A global race to build out artificial intelligence infrastructure is now colliding with the consumer electronics market, and smartphones are emerging as one of the first casualties.

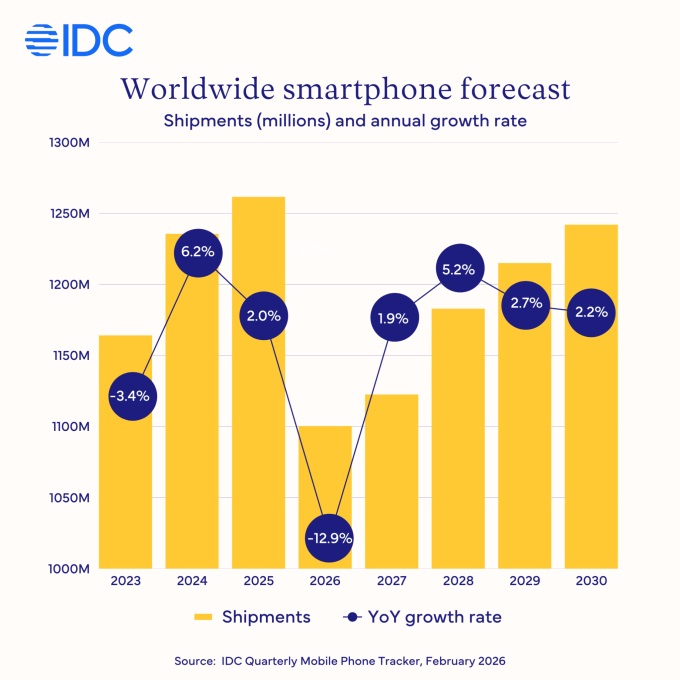

The International Data Corporation (IDC) projects that global smartphone shipments will plunge 12.9% this year to 1.12 billion units, down from 1.26 billion devices shipped in 2025. If realized, it would mark the steepest annual contraction in more than a decade, a stark reversal for an industry that had been stabilizing after years of post-pandemic volatility.

At the center of the disruption is a severe shortage of RAM, driven by surging demand from AI-focused data centers and high-performance computing environments. Memory manufacturers are reallocating capacity toward high-margin server-grade DRAM and high-bandwidth memory (HBM), components essential for training and running large AI models. Smartphones, which rely heavily on commodity DRAM, are being squeezed out in the process.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Register for Tekedia AI Lab.

“The memory crisis will cause more than a temporary decline; it marks a structural reset of the entire market, fundamentally reshaping long-term TAM (Total Addressable Market), the vendor landscape, and the product mix,” said Nabila Popal, senior research director with IDC’s Worldwide Quarterly Mobile Phone Tracker.

Her framing points to more than a cyclical downturn. For years, the smartphone market has been defined by incremental innovation, longer replacement cycles, and intense price competition. Now, input cost inflation is colliding with maturing demand, forcing a reassessment of volume expectations and profitability models.

Prices rise, consolidation looms

IDC expects smartphone average selling prices (ASP) to climb 14% this year to a record $523. The pricing surge reflects both higher memory costs and the broader inflationary pressures embedded in semiconductor supply chains.

“We expect consolidation as smaller players exit, and low-end vendors face sharp shipment declines amid supply constraints and lower demand at higher price points. Although shipments will witness a record drop, Smartphone ASP is projected to rise 14% to a record $523 this year,” Popal said.

The squeeze is particularly acute in the entry and mid-tier segments, long considered the volume backbone of the industry. These devices operate on thin margins and are highly sensitive to component cost swings. When memory prices spike in multiples, vendors face a binary choice: pass costs on to consumers or downgrade specifications.

Carl Pei, co-founder and CEO of Nothing, underscored the pressure facing manufacturers.

“Brands now face a simple choice: raise prices by 30% or more in some cases, or downgrade specs. The ‘more specs for less money’ model that many value brands were built on is no longer sustainable in 2026,” he said.

He added that “some markets, particularly entry and mid-tier segments, are likely to shrink by 20% or more, and brands that have historically dominated these segments will struggle.”

The comment signals a broader shift in competitive dynamics. Smaller brands without scale advantages or long-term supply agreements may struggle to secure memory at viable prices. Larger vendors with diversified portfolios and stronger balance sheets are better positioned to absorb volatility, potentially accelerating consolidation across the Android ecosystem.

Emerging markets under strain, relief distant

IDC forecasts that the Middle East and Africa will see shipments fall by more than 20% year-over-year. China is projected to decline 10.5%, while Asia Pacific (excluding Japan and China) is expected to drop 13.1%.

These regions are critical to global volumes. In many of them, smartphone penetration remains below saturation levels, and growth has historically been driven by affordable devices. A double-digit contraction there suggests that price sensitivity is already biting.

Higher ASPs in cost-conscious markets risk elongating replacement cycles even further. Consumers may delay upgrades, opt for refurbished devices, or shift toward older models with discounted pricing. That dynamic could dampen the industry’s long-term Total Addressable Market, reinforcing IDC’s “structural reset” thesis.

The outlook also diverges sharply from earlier projections. Last year, Counterpoint estimated a relatively modest 2.6% decline in shipments. IDC’s 12.9% forecast highlights how rapidly the memory supply-demand equation has tightened, largely due to the intensity of AI-related capital expenditure.

IDC expects RAM prices to stabilize by mid-2027, implying that the industry could face at least another year of elevated component costs. Until then, smartphone makers will operate in an environment where volume growth is constrained not by lack of consumer interest in connectivity, but by competition for silicon from AI infrastructure.

The broader signal is that capital and capacity are migrating toward AI. As hyperscalers and enterprises pour billions into data centers, semiconductor supply chains are being reprioritized. Smartphones, once the dominant driver of semiconductor demand, are now competing with AI workloads for the same memory resources.