Before any living thing can thrive, the survival aspect of life must be addressed. Food, water, clothing, sleep, and shelter are all necessities for both animals and humans. Other than sleep, which is a natural part of the list, others cannot be obtained without some money. Money, whether borrowed or earned, remains the most important factor in acquiring the necessities. Earning and accessing money are not always easy depending on the environment due to the disparity that exists among the populace. This is the primary reason for various political and economic policies aimed at bridging global income disparities. Business leaders aren’t taking a break from developing financial products and services, especially technology-driven ones, as political leaders and civic space participants continue to develop strategies for closing the gap.

However, as new fintech products and services are introduced on a daily basis, concerns about the efficacy of the offerings grow. Nigerian policymakers and the government have repeatedly warned citizens not to patronize illegal fintech companies. Despite the warning, interest in the companies is growing. Our analyst’s string search on Google Search Engine for “mobile app loans in Nigeria” yielded over 5 million results.

Using the same search term, digital observation analysis reveals that people who are interested in using loan apps from companies are asking a number of questions. The questions such as which app can borrow me 200k in Nigeria? What app can borrow me money instantly? What app gives 50000 loans? Which app gives highest loan instantly in Nigeria? Who can help me with money urgently in Nigeria? Can loan app block my BVN? Which app can I borrow money without asking of BVN? Which loan app is best and reliable in Nigeria? and How do I get loan apps to stop calling my contacts? were found.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

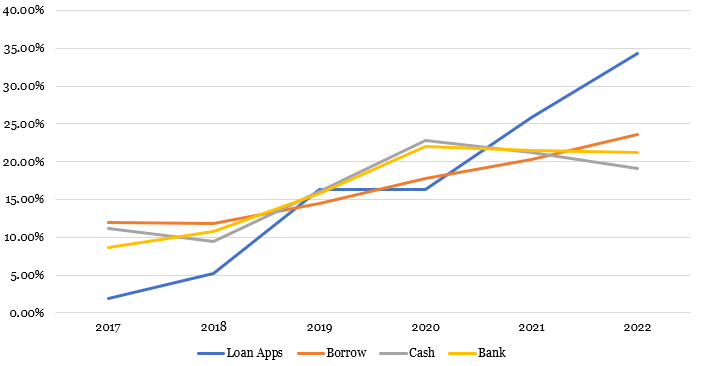

In addition to these analyses, our analyst looked at how Nigerian internet users behaved when looking for information between 2017 and 2022. Analysis reveals that the desire to learn about and comprehend loan applications began to rise in 2018 along with the desire for quick cash. The data indicate, however, that turning to banks for urgent cash may be more effective than using loan applications. This applied to borrowing as well. The data also shows that Nigerian netizens in 2019 who needed urgent cash and were interested in borrowing could be said to have approached the apps for their needs. A small but noticeable disparity was found in the data for 2020.

The data show that during the year, netizens who wanted to borrow got their needs met through apps rather than going to banks. Meanwhile, the close relationship that existed between cash interest and banks suggests that netizens went to banks to withdraw their money or borrow from banks. Our data also show that the pattern of information seeking displayed by netizens in 2018 is not dissimilar to what was observed in 2022, where interest in cash and banks was slightly aligned while interest in loan apps was distant.

Exhibit 1: Nigeria’s Netizens information seeking behaviour in the context of credit and lending

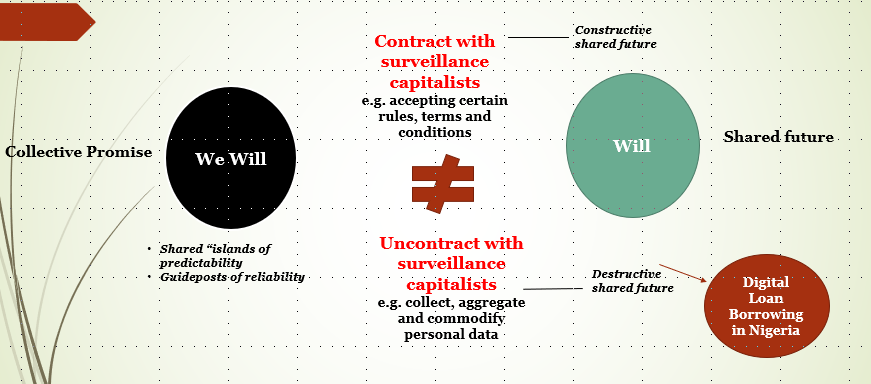

Like political leaders, business leaders want to assist people who need financial assistance in order to own the necessities of life. The borrowers are typically made aware of certain guidelines, conditions, and rules as the money is made available through the apps. According to Shoshanna Zuboff’s book The Age of Surveillance Capitalism, this shows how willing the lenders are to provide the borrowers with a positive shared future. In other words, by providing quick access to the money they need, mobile loan companies help Nigerians achieve their desired futures as soon as possible. In some instances, some of the companies specifically state that loans without collateral will be given, according to our checks. “In reality, all you need to do is to register by providing your personal details. After registration, you can borrow as low as N1,000 or as high as N200,000 with considerable interest,” a part of terms and conditions from one of the apps points out.

Although it is possible to argue that the borrowers entered into a legal agreement with the businesses based on the agreed-upon terms and conditions of repaying the loan, it is instructive to note that gathering, aggregating, and automatically contacting the borrowers’ personal contacts for the purpose of alerting loved ones, coworkers, family members, and friends when the borrowers’ default in repaying amounted to destructive shared future, is a common practice. This, according to Zuboff, is uncontractual. Therefore, the shared future that Nigerian mobile app money lenders promised in their numerous marketing and communication materials is being violated. Not disclosing the use of personal relationships to effect repayment amounted to embarrassment and reputational harm for the borrowers.

Exhibit 2: Mobile Loan Apps in the Midst of Shoshanna Zuboff’s the Age of Surveillance Capitalism