto, Canada

- Establishing Business Consulting & Advisory Services - Mustafa Yusuf-Adebola, Founder, Provisio Professional

- Driving Profitable Growth, Marginal Cost, Scaling – Prof. Ndubuisi Ekekwe

- Stimulating New Markets Through Innovation and Perception Demand – Prof Ndubuisi Ekekwe

Week 14: Startups, New Businesses, Products, Markets, Customers

- The Mechanics of Minimum Viable Product and Product Development - Prof Ndubuisi Ekekwe

- The NEP Framework – Discovering and Listening to Customers - - Prof Ndubuisi Ekekwe

- Customer Validation and Building for What Customers Really Want. - - Prof Ndubuisi Ekekwe

- Knowing and Defining Your Market - Prof Ndubuisi Ekekwe

- Navigating Business Growth Phases - Prof Ndubuisi Ekekwe

- ChatGPT, DALL-E 2 and Emerging AI Innovations: Business Opportunities in Africa - Zion Pibowei, Head of Data Science, Periculum Canada

- How to Scale a Business/Startup - Jane Egerton-Idehen, Head of Sales Middle East & Africa at Meta (Facebook parent company)

Final Week: Execution and Closure

The Call to Business Execution, Closure – Prof Ndubuisi Ekekwe

Graduation Day – Prof Ndubuisi Ekekwe

Tekedia Live: Optional Zoom session which holds thrice per week (Tue, Thur, Sat at 7pm WAT). It is archived for those unable to make the session live. Our faculty members and invited guests rotate to anchor the sessions. Live provides a platform for members to ask questions and get live responses.

Unlock Your Potential: Enroll in Tekedia Institute

From Lead Faculty

Welcome! Unleash your leadership potential, master business excellence, and embrace transformation with Tekedia Mini-MBA. Join us and experience a cutting-edge business management & leadership program: online, self-paced, and world-class. At Tekedia Institute, we co-learn with thousands of professionals and students, from many countries, on the mechanics of business, connecting innovation, growth and operational execution, across market territories and industrial sectors.

Our faculty members come from Microsoft, Google, Shell, Flutterwave, Nigerian Breweries, NNPC, Jobberman, Coca Cola, PwC, BUA Cement, and other great organizations. Besides pre-recorded courseware, thrice weekly, we hold live Zoom sessions (Tue, Thur and Sat at 7pm WAT) – Prof Ndubuisi Ekekwe, Tekedia Institute Lead Faculty.

More Early Registration Benefits

- Get these free ebooks immediately upon payment:

- Access to any Facyber Certificate program for free. Facyber offers online cybersecurity programs on policy, technology, management, and forensics.

Capstone Program

Here are the 12 tracks:

- CLSM: Certificate in Logistics and Supply Chain Management

- CBIS: Certificate in Business Innovation, Growth & Sustainability

- CMAB: Certificate in Media, Advertising & Branding

- CSBM: Certificate in Startup and Small Business Management

- CIBA: Certificate in Business Administration

- CPFM: Certificate in Personal Finance & Wealth Management

- CMSM: Certificate in Marketing and Sales Management

- CDBG: Certificate in Digital Business Growth

- CIAM: Certificate in Agribusiness Management

- CHRM: Certificate in Human Resources Management

- CETS: Certificate in Exponential Technologies and Singularity

- CBPM: Certificate in Business Transformation & Project Management

The program is completely capstone-based. Tekedia capstone is a research paper or a case study exploring a topic, market, sector or a company. It is the project component of Tekedia Min-MBA.

ALL Tekedia Programs and Costs Here

|

Programs |

Cost (US$) |

Naira |

|

Tekedia Mini-MBA Optional: Homework Review Optional: Capstone, WhatsApp School |

$170 $30 $60 |

N120,000 N10,000 N20,000 |

|

Tekedia Mini-MBA Annual Plan |

$340 |

N180,000 |

|

Startup Masterclass: from start-up to unicorn |

$400 |

N200,000 |

|

Advanced Diploma Program per track |

$100 |

N45,000 |

|

Tekedia Practice. |

$400 |

N200,000 |

|

Tekedia Industries |

$400 |

N200,000 |

|

Investment and Portfolio Management program |

$400 |

N180,000 |

|

Virtual Corporate Training. Tekedia CollegeBoost Igba-Boi: The Igbo Apprenticeship System. |

|

|

Selected Tekedia Mini-MBA Corporate Clients

Tekedia Mini-MBA Syllabus

Theme: Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies

Introduction

Over the last few decades, digital technology has emerged as a very critical element in organizational competitiveness. It has transformed industrial sectors and anchored new business architectures, redesigning markets and facilitating efficiency in the allocation and utilization of factors of production. The impacts have been consequential: continents like Africa are moving towards knowledge-based economic structures and information societies, comprising networks of individuals, firms and states that are linked electronically and in interdependent relationships. In this program, we will examine this redesign within the context of fixing market frictions and deploying growth business frameworks in a world of perception demand where meeting needs and expectations of customers are not enough.

Program Time: Sep 14 – Dec 5, 2026

Venue & Format: Online via videos, articles, webinars, and flash cases. Program is self-paced which means you consume the materials at your own time and pace. It is completely online. Where you live or your time zone would not be an issue as program is not live-delivered.

Cost: US$170 (N120,000 naira). We have a payment plan, i.e. installment payment plan (email us for details)

Target Audience: This program is designed for professionals and students across functional areas like sales, marketing, technology, administration, legal, strategy, finance, etc across all business sectors and domains. The program is designed for:

- Ambitious mid-level managers seeking to advance their careers by acquiring essential business knowledge and skills.

