Crypto market momentum is shifting rapidly toward early-stage AI projects as traders and analysts focus on where the next major parabolic wave will originate. Among all emerging tokens, Ozak AI has become the standout name—repeatedly appearing in analyst forecasts as one of the few projects capable of delivering life-changing multipliers in the 2025–26 cycle.

With its AI-native architecture, early-phase valuation, and accelerating demand from the Ozak AI Presale, investors are running scenarios that show how even modest entries could grow into extremely large returns. According to these projections, a strategic flip of just $1,500 into Ozak AI today could potentially transform into a six-figure portfolio if the project hits the 50x–100x range many analysts believe is realistic based on its fundamentals and early traction.

Why Ozak AI Is Being Viewed as a High-Probability 100x Project

The first reason Ozak AI is drawing massive attention is the strength of its utility. Unlike many early-stage tokens that launch without clear technology or product direction, Ozak AI begins with a complete AI-native infrastructure blueprint.

Its ecosystem features millisecond-speed prediction engines capable of reading market conditions instantly, cross-chain analytics modules that interpret multiple blockchain environments at once, and ultra-fast signal flows delivered through its partnership with HIVE that return insights in just 30 milliseconds. On top of this, Ozak AI integrates with SINT’s autonomous AI agent technology, enabling real-time on-chain execution, workflow automation, voice-responsive commands, and intelligence-driven decision-making.

This places Ozak AI at the center of the next major Web3 transformation: AI automation. Analysts repeatedly emphasize that the projects merging artificial intelligence with blockchain infrastructure stand to outpace traditional altcoins over the next several years—and Ozak AI enters the market from the perfect position: early, affordable, and technologically advanced.

How a $1,500 Allocation Could Grow to Six Figures

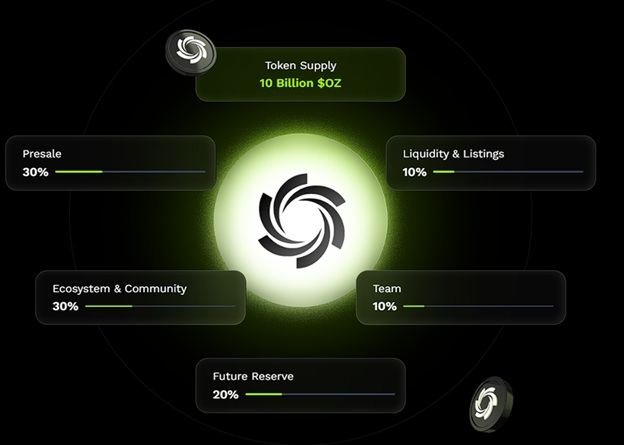

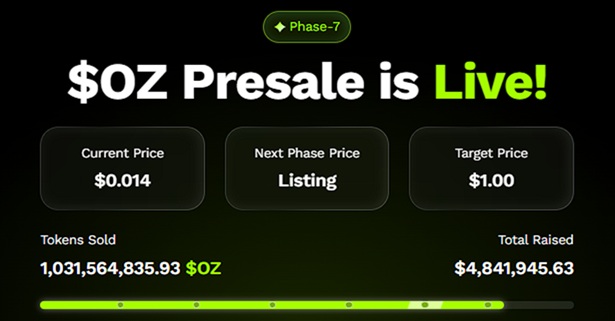

Because Ozak AI is still in the OZ presale phase and priced at an early-stage market cap, even small investments have significant upside potential. With over $4.8 million raised and more than a million tokens sold through the Ozak AI Presale, the project shows the same early adoption curve that characterized previous cycle winners that later surged 50x–100x.

- At a 50x multiple, a $1,500 allocation becomes $75,000.

- At a 100x multiple, the same allocation becomes $150,000.

These projections aren’t based on speculation alone—they’re grounded in Ozak AI’s strong partnerships with Perceptron Network’s 700K node ecosystem, HIVE’s ultra-fast signal infrastructure, and SINT’s autonomous AI agent layer. This gives Ozak AI real-world functionality that can scale immediately upon launch, making its long-term value potential far more tangible than hype-driven meme coins or single-utility projects.

Why Smaller Investments Can Outperform Large Caps

The reason analysts highlight Ozak AI over major assets like Bitcoin, Solana, or Ethereum is rooted in market structure. Large-cap tokens grow steadily, but they rarely produce 50x–100x moves due to their valuations. Early-stage AI tokens, however, sit at small market caps where exponential expansion is possible—especially when backed by real utility and early network effects. Ozak AI fits precisely into this category, which is why traders are labeling it a generational opportunity.

The Next Big Wealth-Building Window May Be Opening Now

With AI-driven projects expected to dominate the 2025–26 cycle, Ozak AI is emerging as the strongest candidate for explosive returns. Its early-stage pricing, real AI infrastructure, rapid adoption curve, and powerful partnerships all point toward long-term scalability—making it a prime contender for six-figure wealth creation from even modest initial contributions.

A $1,500 allocation won’t change anything overnight—but with Ozak AI’s current trajectory, it could be the smartest early move for building a six-figure portfolio by 2026.

About Ozak AI

Ozak AI is a blockchain-based crypto project that provides a technology platform that specializes in predictive AI and advanced data analytics for financial markets. Through machine learning algorithms and decentralized network technologies, Ozak AI enables real-time, accurate, and actionable insights to help crypto enthusiasts and businesses make the correct decisions.

For more, visit:

Website: https://ozak.ai/

Telegram: https://t.me/OzakAGI

Twitter: https://x.com/ozakagi