Asset manager LeverageShares announced plans to debut the world’s first 3x and -3x leveraged exchange-traded products (ETPs/ETFs) tracking Bitcoin (BTC) and Ethereum (ETH) in Europe, with listings expected on Switzerland’s SIX exchange as early as next week.

This move marks a significant expansion of leveraged crypto exposure in the region, building on LeverageShares’ existing suite of high-risk ETPs covering sectors like semiconductors, AI, and blue-chip stocks.

These ETPs aim to deliver three times (3x) the daily performance of BTC and ETH for long positions, or three times the inverse (-3x) for short positions, allowing investors to speculate on both upward and downward price movements without directly holding the cryptocurrencies.

The four products include: 3x Long Bitcoin ETP, -3x Short Bitcoin ETP, 3x Long Ether ETP and -3x Short Ether ETP. They will be available to European retail and institutional investors, subject to final regulatory nods, and are designed for short-term trading due to the compounding effects of daily leverage, which can amplify both gains and losses.

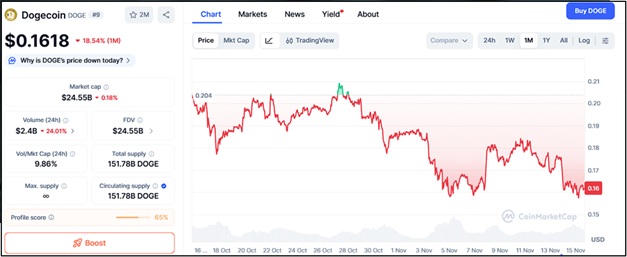

The timing of this launch is striking, coinciding with intense market volatility and a record retail exodus from spot crypto ETFs. In November 2025 alone, investors have pulled approximately $4 billion from U.S. spot Bitcoin and Ether ETFs—surpassing February’s previous record outflows—driven by broader economic pressures and waning enthusiasm for high-risk assets.

Crypto prices have tumbled sharply: Bitcoin has dropped ~35% from its early-October all-time high above $126,000, recently testing support below $80,000. Ether has fallen over 43% in the same period, exacerbating losses in the altcoin sector.

In contrast, traditional equity ETFs have seen inflows of ~$96 billion this month, including into leveraged stock products, highlighting a flight to perceived safer assets like the S&P 500 down just 5% from its October peak.

Analysts note that while this selloff creates a “buy low” opportunity for contrarians, the introduction of 3x leveraged tools could heighten speculation during an already turbulent phase.

Europe’s regulatory environment has been more crypto-friendly than the U.S. in recent years, enabling innovations like these ETPs ahead of potential SEC approvals for similar U.S. products (e.g., Defiance’s proposed 3x funds targeting crypto-related stocks).

However, experts emphasize the high risks: Leveraged ETPs are not suitable for buy-and-hold strategies, as daily resets can lead to significant decay in volatile markets. LeverageShares has stressed the need for investor education and risk safeguards.

Early reactions on X (formerly Twitter) are buzzing, with posts highlighting the “breaking” nature of the news and its potential to draw speculative interest despite the downturn.

This development underscores the crypto market’s resilience in product innovation, even as prices reel—potentially signaling a pivot toward sophisticated hedging tools for European traders.

Leveraged ETFs like the new 3x Bitcoin and 3x Ether ETPs from LeverageShares are powerful but extremely dangerous tools for most investors. They are designed to deliver a multiple (2x, 3x, etc.) of the daily performance of an underlying asset, not the long-term performance.

This daily reset creates several unique and often misunderstood risks. Because leveraged ETFs reset every single day, their long-term returns can deviate dramatically from the simple multiple of the underlying asset—especially in volatile markets.

Example with numbers 3x Bitcoin ETF, suppose Bitcoin does this over three days: Day 1: +10% ? 3x ETF = +30%. Day 2: –9.09% back to original price ? 3x ETF = –27.27%. Day 3: +10% again Bitcoin now flat over 3 days. Bitcoin ends exactly where it started 0% return, but the 3x ETF is down ~13%:

(1 + 0.30) × (1 – 0.2727) × (1 + 0.30) – 1 = –13%. The more volatile the asset and the longer you hold, the worse this decay becomes. Crypto is already one of the most volatile asset classes—3x leverage on it is decay on steroids.2. Losses are magnified much faster than gains.

A 33.4% drop in Bitcoin wipes out a 3x long ETF completely 3 × –33.4% = –100%. A 50% drop in Bitcoin turns a –3x short ETF into a total loss.3. Not suitable for holding longer than one day. The issuers (ProShares, Direxion, LeverageShares, etc.) explicitly state these products are for daily use only.

Most retail investors ignore this and treat them like normal ETFs, leading to catastrophic losses over weeks or months.4. Higher expense ratios and tracking costsLeveraged ETFs use swaps, futures, or daily borrowing, which is expensive.

Typical fees are 0.95%–1.5% per year—far higher than normal ETFs—eating returns even in flat markets.5. Forced liquidations in extreme movesSome leveraged products have termination events. If the underlying moves too much in one day (e.g., Bitcoin drops 25–30% in hours), the ETF can hit its leverage limit and be forced to liquidate, locking in permanent losses for holders.

Psychological and behavioral riskThe huge daily swings encourage emotional trading, over-trading, and revenge trading—exactly the opposite of what wins in investing. Real-world historical examples XXBT a former 2x Bitcoin ETP in Europe: lost >99% of its value from 2021 to 2023 despite Bitcoin only being down ~30% from its peak at the worst point.

UVXY 2x VIX futures is down >99.999% since inception in 2011, even though the VIX itself still exists. Bottom line – Who should use them? Almost nobody who is a normal retail investor. They can be useful for professional day traders hedging a specific short-term view.

Very sophisticated investors who actively monitor and rebalance daily. For 99% of people, 3x leveraged crypto ETPs are financial landmines with a shiny “get rich quick” wrapper. If you wouldn’t be comfortable losing your entire position in a single week or day, stay far away.