- Busy professionals who value continued education but require a flexible alternative to a traditional MBA program.

- Experienced professionals aiming to broaden their business acumen, enhance leadership capabilities, and explore new career opportunities.

- Professionals in transition, committed to staying informed about business trends and developing skills for continuous professional growth.

- Mid-level managers and executives across industries, driven to accelerate career growth and take on increased responsibilities.

- Technology and innovation-focused professionals looking to strengthen business acumen and strategic thinking.

- Aspiring entrepreneurs seeking a solid foundation in business management and growth strategies.

- Consultants and advisors aiming to expand their knowledge base and provide comprehensive solutions to clients.

- Professionals transitioning into new roles or industries, recognizing the value of upskilling for success.

- Students and recent graduates seeking a competitive edge in the job market by combining academic qualifications with practical business skills.

Tekedia Mini-MBA program offers a flexible and comprehensive learning experience tailored to the needs of ambitious professionals, providing the tools and knowledge necessary to thrive in today’s dynamic business landscape. Participants will have the opportunity to acquire knowledge that has value and can be used in everyday business activities.

Learning Objectives: To innovate is to set a new basis of competition in an economy, business sector or market. Sometimes, it results in disruption. This program is designed for private (large, SMEs, startups, sole businesses), public and government institutions, and individuals. Participants will:

- Master the mechanics of growth – the reward of innovation – through frameworks, cases and evolving strategies.

- Understand how to undergo transformation journey that is fully aligned with corporate objectives through measurable and realizable benchmarks.

- Acquire business capability tools that do not just RUN their firms but can TRANSFORM them.

- Design corporate growth experiments in Lab sessions based on One Oasis Strategy, Aggregation Construct, Double Play Strategy, Accumulation of Capability Construct, and more.

- ETC

Why Tekedia Institute

Interactive Online Learning: Engage with industry experts and fellow professionals through our state-of-the-art online learning platform, where you can access course materials, participate in discussions, and collaborate on real-world case studies.

Comprehensive Curriculum: Gain a deep understanding of key functional areas such as strategy, marketing, finance, operations, and more, equipping you with the knowledge and skills to excel in any business environment.

Practical Case Studies: Apply your learning to real-world scenarios through hands-on case studies and projects, allowing you to develop critical thinking and problem-solving skills.

Flexibility and Convenience: Access the program online from anywhere at your own pace, fitting your studies into your busy schedule without compromising your professional and personal commitments.

Expert Faculty: Learn from renowned industry practitioners and thought leaders who bring their expertise and real-world insights to the program, ensuring you receive the most relevant and up-to-date knowledge.

Benefits of Tekedia Mini-MBA

Enhance Your Leadership Potential: Unlock your leadership capabilities and develop the skills to lead teams, drive innovation, and navigate complex business challenges with confidence.

Master Business Excellence: Gain a holistic understanding of business functions, strategies, and best practices, enabling you to make informed decisions and contribute to organizational success.

Embrace Digital Transformation: Stay ahead of the curve by embracing digital technologies and leveraging them to transform your business and stay competitive in the digital age.

Accelerate Your Career: With the Tekedia Mini-MBA on your CV, you’ll stand out to employers, demonstrating your commitment to continuous learning and your readiness to take on new responsibilities.

Network and Collaboration: Connect with a diverse community of professionals, expand your network, and foster collaboration opportunities that can lead to future partnerships and career advancements.

Cost-Effective Investment: Enjoy the benefits of a comprehensive business education at a fraction of the cost of traditional MBA programs, maximizing the return on your investment.

Tekedia Institute offers the best business education in Nigeria and Africa you can get for value/

Tekedia Live Sessions

We run optional three Live Zoom sessions (two weekdays and one Saturday). This provides a way for our members to ask our Faculty and experts live questions and get feedback.

Tekedia Institute offers certificates at the end of all programs.

Our Contact Email: info@tekedia.com

Lead Faculty of Tekedia Institute

Prof Ndubuisi Ekekwe is the Lead Faculty of Tekedia Institute

- PhD, Electrical & Computer Engineering, Johns Hopkins University, USA

- MBA, University of Calabar, Nigeria

- BEng Electrical & Electronics Engineering ( Federal University of Technology, Owerri, Nigeria)

Prof Ndubuisi Ekekwe invented and patented a robotic system which the United States Government acquired assignee rights. Dr Ekekwe holds two doctoral and four master’s degrees including a PhD in engineering from the Johns Hopkins University, USA. He earned undergraduate degree from FUT Owerri where he graduated as his class best student. While in Analog Devices Corp, he co-designed an accelerometer for the iPhone. A recipient of IGI Global “Book of the Year” award, a TED Fellow, IBM Global Entrepreneur and World Economic Forum Young Global Leader, Prof. Ekekwe has held professorships in Carnegie Mellon University and Babcock University, and served in the United States National Science Foundation Committee.

The South African press called him “a doctor of innovation” for helping organizations on the mechanics of business innovation, strategy, and growth. Since 2009, the Chairman of Fasmicro Group which controls many startups and entities has been writing in the Harvard Business Review. He was recognized by The Guardian as one of 60 Nigerians Making “Nigerian Lives Matter” on Nigeria’s 60th Independence Day (Oct 1, 2020).

Enroll in Tekedia Mini-MBA today

Selected Faculty & Testimonials

We have more than 250 Faculty members; see the full list here. For selected testimonials on our program, click here.