A recent on-chain transaction has reignited discussions about one of the cryptocurrency industry’s most legendary investors. According to blockchain analytics platform Lookonchain, a wallet believed to be associated with venture capitalist Tim Draper transferred 1,000 Bitcoin valued at approximately $61.82 million, to Coinbase Prime.

While the purpose of the transfer remains unknown, the movement has attracted widespread attention because of Draper’s historic Bitcoin holdings and his long-standing reputation as one of the earliest institutional supporters of digital assets.

Large Bitcoin transfers to exchanges often spark speculation about whether an investor intends to sell, rebalance a portfolio, or simply move assets into institutional custody.

Coinbase Prime is widely used by institutional investors for secure storage, trading, and asset management, meaning the transaction does not necessarily indicate an imminent sale.

The size of the transfer has prompted market participants to closely monitor future wallet activity. Tim Draper’s Bitcoin story dates back to 2014, when he participated in a U.S. Marshals auction of Bitcoin seized from the Silk Road marketplace. Draper purchased approximately 29,656 BTC at an average price of around $632 per coin.

At the time, many viewed Bitcoin as a highly speculative experiment with uncertain long-term prospects. However, Draper remained confident in the technology’s future and consistently predicted that Bitcoin would become a globally recognized store of value.

That investment has since become one of the most successful trades in cryptocurrency history. The original purchase, worth less than $20 million at the time, appreciated dramatically during Bitcoin’s rise over the following decade.

At its peak valuation, Draper’s holdings were estimated to be worth approximately $3.74 billion. Even after market fluctuations, the same Bitcoin stash is still valued at roughly $1.82 billion, demonstrating the extraordinary returns generated by long-term conviction in digital assets.

Draper’s investment philosophy has consistently emphasized patience over short-term trading. Rather than reacting to daily market volatility, he has repeatedly argued that Bitcoin represents a technological revolution capable of reshaping finance, payments, and global commerce.

His unwavering optimism has made him one of the cryptocurrency industry’s most recognizable advocates, inspiring both retail and institutional investors to adopt a long-term perspective.

The latest wallet movement also highlights the growing importance of blockchain transparency. Unlike traditional financial systems, public blockchains allow analysts to monitor large transfers in real time, even though wallet ownership cannot always be confirmed with certainty.

Firms specializing in on-chain analytics can identify transaction patterns that provide valuable insights into market behavior without revealing the personal identities behind the addresses. Although the transfer has generated considerable interest, investors should avoid drawing premature conclusions.

Large wallet movements occur for many reasons, including custody upgrades, portfolio diversification, collateral management, or preparations for over-the-counter transactions. Until additional evidence emerges, any assumptions about Draper’s intentions remain speculative.

The reported transfer serves as a reminder of Bitcoin’s remarkable journey over the past decade. From being acquired for just hundreds of dollars per coin during a government auction to becoming an asset worth tens of billions across the broader market, Bitcoin has transformed global finance.

Whether this latest transaction represents portfolio management or something more significant, it once again places the spotlight on one of crypto’s most successful early believers and the extraordinary value created through long-term investment conviction.

The logo for Goldman Sachs is seen on the trading floor at the New York Stock Exchange (NYSE) in New York City, New York, U.S., November 17, 2021. REUTERS/Andrew Kelly/Files

Goldman Sachs has strengthened its position as the leading mergers and acquisitions adviser in Europe, the Middle East, and Africa during the first half of 2026, capturing its largest share of the market in nearly a decade as regional dealmaking reached its highest level in 19 years, according to LSEG data.

Dealmaking in the region totaled $676 billion during the January to June period, more than double 2025 levels, reflecting a backdrop of looser regulatory constraints and renewed corporate confidence. Goldman advised on 111 deals, representing 44% of the EMEA M&A total by value in the first six months of 2026, up from 42% in the same period a year earlier. The bank’s share was its highest for the January-June period since 2018, when it reached 46%.

The investment bank, which is also the global leader in M&A advisory, has long dominated the EMEA sector. In the first half of this year, its closest rival, JPMorgan, managed to slightly narrow the gap but still trailed with 35% market share after advising on 99 announced deals. That compared with Goldman’s 11 percentage point lead over JPMorgan in the first half of 2025. Globally, Goldman maintained a commanding 38% market share and advised on the biggest number of deals of any firm.

