I have written so much about Jumia when it was a pure ecommerce company. I never liked the business model then. But when Jumia changed and added payment, I became a fan. My change of heart was supported by data: the world has not seen any successful ecommerce company without double play. In other words, you cannot make money just by doing ecommerce, especially in emerging economies. Rather, you add something on that ecommerce, and use the transaction volume which comes from ecommerce to make money from something else. Alibaba became better with Alipay, its paytech unit. India’s Flipkart depended on PhonePe to become a better company. Even Amazon relied on AWS to find favour before Wall Street.

Jumia has gone paytech and today is one of the largest fintech companies in Africa with more than 6 million users. Wall Street has noticed and its stock is rebounding. In the last 3 months, it has doubled its market cap, and the trajectory looks positive.

Jumia has dramatically underperformed the market since its August IPO at $14.50 a share. The Africa-focused e-commerce company has struggled with fraud allegations on its platform and thin margins in some of its markets. However, Jumia’s revenue is still growing at a respectable pace, and the company has a convincing plan to turn things around over the long term.

To boost margins, management has divested from less profitable markets such as Rwanda, Cameroon, and Tanzania to focus on larger markets like Egypt, Nigeria, and South Africa, where consumers have larger purchasing powers and better access to the internet.

Internet access is a big driver of online retail adoption, and Jumia is well-positioned to benefit from several promising projects aimed at getting more Africans online.

American tech giant Facebook has partnered with several top telecom companies to build a 23,000-mile subsea internet cable called 2Africa to link 16 African countries to Europe and the Middle East. The connection is expected to go live by 2023 or 2024 and dramatically reduce bandwidth costs and improve internet speeds and access on the continent — three massive enablers for Jumia’s revenue growth.

Jumia reported first-quarter earnings on May 13, and the results show resilience amid the COVID-19 pandemic. Annual active customers grew by 51% to 6.4 million, while marketplace revenue grew 22% to 19.1 million euros ($21.48 million).

Comment on LinkedIn Feed

My responses to some comments

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

#1…It is important that those who have different views on Jumia are not seen as bad people. Before Jumia, there were Kalahari, Mocality, etc and all ended up in bankruptcy. People were simply telling Jumia one thing: ecommerce as a solo focus has never worked anywhere in the world.

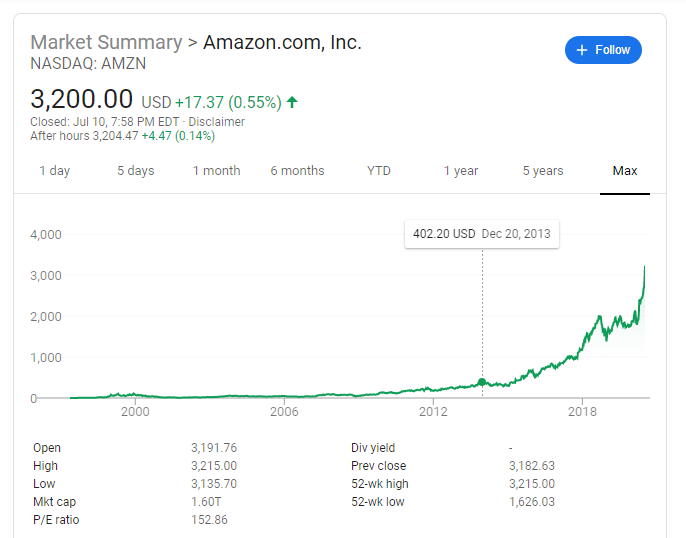

Amazon was a lousy company before AWS and without AWS, Amazon may not be worth half of its current value. The good news is that Jumia is listening and adding those things people told it. For years, analysts wrote the same thing people wrote about Jumia on Amazon. Amazon responded by bringing a double play in AWS.

Amazon ecommerce changed retail. But AWS changed global technology forever.

Between 1994 to 2006 when AWS launched, Amazon stock was FLAT. It was when investors saw AWS impact in 2008 that its stock began to rise. When you write Amazon without that double play context, your readers may not see the big picture. Jumia as a pure play ecommerce has no future but with JumiaPay it is promising.

#2: To know those plays, I will go to things that would improve marginal cost since that is a huge determinant of scaling. Marginal cost = transaction cost + distribution cost. When a play adds payment, you reduce transaction cost. But the distribution cost is all atom (i.e all meatspace friction) which becomes harder when there is no national postal service. So, any 3rd play would be all players coming together to build a national postal network. If they do that, ecommerce will pick up in Africa. Unfortunately, no investor will give any company that type of money.

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube

In other words, Jumia is now reporting numbers that matter to Wall Street folks, not that it has cracked ecommerce code in Africa.

This is how IMF and World Bank develop and deploy frameworks that can at best underdevelop Nigeria and Africa, and yet lecture us that it’s all we need to join the league of Tier 1 nations.

The dichotomy between market valuation and friction fixing cannot be starker.

Your mind is simply amazing. Yes, it is about business for Wall Street. Fixing friction is another story for another day. If fintech does it for Jumia, that is all that matters, ecommerce or no ecommerce.

Yes maybe it’s making money since jumia now have decided to force it’s partners in the delivery department to lower the price by force. That affecting the delivery agents, for instance they’ve come up with something called consolidation. Paying a rider one item out of ten plus and even twenty plus deliveries just because it’s of one person doesn’t make sense. That’s how jumia is milking the common person who does his job diligently but ends up being paid less in the name of take it or leave it.it’s…….