It is no longer news that the African Continental Free Trade Agreement (AfCFTA) became effective May 30, 2019 with 54 of the 55 African Union nations agreeing to a borderless and tariff-free trade agreement. The number of signatories to this agreement makes it the largest in the world in terms of participating countries since the formation of the World Trade Organization (WTO) in January 1995.

Low Intra-African Trade

According to the United Nations Conference on Trade and Development (UNCTAD), at the continental level, inter-regional trade was highest in Europe followed by Asia and North America. Inter-Europe trade, as at 2017, stood at 68% while inter-Asia and Northern America trade were 59% and 31%, respectively. Within the same period, inter-Africa trade recorded 17%, the lowest of any region globally. With an estimated population of 1.2 billion people and gross domestic product (GDP) in excess of US$3.4 trillion, Africa not only has the market but the potential for organic growth through strategic, complementary and mutually-reinforcing trade partnerships.

Benefits of the African Continental Free Trade Agreement

AfCFTA promises the diversification of Africa’s industrial export by encouraging a transition away from extractive commodities such as oil and minerals through continental economic integration, harmonization of customs/border checks and free flow of human and material resources. The agreement also advances the African Union Agenda 2063 which envisages a single African air transportation market. Besides the direct economic benefits to airline operators and the revenue gains to governments within the region, the air transport liberalization is expected to reduce the cost of air transportation. The welfare gains therefrom could be channeled to other alternative uses to increase the quality of life of Africans. However, for AfCFTA to realize its full potential and for Africa to possibly catch-up with the Western world, the continent must address, as urgent and important, its infrastructure deficit which the African Development Bank (AfDB) estimates to be about US$170 billion annually.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Infrastructure Development, a Necessary Condition for AfCFTA’s Effectiveness

Why is infrastructure important to AfCFTA? The Economist argues that good ports are perhaps more important to Africa than any other region since 90% of trade happens by sea. It is, therefore, worrisome that the United Nations Office of the Special Adviser on Africa (UN-OSSA), reports that poor port facilities add 30-40% to intra-African trading costs and Foreign Direct Investment (FDI) and this could more than offset the potential gains of a tariff-free continental trade agreement. Empirical evidences suggest that, “the poor state of infrastructure in Sub-Saharan Africa cuts national economic growth by 2% points every year and reduces productivity by as much as 40%”, while “the output elasticity of infrastructure in South Asian countries ranges between 0.24 and 0.26 percent”. The implication is that investment in infrastructure contributes about a quarter to the growth outcomes in South Asia. Africa’s Pulse, a biannual analysis of African economies by the World Bank, reports that closing the infrastructure quantity and quality gap relative to the best performers in the world could increase per capita GDP growth by 2.6% per year.

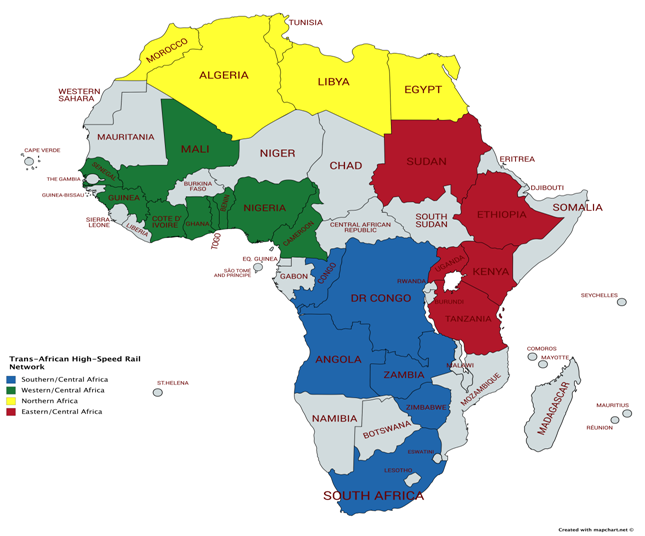

What can Africa do to address this infrastructure shortage? Just like France, Spain, Italy, Germany, Austria, Sweden, Belgium, the Netherlands, Russia and the United Kingdom are connected to a cross-border high-speed railway through the Trans-European high-speed rail network, sub-regional economic giants like Nigeria, South Africa, Egypt and Kenya should be connected through a Trans-African high-speed rail network with connecting stations through other African countries on the rail link as shown on the map below.