“Companies are taking a long-term strategic view and investing for where they want to be in the coming decades, not just the next few quarters,” said Carsten Woehrn, co-head of M&A in EMEA at Goldman Sachs.

Goldman’s dominance was particularly evident in the largest transactions. The bank advised on 15 of the 20 biggest deals in the region, including working alongside Morgan Stanley on Unilever’s approximately $45 billion sale of its food business to McCormick, the largest deal of the period, and on TK Elevators’ $34 billion combination with Kone. Its closest rival, JPMorgan, worked on 13 of the biggest deals and was not involved in the Unilever-McCormick transaction.

Goldman’s sustained leadership in EMEA M&A comes amid a broader transformation in the advisory landscape since the global financial crisis, when the field became narrower and more concentrated, according to Valeria Vitkova, associate professor of finance at Bayes Business School.

“The firm’s sustained leadership reflects more than simply a succession of favorable years. It appears to represent a sustained competitive advantage that has persisted throughout the post-crisis period,” said Vitkova, who added that in that period dealmaking has become more complex.

The surge in activity this year contrasts with last year’s slowdown, which was partly attributed to initial uncertainty surrounding U.S. President Donald Trump’s return to the White House. Despite ongoing market volatility, bankers report that companies are increasingly looking beyond short-term turbulence to pursue strategic opportunities.

Independent advisory boutique Rothschild advised on the highest number of deals at 163, but Goldman’s lead was built on its involvement in the largest transactions. This highlights the bank’s strength in handling complex, high-value mandates that require deep sector expertise and global reach.

The robust first-half performance suggests dealmakers are regaining confidence after a period of caution. Looser regulatory constraints in parts of the region have likely contributed to the pickup, allowing companies to pursue transactions that might have faced greater hurdles in previous years.

Analysts believe that Goldman maintaining its position at the top of the league tables bolsters its reputation as the go-to adviser for major strategic moves. The bank’s ability to secure mandates on some of the period’s most significant deals underscores its competitive edge in a market where relationships, expertise, and execution capabilities remain paramount.

However, the competitive landscape continues to evolve. Analysts note that JPMorgan’s ability to narrow the gap slightly indicates that rivals are also positioning themselves strongly. Other players, including boutique firms like Rothschild, continue to carve out significant roles, particularly in terms of deal volume.

Looking ahead, bankers caution that league tables could shift substantially in the second half if announced deals fail to close. Goldman, for instance, is advising Commerzbank, which has been seeking to fend off a $28 billion bid from UniCredit. The outcome of such high-profile situations could influence final rankings.

However, the strong first-half performance in EMEA M&A provides an encouraging signal for the global dealmaking environment.

Tesla delivered its strongest second-quarter vehicle sales on record, comfortably beating Wall Street expectations and strengthening hopes that the electric vehicle maker could finally end two consecutive years of annual delivery declines.

The results provide an important boost for the company as Chief Executive Elon Musk continues steering Tesla beyond its traditional automotive business toward artificial intelligence, autonomous driving and robotics, businesses that increasingly underpin the company’s roughly $1.6 trillion market valuation.

While the delivery figures exceeded expectations, investors remained cautious about Tesla’s long-term execution strategy. Shares fell about 7% in midday trading on Thursday after climbing roughly 12% earlier in the week, suggesting much of the positive news had already been priced into the stock.

Tesla delivered 480,126 vehicles during the April-June quarter, a record for a second quarter and about 25% higher than a year earlier. The figure far surpassed analysts’ consensus estimate of 402,776 vehicles compiled by Visible Alpha. The company produced 451,758 vehicles during the same period, meaning deliveries exceeded production by more than 28,000 units as Tesla reduced inventory accumulated during the first quarter.

The stronger-than-expected performance arrives at a pivotal time for the automaker. Since late 2024, Tesla has faced slowing demand, intensifying competition from Chinese manufacturers, reduced government incentives in the United States, and lingering reputational damage stemming from Musk’s political activities.

Analysts said the latest results suggest Tesla’s turnaround is gathering momentum, particularly outside its home market.

“I think the huge growth in Europe is the key driver for Tesla right now. U.S. sales still appear to be down, albeit less than the broader U.S. EV decline, while China is seeing small growth,” said Seth Goldstein, senior equity analyst at Morningstar.

