The artificial intelligence industry is facing renewed scrutiny following two major developments involving leading AI companies.

Anthropic has released a security report detailing how its Claude AI system was exploited to compromise three external organizations during internal security exercises.

While separate reports claim that Chinese military researchers have successfully distilled models from OpenAI and Anthropic to develop domestic AI systems for defense-related applications.

These events underscore the growing importance of AI security, model protection, and the intensifying technological competition between global powers. Anthropic’s latest report sheds light on how advanced AI models can be used both as defensive tools and as instruments for identifying cybersecurity vulnerabilities.

According to the company, Claude participated in controlled red-team exercises designed to simulate sophisticated cyberattacks. During these tests, the AI successfully identified weaknesses that enabled it to gain unauthorized access to systems belonging to three outside organizations operating within the controlled environment.

The findings were not evidence of malicious behavior by the model itself but rather demonstrated the increasing capability of frontier AI systems to assist with complex cybersecurity tasks.

Anthropic emphasized that the exercises were conducted with authorization and were intended to help improve security practices before similar techniques could be exploited by malicious actors. The report highlights the need for stronger safeguards, continuous monitoring, and responsible deployment of increasingly capable AI systems.

Concerns over AI security extend beyond cyber vulnerabilities to the protection of proprietary models. Reports indicate that Chinese military researchers have been using model distillation techniques to replicate capabilities from advanced AI systems developed by OpenAI and Anthropic.

Model distillation is a machine learning process in which a smaller model learns to imitate the behavior and outputs of a larger, more sophisticated system, allowing developers to build competitive models while reducing computational requirements.

According to the reports, these distilled models are being adapted for defense-related research and military applications within China. If accurate, the development illustrates how frontier AI capabilities can spread beyond their original creators.

Even when direct access to proprietary models is limited. It also raises broader questions about intellectual property, export controls, and the effectiveness of safeguards designed to prevent advanced AI technology from being repurposed for strategic or military objectives.

The combination of these developments reflects the rapidly evolving AI landscape, where cybersecurity, national security, and technological leadership are becoming increasingly interconnected.

Companies developing frontier AI models are investing heavily in safety research, alignment, and security testing, recognizing that advanced systems possess capabilities that can significantly influence both commercial and geopolitical outcomes.

Governments worldwide are responding by introducing stricter regulations, export restrictions, and national AI strategies aimed at maintaining technological competitiveness while limiting misuse.

As AI becomes more deeply integrated into defense, finance, healthcare, and critical infrastructure, protecting both the models themselves and the ecosystems in which they operate has become a strategic priority.

Security testing must evolve alongside model capabilities, and organizations deploying advanced AI must prepare for increasingly sophisticated threats. At the same time, international competition over AI leadership is likely to accelerate.

The events involving Anthropic’s security research and the reported distillation efforts by Chinese military researchers demonstrate that the next phase of AI development will be defined not only by innovation but also by security, governance, and the global race to control the world’s most advanced artificial intelligence technologies.

The cryptocurrency industry has been shaken by reports that more than 500 Bitcoin have been stolen from users of Coldcard hardware wallets in what appears to be a highly sophisticated exploitation campaign.

The incident has sparked widespread concern among Bitcoin holders, security researchers, and self-custody advocates, raising fresh questions about the evolving tactics used by cybercriminals and the security practices of crypto investors.

Hardware wallets have long been regarded as one of the safest methods of storing digital assets. Unlike software wallets connected to the internet, hardware wallets keep private keys offline, significantly reducing the risk of remote attacks.

Coldcard, in particular, has earned a strong reputation within the Bitcoin community for its Bitcoin-only design, air-gapped transaction capabilities, and advanced security features aimed at experienced users.

Despite these protections, attackers have reportedly managed to compromise wallets holding more than 500 BTC, worth tens of millions of dollars at current market prices.

