It is a very tough call when $billions can just disappear in minutes. But I hate bailouts because only the rich are made whole whenever they do them. Sure, you can argue that it is only when we take care of the rich people that the ordinary citizens will have a chance. Good luck with your trickle down economics; I do not buy it.

In Nigeria, I have argued that we privatize profits but socialize losses when men borrow mindlessly and enjoy lives, only for AMCON, a government entity, to bail them out when they run into troubles. In America, I also posit the same thesis: bailing out millionaires when poor kids with $10,000 student loans cannot get help makes no sense.

Student-loan repayments are likely to restart this summer, and that will mean additional financial pressures for millions of younger Americans who are already in a hole. In the fourth quarter of 2022, Americans 30 and younger fell behind on credit-card payments at a rate similar to that during the end of the 2009 financial crisis, The Wall Street Journal reports. The majority of borrowers haven’t made student-loan payments since the beginning of the pandemic, and with it about to start up again, approximately 40 million people are on the hook for $1.6 trillion, WSJ reports. (LinkedIn News)

Those millionaires privatized their gains and profits as they invested, and when bad things happen, expecting the government to come to save them seems unfair, and out of sync with the spirit of capitalism. For SVB, any help should go to depositors; full access to funds, insured or otherwise. The Wall Street investors should chill. But if the government has to do it and bailout Wall Street, it must first push legislation that makes Joe Biden’s student loan forgiveness possible, making the current litigation at the Supreme Court irrelevant.

Silicon Valley Bank is no more. The FDIC seized the assets of the bank, a fixture of the VC world and a prolific lender to the tech and life sciences sectors, on Friday, marking the largest bank failure since the height of the 2008 financial crisis.

Silicon Valley’s clubby world of venture capital investors and entrepreneurs plunged into panic on Thursday amid fast-spreading reports of financial trouble at one of the startup industry’s most important banks.

SVB announced a day earlier that it was selling off securities and seeking to raise billions in a public share sale to cover steep losses on its balance sheet. Shares of Silicon Valley Bank crashed by roughly 60% in regular trading on Thursday, while the bank’s tech clients scrambled to figure out whether to withdraw their deposits, sparking concerns of an old-fashioned bank run. (Fortune newsletter)

Good one that Secretary of Treasury thinks that no bailout will happen.

“Let me be clear that during the financial crisis, there were investors and owners of systemic large banks that were bailed out, and the reforms that have been put in place mean that we are not going to do that again. But we are concerned about depositors and are focused on trying to meet their needs”.

Protect depositors and make them whole but do not save Wall Street investors. This bank possibly failed because of the panic created by the CEO’s statements and that is the risk therein.

Perspectives from Bill Ackman on Twitter

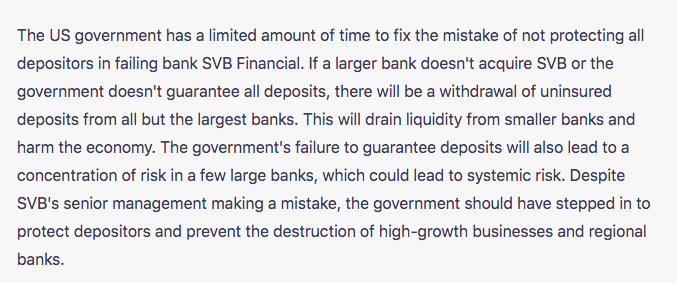

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank. Absent @jpmorgan @citi or…

— Bill Ackman (@BillAckman) March 11, 2023

Reproduced below for clarity: “The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank. Absent @jpmorgan @citi or @BankofAmerica acquiring SVB before the open on Monday, a prospect I believe to be unlikely, or the gov’t guaranteeing all of SVB’s deposits, the giant sucking sound you will hear will be the withdrawal of substantially all uninsured deposits from all but the ‘systemically important banks’ (SIBs).

These funds will be transferred to the SIBs, US Treasury (UST) money market funds and short-term UST. There is already pressure to transfer cash to short-term UST and UST money market accounts due to the substantially higher yields available on risk-free UST vs. bank deposits. These withdrawals will drain liquidity from community, regional and other banks and begin the destruction of these important institutions.

