U.S. spot XRP exchange-traded funds (ETFs) recorded a robust net inflow of $67.74 million, elevating their cumulative net assets under management (AUM) to $844.99 million.

This marks the 12th consecutive day of positive inflows since the funds launched on November 13, 2025, positioning XRP ETFs as the fastest-growing major crypto asset vehicle in the market.

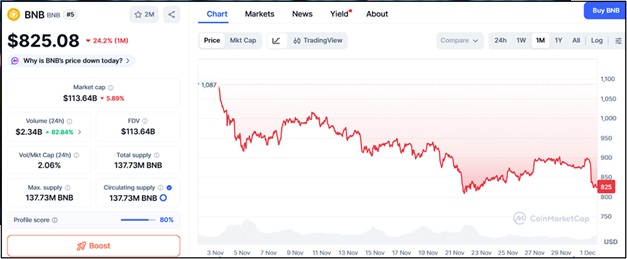

The milestone underscores accelerating institutional adoption of XRP, the native token of the Ripple network, even as it trades around $2.19—up nearly 10% in the past 24 hours.

The $67.74 million influx reflects sustained buying pressure from ETF clients, including major players like Vanguard, which recently listed XRP ETFs on its platform for broader access.

This builds on prior days’ momentum, with total inflows now approaching the $1 billion threshold. At least five spot XRP ETFs are active, including offerings from Grayscale (GXRP), Franklin Templeton (XRPZ), Bitwise, Canary Capital, and others.

Early launches saw strong debuts—e.g., Grayscale’s fund pulled in $67.36 million on day one, while Franklin Templeton’s attracted $62.59 million. Real-time trackers show over 339 million XRP tokens locked across these funds, equivalent to roughly 0.3% of the total circulating supply.

XRP’s price surge aligns with broader crypto optimism, including Bitcoin topping $92,000 and Ethereum at $3,073. However, on-chain data indicates 29% of XRP has left exchanges recently, signaling reduced selling pressure and potential for further upside.

Analysts note a bullish RSI divergence, hinting at a trend reversal despite prior volatility. This inflow streak highlights XRP’s maturation as a regulated investment option, outpacing many peers in growth rate. With ETFs now absorbing significant volumes like models suggest daily buys of 74.5 million XRP could drive prices to $600 under certain elasticity assumptions, it could catalyze a new bull cycle for the altcoin.

As the creator of XRP—the native cryptocurrency of the XRP Ledger (XRPL)—Ripple has been instrumental in shaping the regulatory, infrastructural, and market conditions that enabled these ETFs to launch in November 2025.

While Ripple does not directly issue or manage the ETFs which are handled by third-party asset managers like Grayscale, Franklin Templeton, and Bitwise, its efforts in legal advocacy, technological development, and ecosystem building have been pivotal in unlocking institutional access to XRP.

Ripple’s four-year legal battle with the U.S. Securities and Exchange Commission (SEC)—initiated in 2020 over allegations of unregistered securities sales—served as a critical proving ground for XRP’s non-security status. A landmark July 2023 court ruling affirmed that XRP sold on public exchanges is not a security, while institutional sales were deemed violations.

The SEC appealed but withdrew its challenge in March 2025, culminating in an August 2025 settlement that fully resolved the overhang. This clarity was the green light for spot ETF filings, as it aligned XRP with the regulatory framework that approved Bitcoin and Ethereum ETFs in 2024.

Without this resolution, issuers like Canary Capital and Bitwise could not have pursued “auto-effective S-1” filings under the SEC’s streamlined 2025 process. Ripple CEO Brad Garlinghouse has publicly hailed the outcome as a “win for the entire crypto industry,” emphasizing how it positions XRP as a utility token for payments rather than an investment contract.

The ledger’s consensus protocol enables near-instant transactions (3-5 seconds) at low costs, making it ideal for the high-volume creations and redemptions in ETF operations—where authorized participants exchange baskets of XRP for fund shares.

Ripple’s On-Demand Liquidity (ODL) solution, which uses XRP as a bridge asset for cross-border payments, further underscores its real-world utility, attracting banks and institutions that now view XRP ETFs as a regulated entry point.

Ripple’s recent innovations, like the XRPL lending protocol and integration with ISO 20022 standards, enhance this appeal. For instance, Abu Dhabi’s approval of Ripple’s RLUSD stablecoin for institutional use ties directly into ETF liquidity pools.

Garlinghouse has stressed XRP’s role as a “temporary settlement layer” in global finance, a narrative amplified on X where analysts link it to ETF-driven volume surges. Funds like Grayscale’s GXRP explicitly reference the “peer-to-peer Ripple Network” in their prospectuses, crediting it for XRP’s 13-year track record of reliability.

Ripple’s $500 million funding round in November 2025 at a $40 billion valuation—from firms like Citadel Securities—signals strong backing for scaling XRP’s role in tokenized assets and remittances, projected to capture 14% of SWIFT’s volumes.

While Ripple holds a significant portion of XRP about 40 billion in escrow, it does not directly sell to ETFs, avoiding past SEC scrutiny. Instead, it supports market makers and liquidity providers.

Ripple’s presence at events like Swell 2025, alongside White House officials, has sparked ETF buzz, with posts highlighting how these ties could drive $8 billion in inflows.

ETFs as a Ripple-Led Bull CatalystSince the November 13, 2025, launch of the first spot XRP ETF Canary’s XRPC, with $58 million in debut volume, Ripple’s ecosystem has seen explosive growth.

Total ETF AUM hit $844.99 million by December 3, outpacing early Bitcoin ETF inflows in relative terms. Analysts forecast a 65% XRP price rally to $3.60+ by year-end, driven by ETF demand reducing exchange supply 29% of XRP off exchanges recently.

Ripple’s positioning of XRP for $30 trillion in tokenized assets amplifies this, with ETFs funneling retail and institutional capital into its payments infrastructure. However, risks persist: XRP’s price remains volatile down 40% from its $3.65 July ATH, and competition from stablecoins like USDT challenges its dominance.

Ripple’s escrow releases 1 billion XRP monthly could pressure supply if not managed tightly. Ripple envisions XRP ETFs as a “regulated gateway” to its broader mission of modernizing $120 trillion in annual cross-border flows.

With more filings pending (e.g., 21Shares’ TOXR launching December 2), and futures ETFs like ProShares’ UXRP paving the way, Ripple’s role could evolve into deeper integrations, such as ETF-linked ODL pilots.

As Garlinghouse noted, “XRP connects the digital financial system”—a connectivity now supercharged by Wall Street. For investors, this convergence offers exposure to utility-driven growth, but always DYOR amid crypto’s inherent risks.