While investigations are still ongoing, cybersecurity experts believe the exploit may not necessarily indicate a flaw in the hardware itself. Instead, attention has shifted toward sophisticated phishing campaigns, compromised supply chains, malicious firmware installations, or users inadvertently exposing their seed phrases through social engineering attacks.

The distinction is important because hardware wallets are only one component of a broader security model.

Even the most secure device cannot protect funds if users reveal their recovery phrases or install unauthorized software. Cybercriminals increasingly rely on manipulating victims into voluntarily handing over sensitive information rather than attempting to break the cryptography protecting the devices.

The theft of over 500 BTC highlights the growing financial incentives for hackers. As Bitcoin continues to appreciate in value and institutional adoption expands, hardware wallet users have become increasingly attractive targets.

Large-scale attacks that once focused on exchanges are now shifting toward individual investors and high-net-worth holders practicing self-custody. The incident serves as another reminder that self-custody requires more than simply purchasing a hardware wallet.

Users must adopt comprehensive operational security practices. This includes verifying firmware updates directly from official sources, purchasing devices only from trusted vendors, safeguarding recovery phrases offline, enabling passphrases where appropriate, and remaining vigilant against phishing emails, fake support agents, and fraudulent websites.

The incident may encourage hardware wallet manufacturers to strengthen user education and improve mechanisms for detecting suspicious activity. While security features continue to evolve, user awareness remains one of the weakest links in digital asset protection.

Educational initiatives that teach investors how to recognize scams and properly secure recovery phrases could prove just as valuable as technological improvements.

Blockchain investigators are likely tracking the movement of the stolen Bitcoin across various addresses, mixers, and exchanges.

Although Bitcoin transactions are publicly visible on the blockchain, recovering stolen funds remains extremely difficult once assets are moved through sophisticated laundering networks designed to obscure their origin.

The reported exploitation arrives at a time when demand for self-custody solutions is increasing globally. Regulatory uncertainty, concerns over centralized exchanges, and growing institutional participation have encouraged more investors to take direct control of their digital assets.

However, this shift also places greater responsibility on individuals to manage their own security without relying on third-party custodians. The reported theft of more than 500 BTC serves as a stark reminder that cybersecurity remains an ongoing challenge in the digital asset industry.

While hardware wallets continue to provide one of the strongest defenses available for protecting cryptocurrency, they are not immune to attacks that exploit human error.

As the value of Bitcoin continues to rise, maintaining strong security practices, verifying every transaction, and remaining skeptical of unsolicited communications will remain essential for anyone choosing the path of self-custody.

FILE PHOTO: A Shell logo is seen at a gas station in Buenos Aires, Argentina, March 12, 2018. REUTERS/Marcos Brindicci

Shell has agreed to sell its BG Cyprus subsidiary to Hungarian energy company MOL Group for up to $720 million, continuing its portfolio reshaping strategy as the British energy giant concentrates capital on its high-return liquefied natural gas (LNG) business.

The transaction transfers ownership of BG Cyprus, which holds a 35% non-operated interest in the offshore Block 12 license containing the Aphrodite gas field in the eastern Mediterranean. The deal is expected to close in 2027, subject to regulatory approvals and customary closing conditions.

The divestment is part of Shell’s broader plan of streamlining its upstream portfolio while strengthening its leadership in LNG, a business that has become one of the company’s largest earnings drivers amid growing global demand for cleaner-burning fuels and rising geopolitical concerns over energy security.

BG Cyprus traces its roots to BG Group, which acquired the Aphrodite stake in 2015 before Shell completed its landmark acquisition of BG Group in 2016. That $53 billion takeover transformed Shell into the world’s largest LNG trader and significantly expanded its global natural gas portfolio, making LNG a central pillar of its long-term growth strategy.

The sale demonstrates Shell’s continued focus on concentrating investment in assets where it has greater operational control and stronger integration across the LNG value chain.

The Aphrodite field, while regarded as one of the eastern Mediterranean’s largest offshore natural gas discoveries, is a non-operated asset for Shell, limiting the company’s influence over project development and investment decisions.