Created by the Author using mapchart.net

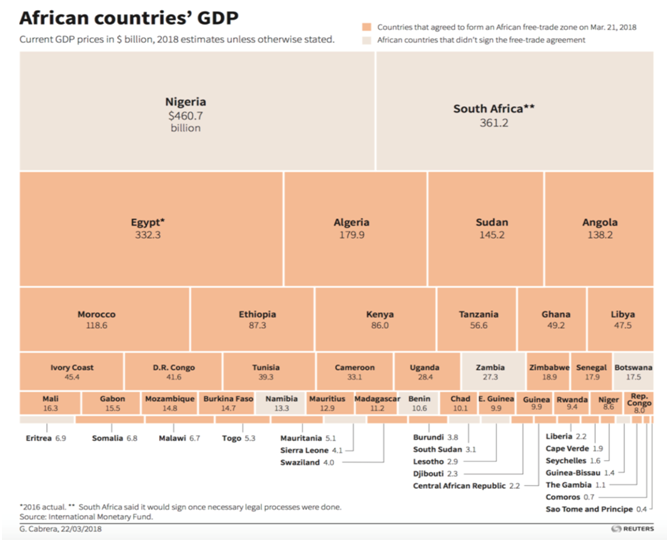

This proposal is based on the size and contribution of countries along the high-speed rail network to Africa’s overall GDP as shown on the chart below. Investment on the Trans-African high-speed rail network is expected to not only reduce the cost of cross-border transportation and transaction costs but also ease the pressure on seaports and airports.

Source: International Monetary Fund/Reuters/World Economic Forum

Financing Africa’s Huge Infrastructure Deficit: Challenges and Opportunities

Following the first Africa Investment Forum in Johannesburg, South Africa in May 2018, where discussions were held as to how to further strengthen Africa-led response to the continent’s infrastructure-financing deficit, the AfDB in November 2018 approved an equity investment of US$50 million in African Finance Corporation (AFC). According to the AfDB, “the equity investment is aimed at strategic partnerships with some Development Finance Institutions (DFIs) that have comparative advantage at regional or sub-regional levels in certain strategic sectors”. Given that bridging Africa’s infrastructure deficit would require about US$170 billion annually (which is 5% of the continent’s GDP), the reasonable question before policy makers at the regional level is where will the money come from? Should Africa rely on Nigeria, South Africa and Egypt that cumulatively account for more than 50% of the continent’s GDP? Can Africa fund Africa’s infrastructure need with Africa’s resources or should we seek external assistance?

What financing options can Africa explore? AfDB is expected to lead the charge here by structuring loan syndication partnership deal with other multilateral development banks (MDBs) like the World Bank, European Investment Bank, International Development Association, Asian Development Bank and Inter-American Development Bank. Loan syndication with a consortium of MDBs has the added advantage of risk diversification. This consortium of MDB lenders with the ratification of the African Union (AU) can select through competitive bidding, a concessionaire with expertise in rail construction and management to guarantee the viability of their investment. The elegance of structuring concession contracts that bundle construction and service-provisions together with a single private operator is that it is generally believed to be incentive-efficient and yields the best outcome.

Alternatively, Africa could also explore financing through Sovereign Wealth Funds (SWFs). With a global cumulative asset of over US$7 trillion, SWFs are better placed to finance large scale infrastructure of this magnitude. Policy Analysts tend to prefer SWFs to institutional investors like Pension Funds because SWFs have longer investment horizon and they do not have substantial explicit liabilities (specific obligations created by law or contract, that government must settle). Additionally, SWFs are not subject to the “prudent person” investment regulation, which prevents large exposure to long-term infrastructure projects.

Africa Infrastructure Bond Market could also be a financing option where the AfDB together with sub-regional and national development banks like ECOWAS Bank for Investment and Development (EBID) and Development Bank of Nigeria (DBN) create infrastructure development bonds with different tenors and yield. This would encourage Africans (within and outside the continent) to invest in Africa and with “strength in numbers” (credit to the Golden State Warriors), Africans can build the Africa of our dreams.

Although the United Nations Economic Commission for Africa (UNECA) has estimated that AfCFTA could potentially boost intra-Africa trade by 52% by 2022, but to realize that estimate, the task of addressing Africa’s infrastructure deficit must be accorded the urgency and importance it deserves. Until then, like Jaramogi Oginga Odinga titled his 1967 Classic, it is not yet uhuru (freedom in Swahili) for Africa.