The increased demand for short-term UST will drive short rates lower complicating the @federalreserve’s efforts to raise rates to slow the economy. Already thousands of the fastest growing, most innovative venture-backed companies in the U.S. will begin to fail to make payroll next week. Had the gov’t stepped in on Friday to guarantee SVB’s deposits (in exchange for penny warrants which would have wiped out the substantial majority of its equity value) this could have been avoided and SVB’s 40-year franchise value could have been preserved and transferred to a new owner in exchange for an equity injection. We would have been open to participating. This approach would have minimized the risk of any gov’t losses, and created the potential for substantial profits from the rescue.

Instead, I think it is now unlikely any buyer will emerge to acquire the failed bank. The gov’t’s approach has guaranteed that more risk will be concentrated in the SIBs at the expense of other banks, which itself creates more systemic risk. For those who make the case that depositors be damned as it would create moral hazard to save them, consider the feasibility of a world where each depositor must do their own credit assessment of the bank they choose to bank with. I am a pretty sophisticated financial analyst and I find most banks to be a black box despite the 1,000s of pages of @SECGov filings available on each bank. SVB’s senior management made a basic mistake. They invested short-term deposits in longer-term, fixed-rate assets. Thereafter short-term rates went up and a bank run ensued. Senior management screwed up and they should lose their jobs.

The @FDICgov and OCC also screwed up. It is their job to monitor our banking system for risk and SVB should have been high on their watch list with more than $200B of assets and $170B of deposits from business borrowers in effectively the same industry. The FDIC’s and OCC’s failure to do their jobs should not be allowed to cause the destruction of 1,000s of our nation’s highest potential and highest growth businesses (and the resulting losses of 10s of 1,000s of jobs for some of our most talented younger generation) while also permanently impairing our community and regional banks’ access to low-cost deposits.

This administration is particularly opposed to concentrations of power. Ironically, its approach to SVB’s failure guarantees duopolistic banking risk concentration in a handful of SIBs. My back-of-the envelope review of SVB’s balance sheet suggests that even in a liquidation, depositors should eventually get back about 98% of their deposits, but eventually is too long when you have payroll to meet next week. So even without assigning any franchise value to SVB, the cost of a gov’t guarantee of SVB deposits would be minimal. On the other hand, the unintended consequences of the gov’t’s failure to guarantee SVB deposits are vast and profound and need to be considered and addressed before Monday. Otherwise, watch out below.”

This is the ChatGPT summary of this tweet:

Y Combinator Begins a Petition for “backstop of depositors”

To the Honorable Secretary Janet Yellen, Chairman Martin J. Gruenberg, Chairman Brown, and Chairman McHenry:

We, the undersigned, are deeply concerned about the rapid failure of Silicon Valley Bank, a leading financial institution that has played a vital role in supporting the technology industry in the United States. We are not asking for a bailout for the bank equity holders or its management; we are asking you to save innovation in the American economy.

We ask for relief and attention to an immediate critical impact on small businesses, startups, and their employees who are depositors at the bank. According to the NVCA, Silicon Valley Bank has over 37,000 small businesses with more than $250,000 in deposits. These balances are now unavailable to them, and without further intervention, according to the FDIC website, may be inaccessible for months to years.

In the Y Combinator community, one-third of startups with exposure to SVB used SVB as their sole bank account. As a result, they will fail to have the cash to run payroll in the next 30 days. By that measure, we can estimate that payroll-related furlough or shutdown will impact more than 10,000 small businesses and startups. If the average small business or startup employs 10 workers, this will have an immediate effect of furlough, layoff, or shutdown, affecting over 100,000 jobs in the most vibrant sector of innovation in our economy.

Silicon Valley Bank’s failure has a real risk of systemic contagion. Its collapse has already instilled fear among founders and management teams to look for safer havens for their remaining cash, which can trigger a bank run on every other smaller bank.

If we allow this to happen, it will immediately impact the US technology industry and US competitiveness worldwide and ultimately set back US competitiveness by a decade or more, while the rest of the world races forward.

We have a simple ask:

– Small business depositors at Silicon Valley Bank should be made whole. Regulators need to conduct a backstop of depositors. We are not asking for a bank bailout.

– Longer term, Congress should work to restore stronger regulatory oversight and capital requirements for regional banks, and any malfeasance or mismanagement on the part of SVB executives leading to this failure should be investigated.