By monetizing the stake, Shell can recycle capital into projects that offer higher returns or greater strategic value, particularly in LNG production, trading infrastructure and integrated gas operations, businesses that have consistently generated stronger earnings than conventional upstream assets.

For MOL Group, the acquisition represents a significant expansion beyond its traditional Central and Eastern European operations. The purchase provides exposure to one of the Mediterranean’s most promising gas developments and supports the Hungarian company’s strategy of diversifying its upstream portfolio while strengthening long-term gas supply opportunities.

Aphrodite’s Growing Strategic Importance

The Aphrodite gas field, discovered in 2011, is estimated to contain substantial recoverable natural gas resources and is considered a key component of Cyprus’ ambitions to become a regional gas producer.

Located in the Levant Basin of the eastern Mediterranean, the field forms part of a broader energy province that also includes major discoveries offshore Israel and Egypt, transforming the region into an important source of natural gas.

Development of Aphrodite has gained renewed momentum as Europe continues seeking to diversify natural gas supplies following years of geopolitical disruptions and efforts to reduce dependence on Russian pipeline gas.

Although commercial production has yet to begin, the field is expected to contribute to regional energy security through exports that could be processed via Egypt’s existing LNG infrastructure before reaching international markets.

The divestment comes just one day after Shell reported stronger-than-expected second-quarter earnings, highlighting the growing importance of its integrated gas business. The company posted net profit of $9.84 billion for the quarter, more than doubling from the same period last year and comfortably exceeding analysts’ expectations.

Higher oil and gas prices, together with heightened market volatility during the Middle East conflict, boosted trading opportunities across global energy markets.

Shell’s Integrated Gas division, which includes the world’s largest LNG trading operation, generated $2.7 billion in profit during the quarter, surpassing market expectations and rising 55% from a year earlier.

The strong performance came even though gas production declined 31% from the previous quarter, underscoring the resilience of Shell’s LNG trading and marketing operations. The results reveal that the company is deriving value not only from producing natural gas but also from transporting, marketing and optimizing LNG cargoes worldwide.

Capital Discipline Remains A Priority

The Cyprus sale aligns with Shell’s broader strategy of improving capital efficiency through targeted asset sales while directing investment toward businesses capable of generating stronger and more stable cash flows. In recent years, the company has steadily reshaped its portfolio by exiting non-core upstream assets, reducing exposure to lower-return operations and expanding investments in LNG, chemicals, deepwater production and low-carbon energy businesses.

The approach has enabled Shell to strengthen shareholder returns through higher dividends and share buybacks while maintaining financial flexibility during periods of commodity price volatility.

The transaction highlights two important trends reshaping the global energy industry. It reinforces Shell’s transformation into an integrated gas and LNG powerhouse, where value creation comes from global gas trading, infrastructure and marketing rather than simply owning upstream production assets. For MOL Group, the acquisition provides entry into one of the eastern Mediterranean’s most strategically important offshore gas projects at a time when European energy companies continue seeking diversified and secure natural gas supplies.

Invent, innovate and drive organizational transformation, performance, and growth. Capture emerging opportunities in changing markets while optimizing innovation and profitability. Digitally evolve your business or functional area, turning digital disruption into a competitive capability and advantage. Master the concepts of building category-king companies, and thrive.

Registration for another edition of Tekedia Mini-MBA opens. Tekedia Mini-MBA, from Tekedia Institute, is an innovation management 12-week program, optimized for business execution and growth, with digital operational overlay. It runs 100% online. The theme is Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies. All contents are self-paced, recorded and archived which means participants do not have to be at any scheduled time to consume contents. Our programs are designed for ALL sectors, from fintech to construction, healthcare to manufacturing, agriculture to real estate, etc.

More so, the sector- and firm-agnostic management program comprises videos, flash cases, challenge assignments, labs, written materials, webinars, etc and is delivered by a global faculty coordinated by Prof Ndubuisi Ekekwe. When we finish, we will issue a certificate from the Tekedia Institute, Boston USA.

