Financial inclusion is a key indicator of economic development and social welfare. It means that people have access to basic financial services, such as savings, payments, credit and insurance, that enable them to participate in the formal economy and improve their lives.

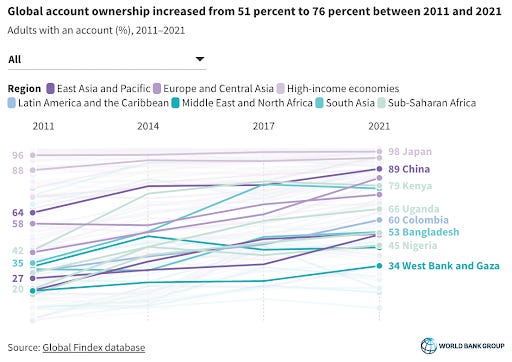

However, according to the latest data from the World Bank, there are still 1.7 billion adults in the world who do not have a bank account or a mobile money provider. This represents 24% of the global population, a significant decrease from 31% in 2014, but still far from the universal access envisioned by the Sustainable Development Goals.

Why does financial inclusion matter? Because it empowers people to make informed choices about their money, to save for emergencies and opportunities, to invest in their education and health, to start and grow businesses, to support their families and communities, and to contribute to the overall economic growth and stability of their countries.

Financial inclusion also reduces poverty and inequality, as it enables the most vulnerable and marginalized groups, such as women, rural dwellers, refugees and migrants, to access formal financial services that are affordable, convenient and secure.

The Sustainable Development Goals (SDGs) are a set of 17 global goals adopted by the United Nations in 2015, as part of the 2030 Agenda for Sustainable Development. They cover various aspects of human and planetary well-being, such as poverty, hunger, health, education, gender equality, clean energy, climate action and peace. One of the targets under the SDG 1 (No Poverty) is to ensure that all men and women have equal access to basic financial services by 2030.

Why does financial inclusion matter? Because it empowers people to make informed choices about their money, to save for emergencies and opportunities, to invest in their education and health, to start and grow businesses, to support their families and communities, and to contribute to the overall economic growth and stability of their countries.

Financial inclusion also reduces poverty and inequality, as it enables the most vulnerable and marginalized groups, such as women, rural dwellers, refugees and migrants, to access formal financial services that are affordable, convenient and secure.

How can we achieve financial inclusion for all? There is no single solution, but rather a combination of factors that need to work together. These include:

- Developing an enabling regulatory environment that fosters innovation and competition, while protecting consumers and ensuring financial integrity.

-

Leveraging digital technologies, such as mobile phones, biometrics and blockchain, that can lower the cost and increase the reach of financial services, especially in remote and underserved areas.

-

Building inclusive financial infrastructure, such as payment systems, credit bureaus and identification systems, that can facilitate interoperability and data sharing among different providers and platforms.

-

Enhancing financial literacy and capability, through education and awareness campaigns, that can help people understand and use financial services effectively and responsibly.

-

Promoting financial inclusion as a cross-cutting issue, that requires coordination and collaboration among various stakeholders, such as governments, regulators, private sector, civil society, donors and international organizations.

Financial inclusion is not an end in itself, but a means to an end. It is a tool that can help people achieve their potential and aspirations. It is a right that should be accessible to everyone. It is a challenge that we can overcome together.

Why is financial inclusion important? Because it can help people improve their lives and achieve their goals. For example, financial inclusion can help people:

- Manage their cash flow and cope with unexpected shocks, such as illness, natural disasters, or loss of income.

-

Build assets and invest in education, health, housing, or business opportunities.

-

Reduce their vulnerability and increase their resilience to poverty and inequality.

-

Participate in the formal economy and benefit from the opportunities it offers.

Financial inclusion is not only good for individuals, but also for societies and economies. Financial inclusion can:

- Support economic growth and development by mobilizing savings, allocating resources efficiently, and facilitating innovation and entrepreneurship.

-

Promote social cohesion and stability by reducing inequality, empowering women and marginalized groups, and enhancing trust and cooperation among people.

-

Strengthen financial systems and institutions by increasing their outreach, diversification, competition, and sustainability.

However, financial inclusion is not a magic bullet that can solve all the problems of the world. Financial inclusion is not an end in itself, but a means to an end. It is a tool that can enable people to achieve their potential and aspirations. But it is not enough by itself. Financial inclusion needs to be complemented by other policies and interventions that address the root causes of poverty, exclusion, and vulnerability.

Therefore, financial inclusion should not be seen as a standalone goal, but as part of a broader agenda of inclusive development. Financial inclusion should be aligned with the Sustainable Development Goals (SDGs), which are a set of 17 global goals that aim to end poverty, protect the planet, and ensure peace and prosperity for all by 2030. Financial inclusion can contribute to many of the SDGs, such as:

- SDG 1: No Poverty

-

SDG 2: Zero Hunger

-

SDG 3: Good Health and Well-being

-

SDG 4: Quality Education

-

SDG 5: Gender Equality

-

SDG 8: Decent Work and Economic Growth

-

SDG 10: Reduced Inequalities

-

SDG 13: Climate Action

To achieve financial inclusion for all, we need to work together as a global community. We need to involve all stakeholders, such as governments, regulators, financial service providers, civil society organizations, donors, academia, media, and most importantly, the people themselves. We need to foster a culture of innovation, collaboration, learning, and adaptation. We need to leverage the power of technology, data, and digital platforms.