This requires swift and decisive action in order to prevent further shockwaves through the economy that could lead to financial crisis and layoffs of more than 100,000 workers. We must protect US competitiveness in the world.

Thank you for your attention to this important matter.

Sincerely,

Garry Tan, CEO & President Y Combinator

US Government Will Protest All Deposits

WASHINGTON, DC — The following statement was released by Secretary of the Treasury Janet L. Yellen, Federal Reserve Board Chair Jerome H. Powell, and FDIC Chairman Martin J. Gruenberg:

Today we are taking decisive actions to protect the U.S. economy by strengthening public confidence in our banking system. This step will ensure that the U.S. banking system continues to perform its vital roles of protecting deposits and providing access to credit to households and businesses in a manner that promotes strong and sustainable economic growth.

After receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Yellen approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.

We are also announcing a similar systemic risk exception for Signature Bank, New York, New York, which was closed today by its state chartering authority. All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer.

Shareholders and certain unsecured debtholders will not be protected. Senior management has also been removed. Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

Finally, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.

The U.S. banking system remains resilient and on a solid foundation, in large part due to reforms that were made after the financial crisis that ensured better safeguards for the banking industry. Those reforms combined with today’s actions demonstrate our commitment to take the necessary steps to ensure that depositors’ savings remain safe.

Comment on Feed

Comment 1: Prof. your submission is so apt. I remember writing a post some years ago for AMCON to be shutdown completely. I was forced to delete post. I see no reason why a reckless capitalist take gains and profits in private but put their losses into the hands of the society due to their unreasonable and high risk appetite all in the name of bailout.

Comment 2: Hmm. Like you said Sir, it is indeed a very tough call. And I agree with you as many of these elites borrow and spend recklessly only to run into problems and cry out for bail outs.

With that said I believe there should be a balance which would mean creating standards to qualify for bail outs should the unthinkable happen.

Comment 3: I think this is a good decision from the regulators. It will send a warning to others. You can’t get greedy, taking risks with reckless abandon. And except when things go wrong government will bail out.

Comment 4: Honestly, if the government bails out SVB without forgiving my $10,000 in student loan first, I would carry a placard. The 1 percent of the population of every country can no longer hedge their greatest risks which is total annihilation on the backs of the middle class while enjoying their gains by themselves. If SVB lost $2.2 Billion dollars, why was Billiornaire depositors allowed to withdraw their funds. Whose $2.2 Billion was lost?

My Response: SVB was worth and traded well above $10 billion in NASDAQ before it went under. Those men are the ones tweeting for bailout!

Comment 5: But Prof, these firms serve public good despite the privatalisation of their gains or profits. Bailing them out protect a social course and advance societal growth.

In times of crisis, focusing on the general good should be of importance. You can bail out the company and let the culprits face the full rigors of the law.

My Response: “But Prof, these firms serve public good despite the privatalisation of their gains or profits. Bailing them out protect a social course and advance societal growth.” – As I wrote, I do not believe in trickle down economics.

On the law, there is no law possibly broken. When banks fail due to bank runs, nothing illegal /criminal needs to happen.

I will be fine with a bailout provided the $10k student loans bailout will go through for students. That is also public good.

Comment 6: I think it is all about perspective, I’ve always been a supporter of bailouts because there is a socialist angle to it. Just imagine the number of people that might lose their jobs and number of dependents that might be hit as a result of SVB crisis, if government decides to look away. Imagine the value of individual income tax that government will lose, and so many more. Of course, those who dropped the ball (Directors and Significant Shareholders) can be punished in another way, but firstly, we must save the employees and their families.

My Response: I am in 100% provided they approve the $10k student loans. If you graduate without student loans, you have choices. But if you have piles of loans, you cannot have freedom in many ways. The argument that bailing out Wall Street is great when trial lawyers are telling the government not to help students is what I do not buy. (I have no student loans, I went through Fellowships in Johns Hopkins)

Comment 7: Very well said Professor, you may not agree with me but bail out is necessary in my opinion and the reason is simple. Without the bail out, the billionaires and millionaires will lose money but they’ll still be fine at the end of the day. What about the middle class who’ll lose their lively hood? We are looking at the 150k jobs going down the drain. The US already lost the manufacturing war, it can afford to lose tech.