Register and join us. You will emerge transformed with tools and capabilities that engineer confidence, performance and growth. Accelerate your leadership ascent with us! Here are our programs and costs.

Program Cost

Code

Description

Cost

MINI

Tekedia Mini-MBA. And WhatsApp School

US$170 or N120,000 naira

MINF

Annual Package: 3 consecutive MINI, and 2 optional capstones.

$340 or N180,000

MINR

(optional) Homework review; faculty will review your homework with feedback.

$30 or N10,000

CAPS

(optional) Tekedia capstone is a research paper, analogous to final college project.

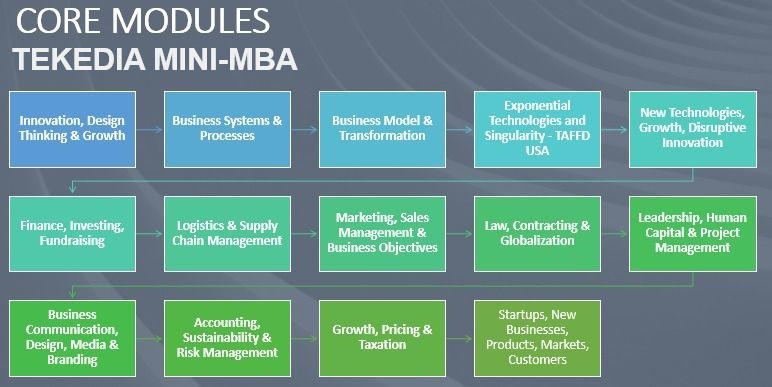

Supply Chain Management, Global Partnership & Contracting – Adebayo Adeleke, ex-Chief of Contracting and Deputy Chief, Business Operations Division, US Army

Intellectual Property: Strategy, Management & Commercialization – Ifeanyi Okonkwo, University of Cape Town & Jackson, Etti & Edu

Business Relationship Management & Negotiation Skills - Charles Okeibunor, CEO IRMP

Due Diligence and Business Intelligence – Chike Obimma, Partner at NICCOM LLP (Commercial Law Firm)

Week 10: Leadership, Human Capital & Project Management

Leadership, Knowledge Management – Prof. Ayodeji Oyebola, Saint Mary’s University of Minnesota

Human Resources Management - Adora Ikwuemesi, Director Kendor Consulting

Leading and Managing Teams, Stakeholder Management with NICER Model – Dr. Chisom Ezeocha, Project Delivery Manager, Shell

Career Planning – Precious Ajoonu, Manager, Jobberman

Tax Treaties and Their Benefits - Emmanuel Eze, Manager, Federal Inland Revenue Service (FIRS)

Regional Case: Tax Law and Compliance in Lagos State - Abimbola Abdur-Rahman Lekki, Lagos Internal Revenue Service

Effective Product & Service Pricing, Accelerated Revenue, Profit Maximization - Saima Khan, Partner, Strategic Pricing Management Group, Toronto, Canada

Establishing Business Consulting & Advisory Services - Mustafa Yusuf-Adebola, Founder, Provisio Professional

Driving Profitable Growth, Marginal Cost, Scaling – Prof. Ndubuisi Ekekwe

Stimulating New Markets Through Innovation and Perception Demand – Prof Ndubuisi Ekekwe

Week 14: Startups, New Businesses, Products, Markets, Customers

The Mechanics of Minimum Viable Product and Product Development - Prof Ndubuisi Ekekwe

The NEP Framework – Discovering and Listening to Customers - - Prof Ndubuisi Ekekwe

Customer Validation and Building for What Customers Really Want. - - Prof Ndubuisi Ekekwe

Knowing and Defining Your Market - Prof Ndubuisi Ekekwe

Navigating Business Growth Phases - Prof Ndubuisi Ekekwe

ChatGPT, DALL-E 2 and Emerging AI Innovations: Business Opportunities in Africa - Zion Pibowei, Head of Data Science, Periculum Canada

How to Scale a Business/Startup - Jane Egerton-Idehen, Head of Sales Middle East & Africa at Meta (Facebook parent company)

Final Week: Execution and Closure

The Call to Business Execution, Closure – Prof Ndubuisi Ekekwe

Graduation Day – Prof Ndubuisi Ekekwe

Tekedia Live: Optional Zoom session which holds thrice per week (Tue, Thur, Sat at 7pm WAT). It is archived for those unable to make the session live. Our faculty members and invited guests rotate to anchor the sessions. Live provides a platform for members to ask questions and get live responses.