Goldstein, who had previously forecast Tesla would report a third consecutive annual decline in deliveries, revised his outlook after the figures.

“I think it would be very hard to see a decline for the full year at this point,” he said.

Europe emerged as Tesla’s brightest region during the quarter, benefiting from a combination of higher fuel prices, expanded government incentives for electric vehicles, faster electrification of commercial fleets, and easing consumer resistance following last year’s backlash against Musk’s far-right political positions.

Tesla also continued to benefit from pricing adjustments introduced last year, including lower-cost versions of its Model 3 sedan and Model Y sport utility vehicle, alongside aggressive financing offers designed to stimulate demand.

“Their pricing and their products are helping the buyers overcome any issues they might have with Elon Musk personally,” said Sam Fiorani, vice president at AutoForecast Solutions.

Demand in the United States, however, remains considerably weaker.

The removal of federal tax credits for electric vehicles late last year continues to weigh on consumer purchases, even as Tesla attempts to stimulate sales through refreshed models and financing incentives.

“We’re cautiously optimistic for some growth this year,” Fiorani said.

Other analysts remain more guarded about Tesla’s prospects in its largest market.

“We believe Tesla’s U.S. sales likely declined by at least 10% in the quarter,” said Freedom Broker senior analyst Dmitriy Pozdnyakov.

But China has continued to provide another source of resilience.

Sales of Tesla’s China-produced vehicles have improved this year following the introduction of the refreshed Model Y, although competition from domestic manufacturers remains intense, particularly from BYD and other Chinese electric vehicle producers that continue expanding both product offerings and price competition.

Tesla is also seeking to stimulate demand in North America through new products. On Thursday, the company introduced the six-seat, longer-wheelbase version of the Model Y in the United States. The three-row SUV, known as the Model Y L, previously contributed to stronger sales in China, and analysts believe it could broaden Tesla’s appeal among larger American families.

The delivery results also strengthen Tesla’s financial position as it embarks on one of the most aggressive investment programs in the automotive industry’s history. The company expects capital expenditure to exceed $25 billion in 2026, nearly three times the $8.5 billion invested last year.

The spending will fund expansion across several strategic initiatives, including artificial intelligence infrastructure, battery manufacturing, production facilities for the Cybercab autonomous vehicle, and development of the Optimus humanoid robot. These businesses have increasingly become central to Tesla’s valuation, with many investors viewing the company less as a conventional automaker and more as an AI and robotics company.

Tesla has continued expanding the deployment of its Full Self-Driving (FSD) advanced driver-assistance software across Europe, although regulatory approvals mean the technology remains available in only a limited number of countries. Analysts expect wider European availability over the coming months, which could further support vehicle demand.

The company is simultaneously expanding its robotaxi ambitions after launching a limited commercial autonomous ride-hailing service in Austin, Texas, in June. Musk has repeatedly stated that Tesla intends to scale the robotaxi network rapidly throughout 2026, positioning autonomous mobility as a future pillar of the company’s business.

Production of the Cybercab, Tesla’s purpose-built autonomous vehicle that eliminates both pedals and a steering wheel, is expected to accelerate later this year.

Even with stronger vehicle deliveries, investors remain focused on whether Tesla can successfully execute its broader transformation beyond electric cars.

“The stock price is still riding a bit of a rollercoaster. Investors are hyped about the bounce-back, but the big money is still waiting to see if Tesla can actually deliver on Elon Musk’s promises around AI, robotaxis, and self-driving tech,” said David Wagner, head of equity at Tesla shareholder Aptus Capital Advisors.

The second-quarter delivery report therefore represents more than a rebound in vehicle sales as it offers evidence that Tesla’s core automotive business continues to generate the cash flow needed to finance its increasingly ambitious AI and autonomous driving strategy.

