- By Samson G. SIMON, Ph.D., CPLP

- Head, Research & Hubs Coordination, @Opolo Global Innovation Limited, Ikoyi-Lagos.

INTRODUCTION & BACKGROUND

Nigeria’s fiscal mess will definitely require the new Tinubu’s government to take urgent and far-reaching measures to fix the problem. For it is unsustainable to continue on the particular trajectory it met when it came to power few weeks ago. Opinions seem divided: One side of the divide; populated mainly by the led as well as professional economists; thinks Nigeria has a debt problem. However, the other side of the divide; where you have the fiscal authorities, most especially the crop in charge of the policy for the last eight years; believes that Nigeria’s problem is a revenue one, not a debt one.

On the whole, Nigeria’s problem is clearly both. It has over N12.1 trillion in fiscal deficits in the 2023 budget alone, with overall national debt projected at a whopping N77 trillion when CBN’s Ways and Means of N23 trillion is securitized by the end of the last dispensation. The CBN advances attract N1.8 trillion yearly in interest payments, and in 2022, a whopping 81% of revenue was used to service debts. Debt service to revenue ratio even exceeded 100% in the first quarter of 2022. Similarly, as it is projected now by the World Bank to be in the region of 102. 3% for the current year. Furthermore, the World Bank is projecting the same ratio to double what was experienced in 2022 to be 160% by 2027. Hence, the problem is both revenue and debt.

The new administration should deploy all tools to ensure fiscal sustainability by broadening the tax base and reducing leakages and the unnecessary costs of tax administration. Urgent reforms are needed to avert the looming danger as Nigeria approaches a fiscal cliff, if it is not there already.

When the public sector embarks on borrowing to fund its budget that will crowd out the private sector. This is possible as a result of increase in the costs of borrowing. This ultimately reduces demand for borrowing hence spending by corporates and individuals.

More so, if a government is raking in huge revenues, there may be no need to borrow as it has a surfeit of resources to meet its needs. And to boost this income, the authorities can deploy technology. Financial Technology (FinTech) can be maximised to increase government revenue. The new government can use FinTech to set up a system that helps it in formulating, implementing, and executing its fiscal policy, particularly for those ones around non-tax collections, taxes and even spending in an efficient way.

TYPES OF FINTECH

There are three types of FinTech. One type is mobile money; an example can be found in Kenya using M-Pesa by Safaricom etc. M-Pesa accounts for a whopping 85% of non-cash transactions. Mobile money is different from mobile banking. While the former can be done even without a bank account, the latter has to do with e-transactions using bank accounts. The second type of FinTech is an internet-based payment system (e-payment). This type is better than mobile money because it can transact much larger amounts than what mobile money will normally allow. This is so because the internet and digitisation not being available to mobile money. Third, digital money such as CBDC (Central Bank Digital Currency), e-Money, and stablecoins are assets that have the properties of traditional money like cash and bank deposits.

FinTech can be deployed by the government to boost financial inclusion which the monetary authority has tried so far but does not seem to be making much headway. FinTech helps financial inclusion for the unbanked or underserved communities. When the financial exclusion of people is reduced through the deployment of financial technology, this will widen the tax net and the tax base hence improving government revenue. The authorities can rake in non-tax revenue for royalties on the extractive industries, dividends from Government Owned Enterprises (GOE) payments for government delivery of goods and services such as passport issuance, port fees, fines, and penalties, health, and education. FinTech will help accelerate the financial inclusion rate which at present is at a pathetic 0.09% per year while almost 40 million Nigerians remain excluded from the financial system. Hence, including them will boost the economy and bring about more revenue for the government.

CBDC will help improve efficiency, access and cut costs for transactions; help expand tax base, combat illegal activities, and optimise government disbursement of its benefits.

HOW FINTECH CAN HELP THE GOVERNMENT

Setting up tax collection platforms just like India did in creating a portal for non-tax revenue where all fees, fines, and charges are paid. No cash transactions should be encouraged, as making all payments cashless will cut down to almost nothing the chance of money being stolen or any other leakages. It will also make the population have confidence in the process and the institutions rendering the service or providing the good. Rwanda and the Dominican Republic equally have deployed FinTech to reduce waste and ensure any income meant for the government gets to the government unfailingly. Tanzania too has deployed technology in its public finances to improve and modernise tax collection. Brazil too with its PagTousoro has helped it improve its non-tax income. Senegal’s M-Tax (Mobile Tax) uses SMS and USSD for businesses to pay taxes. It has digitised tax payments hence making it more efficient, transparent, and seamless. FinTech can help reduce the rate of tax evasion which is one of the major problems for the taxman.

Other benefits accrue as a result of bringing in financial technology. The deployment of Financial Technology (FinTech) helps the government to substantially increase the speed of its transactions such as making and receiving payments. It helps facilitate government interactions with citizens in areas like Governments-to-People, People-to-Governments, Governments-to-Businesses, and Businesses-to-Government. It will help in the collection of tax and non-tax revenue as well as debt management. Generally strengthening public finance management. FinTech will help strengthen accountability, make reliable audit trails, enhance financial data collection, and improve budget planning. When tax collection is digitised this will lead to: better compliance hence higher revenue; automation leading to low costs of tax administration; greater accountability and transparency in tax administration; broader tax base as it will reduce Nigeria’s informal economy; and an abundance of data for effective decision-making.

