Wema Bank is having a great New Year. A LinkedIn user shared some nice stats which the bank posted on Twitter.

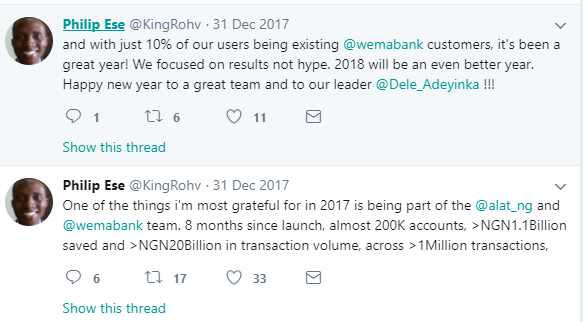

I remember Prof Ndubuisi Ekekwe‘s post 2 months ago about Wema Bank Alat. It’s apparent that Alat by wema bank will grow bigger than Wema Bank or most banks in Nigeria in few years. According to Philip Ese via his twitter handle shared that, they now have almost 200k accounts since Alat was launched 8 months ago, ?1.1 Billion saved and ?20 billion in transaction volume across 1 Million transactions and that only 10% of the users are existing wema bank Customers.

In that post, the user linked to my piece on Wema Bank’s ALAT where I made bold predictions that in future, Wema Bank could either be folded into ALAT or ALAT be divested as a separate entity.

ALAT is the first step for Wema Bank. In the next few years, depending on its progress, ALAT can be divested from Wema Bank, to allow it to compete more aggressively in the African market without being tethered to a bank and the associated regulation. The regulation is important and there is nothing wrong with that: banks like Wema Bank take customer deposits, unlike most fintechs, and should be regulated. So, ALAT can become an operational arm of Wema Bank while the bank remains a dumb pipeline, typical of most traditional banks today (i.e. not much intelligence due to lack of deep insights), to support what that modern banking named ALAT does. Perhaps in 10 years, Wema Bank may even simply change its name to ALAT if this new modern banking solution evolves into its future.

The original tweets are reproduced below

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

The Implications

These numbers are significant because the implication is that ALAT is driving growth in Wema Bank. Wema Bank has about 1.5 million customers and hopes to push the number to 3 million through ALAT by 2020. Within 8 months, they have 200,000 on-boarded. My focus is not really the 200,000 customers in ALAT but the fact that Wema is attracting new people into Wema: “with just 10% of our users being existing @wemabank customers”. This is significant for the relatively small bank. Getting 90% of new customers through ALAT is very great. It would have been bad if it was only moving current customers to ALAT. So, ALAT offers growth to the bank.

ALAT is a bank, and it can become a truly African banking institution, if it pursues new opportunities in Africa, with growth typical in most highly scalable businesses. I am expecting the management to make ALAT a pan-African “bank”, and use it to redesign the banking experience for young people which it continues to pursue. Wema Bank is working. It is on ALAT now and that is a good thing.

There are many strategic things which the bank can do to scale ALAT across the ECOWAS region. The product has demonstrated that it can offer value to non-Wema customers since 90% of users are new to the bank. This is a fintech within a bank and the bank must take it and run with it. The bank needs to drive it with the fierce urgency typical in a high growth scalable business with a low marginal cost and a high scalable advantage. There is nothing that can stop this product from scaling when you look at the product design.

ALAT is digital which means that its marginal cost of adding a new user is close to zero, and with that capability it is not bounded by geography within Nigeria where the bank has license to operate. I expect ALAT 2.0 to anchor a redesign in Wema Bank where most of its branches would be closed even while making it easier for customers to do business. That will improve its cost-to-income ratio even when growing its customer base. Most Nigerian banks saw their digital products as extensions of their traditional products; Wema Bank’s ALAT was the only one that built something sequestered from the current for an opportunity into the future. From the naming and marketing, they diminished the bank to allow ALAT to glow. In other words, ALAT does not need Wema Bank and that removed any potential innovation hangover in the product design.

ALAT has sent an alert to the Nigerian banks. Wema Bank needs to sustain this product because it is one of the finest fintech products in the nation. It needs to use this product to drive its agency banking by linking it to voice banking. Also, that location-agnostic intra-African remittance should not be far away. ALAT is sending alerts and that is a good thing.

Here, I explain my reason for liking the ALAT Strategy

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube

ALAT is truly a fine digital bank by Wema. It would be great to see ALAT become a pan-African bank, as you have mentioned. The unbanked but ever-mobile in Africa would be the greatest beneficiaries.

Yes, ALAT has a promising future.