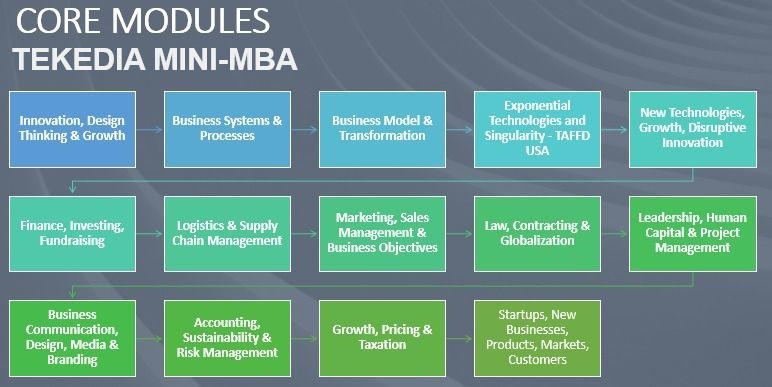

Invent, innovate and drive organizational transformation, performance, and growth. Capture emerging opportunities in changing markets while optimizing innovation and profitability. Digitally evolve your business or functional area, turning digital disruption into a competitive capability and advantage. Master the concepts of building category-king companies, and thrive.

Registration for another edition of Tekedia Mini-MBA opens. Tekedia Mini-MBA, from Tekedia Institute, is an innovation management 12-week program, optimized for business execution and growth, with digital operational overlay. It runs 100% online. The theme is Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies. All contents are self-paced, recorded and archived which means participants do not have to be at any scheduled time to consume contents. Our programs are designed for ALL sectors, from fintech to construction, healthcare to manufacturing, agriculture to real estate, etc.

More so, the sector- and firm-agnostic management program comprises videos, flash cases, challenge assignments, labs, written materials, webinars, etc and is delivered by a global faculty coordinated by Prof Ndubuisi Ekekwe. When we finish, we will issue a certificate from the Tekedia Institute, Boston USA.

Register and join us. You will emerge transformed with tools and capabilities that engineer confidence, performance and growth. Accelerate your leadership ascent with us! Here are our programs and costs.

Program Cost

Code

Description

Cost

MINI

Tekedia Mini-MBA. And WhatsApp School

US$170 or N120,000 naira

MINF

Annual Package: 3 consecutive MINI, and 2 optional capstones.

$340 or N180,000

MINR

(optional) Homework review; faculty will review your homework with feedback.

$30 or N10,000

CAPS

(optional) Tekedia capstone is a research paper, analogous to final college project.

Supply Chain Management, Global Partnership & Contracting – Adebayo Adeleke, ex-Chief of Contracting and Deputy Chief, Business Operations Division, US Army

Intellectual Property: Strategy, Management & Commercialization – Ifeanyi Okonkwo, University of Cape Town & Jackson, Etti & Edu

Business Relationship Management & Negotiation Skills - Charles Okeibunor, CEO IRMP

Due Diligence and Business Intelligence – Chike Obimma, Partner at NICCOM LLP (Commercial Law Firm)

Week 10: Leadership, Human Capital & Project Management

Leadership, Knowledge Management – Prof. Ayodeji Oyebola, Saint Mary’s University of Minnesota

Human Resources Management - Adora Ikwuemesi, Director Kendor Consulting

Leading and Managing Teams, Stakeholder Management with NICER Model – Dr. Chisom Ezeocha, Project Delivery Manager, Shell

Career Planning – Precious Ajoonu, Manager, Jobberman

Tax Treaties and Their Benefits - Emmanuel Eze, Manager, Federal Inland Revenue Service (FIRS)

Regional Case: Tax Law and Compliance in Lagos State - Abimbola Abdur-Rahman Lekki, Lagos Internal Revenue Service

Effective Product & Service Pricing, Accelerated Revenue, Profit Maximization - Saima Khan, Partner, Strategic Pricing Management Group, Toronto, Canada

Establishing Business Consulting & Advisory Services - Mustafa Yusuf-Adebola, Founder, Provisio Professional

Driving Profitable Growth, Marginal Cost, Scaling – Prof. Ndubuisi Ekekwe

Stimulating New Markets Through Innovation and Perception Demand – Prof Ndubuisi Ekekwe

Week 14: Startups, New Businesses, Products, Markets, Customers

The Mechanics of Minimum Viable Product and Product Development - Prof Ndubuisi Ekekwe

The NEP Framework – Discovering and Listening to Customers - - Prof Ndubuisi Ekekwe

Customer Validation and Building for What Customers Really Want. - - Prof Ndubuisi Ekekwe

Knowing and Defining Your Market - Prof Ndubuisi Ekekwe

Navigating Business Growth Phases - Prof Ndubuisi Ekekwe

ChatGPT, DALL-E 2 and Emerging AI Innovations: Business Opportunities in Africa - Zion Pibowei, Head of Data Science, Periculum Canada

How to Scale a Business/Startup - Jane Egerton-Idehen, Head of Sales Middle East & Africa at Meta (Facebook parent company)

Final Week: Execution and Closure

The Call to Business Execution, Closure – Prof Ndubuisi Ekekwe

Graduation Day – Prof Ndubuisi Ekekwe

Tekedia Live: Optional Zoom session which holds thrice per week (Tue, Thur, Sat at 7pm WAT). It is archived for those unable to make the session live. Our faculty members and invited guests rotate to anchor the sessions. Live provides a platform for members to ask questions and get live responses.