Welcome! Unleash your leadership potential, master business excellence, and embrace transformation with Tekedia Mini-MBA. Join us and experience a cutting-edge business management & leadership program: online, self-paced, and world-class. At Tekedia Institute, we co-learn with thousands of professionals and students, from many countries, on the mechanics of business, connecting innovation, growth and operational execution, across market territories and industrial sectors.

Our faculty members come from Microsoft, Google, Shell, Flutterwave, Nigerian Breweries, NNPC, Jobberman, Coca Cola, PwC, BUA Cement, and other great organizations. Besides pre-recorded courseware, thrice weekly, we hold live Zoom sessions (Tue, Thur and Sat at 7pm WAT) – Prof Ndubuisi Ekekwe, Tekedia Institute Lead Faculty.

Access to any Facyber Certificate program for free. Facyber offers online cybersecurity programs on policy, technology, management, and forensics.

Capstone Program

Here are the 12 tracks:

CLSM: Certificate in Logistics and Supply Chain Management

CBIS: Certificate in Business Innovation, Growth & Sustainability

CMAB: Certificate in Media, Advertising & Branding

CSBM: Certificate in Startup and Small Business Management

CIBA: Certificate in Business Administration

CPFM: Certificate in Personal Finance & Wealth Management

CMSM: Certificate in Marketing and Sales Management

CDBG: Certificate in Digital Business Growth

CIAM: Certificate in Agribusiness Management

CHRM: Certificate in Human Resources Management

CETS: Certificate in Exponential Technologies and Singularity

CBPM: Certificate in Business Transformation & Project Management

The program is completely capstone-based. Tekedia capstone is a research paper or a case study exploring a topic, market, sector or a company. It is the project component of Tekedia Min-MBA.

Theme: Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies

Introduction

Over the last few decades, digital technology has emerged as a very critical element in organizational competitiveness. It has transformed industrial sectors and anchored new business architectures, redesigning markets and facilitating efficiency in the allocation and utilization of factors of production. The impacts have been consequential: continents like Africa are moving towards knowledge-based economic structures and information societies, comprising networks of individuals, firms and states that are linked electronically and in interdependent relationships. In this program, we will examine this redesign within the context of fixing market frictions and deploying growth business frameworks in a world of perception demand where meeting needs and expectations of customers are not enough.

Program Time: Sep 14 – Dec 5, 2026

Venue & Format: Online via videos, articles, webinars, and flash cases. Program is self-paced which means you consume the materials at your own time and pace. It is completely online. Where you live or your time zone would not be an issue as program is not live-delivered.

Cost: US$170 (N120,000 naira). We have a payment plan, i.e. installment payment plan (email us for details)

Target Audience: This program is designed for professionals and students across functional areas like sales, marketing, technology, administration, legal, strategy, finance, etc across all business sectors and domains. The program is designed for:

Ambitious mid-level managers seeking to advance their careers by acquiring essential business knowledge and skills.

Busy professionals who value continued education but require a flexible alternative to a traditional MBA program.

Experienced professionals aiming to broaden their business acumen, enhance leadership capabilities, and explore new career opportunities.

Professionals in transition, committed to staying informed about business trends and developing skills for continuous professional growth.

Mid-level managers and executives across industries, driven to accelerate career growth and take on increased responsibilities.

Technology and innovation-focused professionals looking to strengthen business acumen and strategic thinking.

Aspiring entrepreneurs seeking a solid foundation in business management and growth strategies.

