: Rates, MPC, CRR")

It’s no longer news that Guaranty Trust Bank (GTB) crashed interest rates on its Quick Credit loan by 24% from 1.75% to 1.33%. This monthly 1.33% for 12 months will give an annual interest rate of 15.96%, if you factor in inflation at 11.98%; the real return that will go to the bank annually per customer is very thin at 3.98%. That’s too low by Nigerian lending standards; clearly, GTB has more in mind than profit/spread. They have disruption in mind. Now, who is disrupting who?

We will come back to the disruption topic. Currently, banks are battling with two forces, market forces and Central Bank of Nigeria (CBN); market forces led by interest rates and CBN through LDR (loan-to-deposit ratio). While LDR is saying you must lend businesses and consumers money, interest rate is shouting you must lend cheap. The hands of banks are tied, tied by crashing yields across all government securities – what can be likened to a ‘coup of rates’ on the banks by the government.

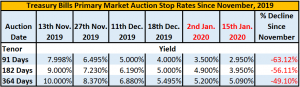

The average decline in treasury bill rates across all tenors in the last six auctions is over 55%.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

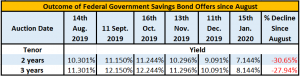

FGN (Federal Government of Nigeria) savings bond yields are down by over 29%.

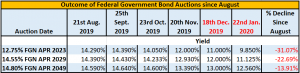

As for FGN Bond, the decline is over 22%. Taking a closer look at the trend (especially from November 2019), clearly, the government has a plan, something like a ‘coup of rates’. Despite these declines, banks, fund managers and PFAs (pension fund administrators) are still desperately after these government securities.

Government is saying we don’t need your cash, invest them in the real sector via loans. For the moralists, it won’t be wrong to ask “Why are we so keen on funding the inefficiencies of government when we complain of the same inefficiencies?”.

The first FGN Bond Auction for the year held on 22nd January 2020 recorded an oversubscription of more than 300%. Subscriptions received through competitive (N624.5b) and Non-competitive bids (N1.83b) totaled N626.33 billion. Following the auction, only N411.822 billion was allotted leaving another N214.508 billion stranded. Already, we have over a trillion stranded from other maturities and more will join them soon.

Conservatively, we can say hundreds of billions are stranded in the system but don’t be surprised when bankers argue in the line of ‘trillions’, anytime these debates take place, expect the CBN.

CBN raise CRR to 27.5%

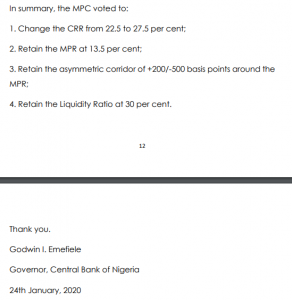

Yes, CBN turned up. At the first Monetary Policy Committee (MPC) meeting of the year held on 23rd and 24th January 2020, the CBN raised Cash Reserve Ratio (CRR) by 500bps to 27.5% from 22.5%. What’s CRR again?

CRR is a specified minimum percentage of the total deposits of customers, which commercial banks have to hold as reserves in cash with the CBN. The required reserve ratio is sometimes used as a tool in monetary policy, influencing the country’s borrowing and interest rates by changing the amount of funds available for banks to make loans with.

Simply put, CRR is a monetary policy tool of the CBN used to ‘lock up excess cash’. You may want to ask why is CBN locking up cash when I need loans for my business?

“The Committee is confident that increasing the CRR at this time is fortuitous as it will help address monetary-induced inflation whilst retaining the benefits from the Bank’s LDR policy, which has been successful in significantly increasing credit to the private sector as well as pushing market interest rates downwards.” MPC

Deposits of customers with banks are currently estimated to be over N16 trillion and growing, a 5% (500bps) increase in CRR will take less than a trillion naira from the system, as a result, we do not expect the increase in CRR to immediately impact the current status-quo.

Expect more insights on the outcome of the MPC during the week.

The fund managers don’t like taking risks, so even when securities return 0.5%, most will prefer to dump the cash there, they may even pay the government to accept their cash; that’s the kind of weird system we operate here…

We shall see which side that will get bored first, the three sides for now feel they could pull through; we see what happens.

Nice insights.

Yes I agree because the funds managers made a “promise” to most of Nigeria’s middle class with spare cash seeking minimum risk investments.

The critical questions we ought to ask ourselves is why those with spare cash mostly prefer this investment path?

I’d say Trust in the system.

Farmcrowdy and other similar tech startups are trying to prove a point through fund pooling/investment. I hope the trust is sustained.

It has to happen fast, that is why we equally working on something in that space, people can’t complain of small economy and yet not willing to help it grow bigger.