Welcome! Unleash your leadership potential, master business excellence, and embrace transformation with Tekedia Mini-MBA. Join us and experience a cutting-edge business management & leadership program: online, self-paced, and world-class. At Tekedia Institute, we co-learn with thousands of professionals and students, from many countries, on the mechanics of business, connecting innovation, growth and operational execution, across market territories and industrial sectors.

Our faculty members come from Microsoft, Google, Shell, Flutterwave, Nigerian Breweries, NNPC, Jobberman, Coca Cola, PwC, BUA Cement, and other great organizations. Besides pre-recorded courseware, thrice weekly, we hold live Zoom sessions (Tue, Thur and Sat at 7pm WAT) – Prof Ndubuisi Ekekwe, Tekedia Institute Lead Faculty.

Access to any Facyber Certificate program for free. Facyber offers online cybersecurity programs on policy, technology, management, and forensics.

Capstone Program

Here are the 12 tracks:

CLSM: Certificate in Logistics and Supply Chain Management

CBIS: Certificate in Business Innovation, Growth & Sustainability

CMAB: Certificate in Media, Advertising & Branding

CSBM: Certificate in Startup and Small Business Management

CIBA: Certificate in Business Administration

CPFM: Certificate in Personal Finance & Wealth Management

CMSM: Certificate in Marketing and Sales Management

CDBG: Certificate in Digital Business Growth

CIAM: Certificate in Agribusiness Management

CHRM: Certificate in Human Resources Management

CETS: Certificate in Exponential Technologies and Singularity

CBPM: Certificate in Business Transformation & Project Management

The program is completely capstone-based. Tekedia capstone is a research paper or a case study exploring a topic, market, sector or a company. It is the project component of Tekedia Min-MBA.

Theme: Innovation, Growth & Digital Execution – Techniques for Building Category-King Companies

Introduction

Over the last few decades, digital technology has emerged as a very critical element in organizational competitiveness. It has transformed industrial sectors and anchored new business architectures, redesigning markets and facilitating efficiency in the allocation and utilization of factors of production. The impacts have been consequential: continents like Africa are moving towards knowledge-based economic structures and information societies, comprising networks of individuals, firms and states that are linked electronically and in interdependent relationships. In this program, we will examine this redesign within the context of fixing market frictions and deploying growth business frameworks in a world of perception demand where meeting needs and expectations of customers are not enough.

Program Time: Sep 14 – Dec 5, 2026

Venue & Format: Online via videos, articles, webinars, and flash cases. Program is self-paced which means you consume the materials at your own time and pace. It is completely online. Where you live or your time zone would not be an issue as program is not live-delivered.

Cost: US$170 (N120,000 naira). We have a payment plan, i.e. installment payment plan (email us for details)

Target Audience: This program is designed for professionals and students across functional areas like sales, marketing, technology, administration, legal, strategy, finance, etc across all business sectors and domains. The program is designed for:

Ambitious mid-level managers seeking to advance their careers by acquiring essential business knowledge and skills.

Busy professionals who value continued education but require a flexible alternative to a traditional MBA program.

Experienced professionals aiming to broaden their business acumen, enhance leadership capabilities, and explore new career opportunities.

Professionals in transition, committed to staying informed about business trends and developing skills for continuous professional growth.

Mid-level managers and executives across industries, driven to accelerate career growth and take on increased responsibilities.

Technology and innovation-focused professionals looking to strengthen business acumen and strategic thinking.

Aspiring entrepreneurs seeking a solid foundation in business management and growth strategies.

Consultants and advisors aiming to expand their knowledge base and provide comprehensive solutions to clients.

Professionals transitioning into new roles or industries, recognizing the value of upskilling for success.

Students and recent graduates seeking a competitive edge in the job market by combining academic qualifications with practical business skills.