Consultants and advisors aiming to expand their knowledge base and provide comprehensive solutions to clients.

Professionals transitioning into new roles or industries, recognizing the value of upskilling for success.

Students and recent graduates seeking a competitive edge in the job market by combining academic qualifications with practical business skills.

Tekedia Mini-MBA program offers a flexible and comprehensive learning experience tailored to the needs of ambitious professionals, providing the tools and knowledge necessary to thrive in today’s dynamic business landscape. Participants will have the opportunity to acquire knowledge that has value and can be used in everyday business activities.

Learning Objectives: To innovate is to set a new basis of competition in an economy, business sector or market. Sometimes, it results in disruption. This program is designed for private (large, SMEs, startups, sole businesses), public and government institutions, and individuals. Participants will:

Master the mechanics of growth – the reward of innovation – through frameworks, cases and evolving strategies.

Understand how to undergo transformation journey that is fully aligned with corporate objectives through measurable and realizable benchmarks.

Acquire business capability tools that do not just RUN their firms but can TRANSFORM them.

Design corporate growth experiments in Lab sessions based on One Oasis Strategy, Aggregation Construct, Double Play Strategy, Accumulation of Capability Construct, and more.

ETC

Why Tekedia Institute

Interactive Online Learning: Engage with industry experts and fellow professionals through our state-of-the-art online learning platform, where you can access course materials, participate in discussions, and collaborate on real-world case studies.

Comprehensive Curriculum: Gain a deep understanding of key functional areas such as strategy, marketing, finance, operations, and more, equipping you with the knowledge and skills to excel in any business environment.

Practical Case Studies: Apply your learning to real-world scenarios through hands-on case studies and projects, allowing you to develop critical thinking and problem-solving skills.

Flexibility and Convenience: Access the program online from anywhere at your own pace, fitting your studies into your busy schedule without compromising your professional and personal commitments.

Expert Faculty: Learn from renowned industry practitioners and thought leaders who bring their expertise and real-world insights to the program, ensuring you receive the most relevant and up-to-date knowledge.

Benefits of Tekedia Mini-MBA

Enhance Your Leadership Potential: Unlock your leadership capabilities and develop the skills to lead teams, drive innovation, and navigate complex business challenges with confidence.

Master Business Excellence: Gain a holistic understanding of business functions, strategies, and best practices, enabling you to make informed decisions and contribute to organizational success.

Embrace Digital Transformation: Stay ahead of the curve by embracing digital technologies and leveraging them to transform your business and stay competitive in the digital age.

Accelerate Your Career: With the Tekedia Mini-MBA on your CV, you’ll stand out to employers, demonstrating your commitment to continuous learning and your readiness to take on new responsibilities.

Network and Collaboration: Connect with a diverse community of professionals, expand your network, and foster collaboration opportunities that can lead to future partnerships and career advancements.

Cost-Effective Investment: Enjoy the benefits of a comprehensive business education at a fraction of the cost of traditional MBA programs, maximizing the return on your investment.

We run optional three Live Zoom sessions (two weekdays and one Saturday). This provides a way for our members to ask our Faculty and experts live questions and get feedback.

Tekedia Mini-MBA certificate sample

Tekedia Institute offers certificates at the end of all programs.

Our Contact Email: info@tekedia.com

Refund policy is full refund within 6 days from start of a program; after that, none, but we can defer as requested.

Lead Faculty of Tekedia Institute

Prof Ndubuisi Ekekwe is the Lead Faculty of Tekedia Institute

PhD, Electrical & Computer Engineering, Johns Hopkins University, USA

MBA, University of Calabar, Nigeria

BEng Electrical & Electronics Engineering ( Federal University of Technology, Owerri, Nigeria)

Prof Ndubuisi Ekekwe invented and patented a robotic system which the United States Government acquired assignee rights. Dr Ekekwe holds two doctoral and four master’s degrees including a PhD in engineering from the Johns Hopkins University, USA. He earned undergraduate degree from FUT Owerri where he graduated as his class best student. While in Analog Devices Corp, he co-designed an accelerometer for the iPhone. A recipient of IGI Global “Book of the Year” award, a TED Fellow, IBM Global Entrepreneur and World Economic Forum Young Global Leader, Prof. Ekekwe has held professorships in Carnegie Mellon University and Babcock University, and served in the United States National Science Foundation Committee.