NIGERIA’S DEBT SERVICE TO REVENUE RATIO

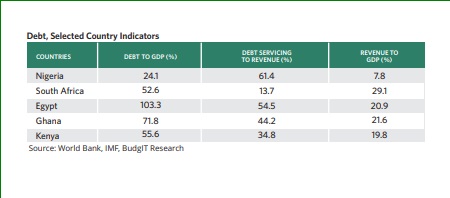

Nigeria’s debt-to-GDP ratio is relatively low. As the table shows, Nigeria’s public debt is less than a quarter of GDP which is clearly below the DMO’s self-imposed limit of 40%. Way below the IMF/World Bank’s recommendation of 55% for countries within Nigeria’s peer group. While the Debt-to-GDP ratio is clearly not a problem, debt servicing to revenue ratio as well as revenue to GDP are clearly huge problems. For example on the table above, Nigeria has the least percentage points for revenue to GDP. This means it is the worst performer amongst this set of its African peers like Egypt, South Africa, Ghana and Kenya. Nigeria has a value below 8% while South Africa has almost four times to arrive at 29%. For the debt service to revenue ratio relative to other African nations; Nigeria is at 61.4% almost twice Kenya’s level at 34% and almost 5 times South Africa’s which at 13.7% is relatively extremely measly. This shows Nigeria uses 61 cents of any currency 1 dollar to service debts. As if the numbers are not bad enough they even got worse at over 80% last year.

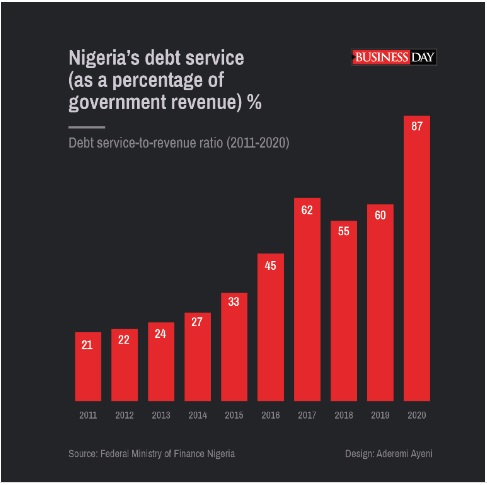

As shown above, Nigeria’s debt service costs as a percentage of its revenues have not only been climbing but also spiking in recent times. Meaning, it’s in fiscal distress with less and less fiscal space. This calls for drastic changes to stop the slide in its tracks. And financial technology can help with a lot of these challenges.

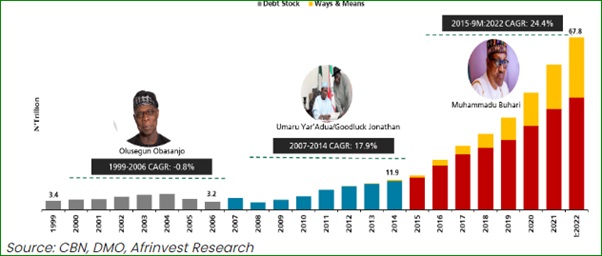

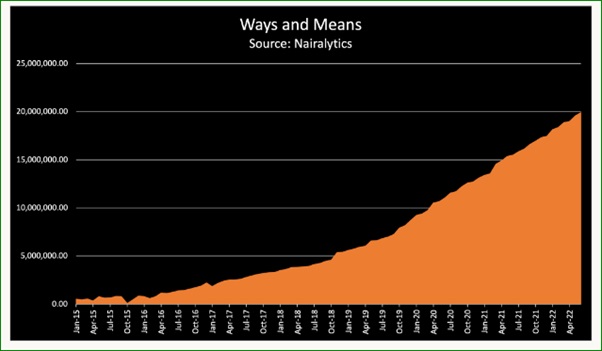

CBN’S WAYS & MEANS AS WELL AS NIGERIA’S DEBT STOCK

While the CBN ACT 2007 allows the government to take out loan from the monetary authority to solve urgent financial difficulties, however, this has been obviously abused by the current government. The tables below show how the current dispensation has come to rely too much on the CBN for the financing of its activities.

The law says only 5% of previous year’s revenues should be owed by the government at any particular time. Nonetheless, the government has not only disregarded that and now owes several folds of the previous year’s revenues. The law also says, if the government doesn’t pay back, the powers by the CBN to lend to it cannot be exercisable. The CBN still lends to the government. Thirdly, the law says these borrowings from the CBN should not be securitised. Nevertheless, the government has done just that!

CONCLUSION

While deploying financial technology (Fintech) can help the new government plug leakages; raise more revenue; spend better; and provide the dividends of democracy in great measure. This does not mean that it is all sunshine as challenges too abound. The privacy of the participants concerned as well as the danger of cyber crimes can be daunting.