“Gold clingeth to the protection of the cautious owner who invests it under the advice of men wise in its handling.” —The Third Law of Gold

The quote above is culled from The Richest Man in Babylon by George S. Clason. Recently, Prof Ndubuisi Ekekwe expounded it in How You Can Invest N10 Million in Nigeria Right Now. His investment counsel came at the most appropriate time when all interest rates are crashing with the Treasury Bills, TB, leading the pack. Before now TB has been a lucrative and the safest portfolio investment but it has lost its attractiveness and thrown investors into a dilemma.

Investors are having tough times in deciding the next best investment choice to secure and grow their wealth. And, according to the possible alternatives listed by the erudite professor, fixed deposits tops the list. He said,

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

“If you fix the money for 3 years, in a good bank in Nigeria. The Nigeria Deposit Insurance Corporation (NDIC) insurance will cover a part of the N10 million even in a rare case the bank collapses! So, your risk is fairly managed, broadly, for 10 million, the interest rate cannot be more than 10% looking at some numbers from most Nigerian banks. In short, the average for 10 million fixed deposits, for three years is about 6 – 7%.”

I find his position to be true of commercial banks by my validation. Two months back, I visited the major commercial banks to get their deposits rates and compare with that of AB Microfinance Bank under the guise of an investor. The variance was very significant.

I bet you are trying to retrieve the file of AB Microfinance Bank from your memory bank, just click here to know more. Hold on, before you click, know that AB MfB is one of the few national microfinance banks in Nigeria. It’s the largest German owned firm by number of employees (over 1000). It has been in operation since 2008 with 23 branches in Lagos, Ogun, Oyo, and Ondo states. Five more branches are expected to kick start in the five Southeastern states by the first quarter of 2020.

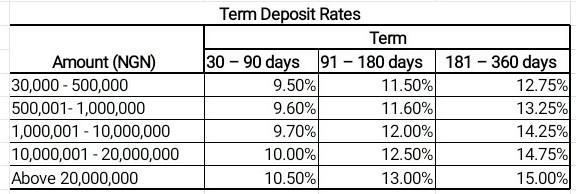

The highest rates on a fixed deposit hitherto offered by other banks is our starting point. How are we able to do this, you ask? Our investment is long term, and our clients are not the few macro borrowers who always fail to pay back their loans. We service the long neglected millions of the micro, small, and medium enterprises whose risk of default is manageable. This guarantees our profitability and continuity. The table below shows our current rates on time/fixed deposits.

Note:

- Interest rates are subject to 10% withholding tax (WHT).

- Interest rates reduction in case of early withdrawal:

- By 50%, if withdrawal is in the first half of the term; and

- By 25%, if withdrawal is in the second half of the term.

- If interest is paid monthly, the above interest rates are reduced by 0.5%

- You can also negotiate for higher rates than 15% for amounts above 20 million.

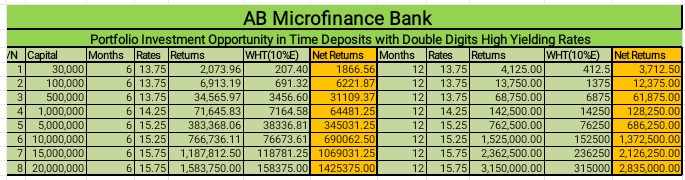

In the second table below, I showed the net earnings on some specific amount of money fixed for 6 months, and 12 months. The net earnings were determined by deducting WHT from the earnings at maturity.

In conclusion, another eternal truth from the Richest Man in Babylon will be helpful.

“Wealth, like a tree grows from a tiny seed. The first copper you save is the seed from which your seed of wealth shall grow. The sooner you plant that seed, the sooner shall the tree grow. And more faithfully you nourish and water that tree with consistent savings, the sooner you may bask in contentment beneath its shade.”

Benefits of Investing in AB MfB Term Deposits

- Minimum risk portfolio with predictable yield.

- High and stable interest rates above the level of inflation of 11.98%

- Flexible amounts and interests determined by clients preferences.

- Roll over option.

- Easily and readily available when demanded by clients.

Why not invest with AB MfB today? Contact David Gani at David.Gani@ab-mfbnigeria.com or call 0703 744 7482

Mitigate that risk!