The South African press called him “a doctor of innovation” for helping organizations on the mechanics of business innovation, strategy, and growth. Since 2009, the Chairman of Fasmicro Group which controls many startups and entities has been writing in the Harvard Business Review. He was recognized by The Guardian as one of 60 Nigerians Making “Nigerian Lives Matter” on Nigeria’s 60th Independence Day (Oct 1, 2020).

Amazon delivered a strong quarterly performance, surpassing Wall Street expectations and sending its shares up roughly 7% in after-hours trading.

The results reinforced investor confidence in the company’s ability to balance rapid growth across its e-commerce, cloud computing, advertising, and artificial intelligence businesses despite a challenging global economic environment.

The earnings report highlighted Amazon’s continued success in expanding revenue while maintaining operational efficiency.

Strong consumer demand, improved logistics, and disciplined cost management helped the company exceed analyst forecasts for both revenue and profit.

Investors viewed the results as evidence that Amazon’s long-term strategy of investing heavily in technology and infrastructure continues to generate substantial returns. One of the biggest contributors to Amazon’s performance was its cloud computing division.

Although competition in the cloud market remains intense, AWS demonstrated resilience by attracting enterprise customers seeking scalable AI infrastructure and cloud services. The growing demand for generative AI applications has increased the need for computing power, positioning AWS as a key beneficiary of the AI boom.

Businesses across industries continue to migrate workloads to the cloud while adopting AI tools that require advanced computing capabilities. Amazon’s advertising business also continued its impressive expansion.

Advertising has become one of the company’s fastest-growing and highest-margin segments, benefiting from the massive amount of shopping data generated on Amazon’s marketplace.

Brands increasingly allocate larger portions of their digital advertising budgets to Amazon because it offers direct access to consumers at the point of purchase. This diversification has helped reduce the company’s reliance on traditional retail profits.

The retail division likewise showed encouraging signs of strength. Faster delivery speeds, improved inventory management, and expanding fulfillment networks have enhanced customer satisfaction while lowering operating costs.

Amazon’s ongoing investments in automation and robotics have streamlined warehouse operations, allowing the company to process orders more efficiently and improve profitability without sacrificing service quality.

Artificial intelligence has emerged as another important driver of Amazon’s future growth. The company continues to integrate AI across its ecosystem, from personalized shopping recommendations and warehouse optimization to cloud-based AI services offered through AWS.

Management emphasized that AI investments are expected to create new revenue opportunities while improving productivity across nearly every aspect of the business. This aligns with broader industry trends.

Where major technology firms are racing to build the infrastructure needed for the next generation of AI-powered applications. The market responded enthusiastically to the earnings announcement.

A 7% overnight jump in Amazon’s share price reflected renewed optimism about the company’s growth prospects and its ability to capitalize on expanding demand for AI and cloud services.

The rally also lifted sentiment across the broader technology sector, as investors interpreted Amazon’s results as a positive signal for digital infrastructure and enterprise technology spending.

Amazon appears well-positioned to sustain its momentum. Continued innovation in AI, steady expansion of AWS, growth in advertising revenue, and ongoing improvements in logistics provide multiple avenues for long-term success.

While challenges such as regulatory scrutiny, competitive pressures, and macroeconomic uncertainty remain, Amazon’s diversified business model offers significant resilience.

Overall, Amazon’s better-than-expected earnings demonstrate the company’s ability to adapt to changing market conditions while investing for the future.

The strong quarterly performance and positive investor reaction underscore Amazon’s status as one of the world’s most influential technology companies, with multiple growth engines capable of driving value in the years ahead.