Tekedia Mini-MBA program offers a flexible and comprehensive learning experience tailored to the needs of ambitious professionals, providing the tools and knowledge necessary to thrive in today’s dynamic business landscape. Participants will have the opportunity to acquire knowledge that has value and can be used in everyday business activities.

Learning Objectives: To innovate is to set a new basis of competition in an economy, business sector or market. Sometimes, it results in disruption. This program is designed for private (large, SMEs, startups, sole businesses), public and government institutions, and individuals. Participants will:

Master the mechanics of growth – the reward of innovation – through frameworks, cases and evolving strategies.

Understand how to undergo transformation journey that is fully aligned with corporate objectives through measurable and realizable benchmarks.

Acquire business capability tools that do not just RUN their firms but can TRANSFORM them.

Design corporate growth experiments in Lab sessions based on One Oasis Strategy, Aggregation Construct, Double Play Strategy, Accumulation of Capability Construct, and more.

ETC

Why Tekedia Institute

Interactive Online Learning: Engage with industry experts and fellow professionals through our state-of-the-art online learning platform, where you can access course materials, participate in discussions, and collaborate on real-world case studies.

Comprehensive Curriculum: Gain a deep understanding of key functional areas such as strategy, marketing, finance, operations, and more, equipping you with the knowledge and skills to excel in any business environment.

Practical Case Studies: Apply your learning to real-world scenarios through hands-on case studies and projects, allowing you to develop critical thinking and problem-solving skills.

Flexibility and Convenience: Access the program online from anywhere at your own pace, fitting your studies into your busy schedule without compromising your professional and personal commitments.

Expert Faculty: Learn from renowned industry practitioners and thought leaders who bring their expertise and real-world insights to the program, ensuring you receive the most relevant and up-to-date knowledge.

Benefits of Tekedia Mini-MBA

Enhance Your Leadership Potential: Unlock your leadership capabilities and develop the skills to lead teams, drive innovation, and navigate complex business challenges with confidence.

Master Business Excellence: Gain a holistic understanding of business functions, strategies, and best practices, enabling you to make informed decisions and contribute to organizational success.

Embrace Digital Transformation: Stay ahead of the curve by embracing digital technologies and leveraging them to transform your business and stay competitive in the digital age.

Accelerate Your Career: With the Tekedia Mini-MBA on your CV, you’ll stand out to employers, demonstrating your commitment to continuous learning and your readiness to take on new responsibilities.

Network and Collaboration: Connect with a diverse community of professionals, expand your network, and foster collaboration opportunities that can lead to future partnerships and career advancements.

Cost-Effective Investment: Enjoy the benefits of a comprehensive business education at a fraction of the cost of traditional MBA programs, maximizing the return on your investment.

We run optional three Live Zoom sessions (two weekdays and one Saturday). This provides a way for our members to ask our Faculty and experts live questions and get feedback.

Tekedia Mini-MBA certificate sample

Tekedia Institute offers certificates at the end of all programs.

Our Contact Email: info@tekedia.com

Refund policy is full refund within 6 days from start of a program; after that, none, but we can defer as requested.

Lead Faculty of Tekedia Institute

Prof Ndubuisi Ekekwe is the Lead Faculty of Tekedia Institute

PhD, Electrical & Computer Engineering, Johns Hopkins University, USA

MBA, University of Calabar, Nigeria

BEng Electrical & Electronics Engineering ( Federal University of Technology, Owerri, Nigeria)

Prof Ndubuisi Ekekwe invented and patented a robotic system which the United States Government acquired assignee rights. Dr Ekekwe holds two doctoral and four master’s degrees including a PhD in engineering from the Johns Hopkins University, USA. He earned undergraduate degree from FUT Owerri where he graduated as his class best student. While in Analog Devices Corp, he co-designed an accelerometer for the iPhone. A recipient of IGI Global “Book of the Year” award, a TED Fellow, IBM Global Entrepreneur and World Economic Forum Young Global Leader, Prof. Ekekwe has held professorships in Carnegie Mellon University and Babcock University, and served in the United States National Science Foundation Committee.

The South African press called him “a doctor of innovation” for helping organizations on the mechanics of business innovation, strategy, and growth. Since 2009, the Chairman of Fasmicro Group which controls many startups and entities has been writing in the Harvard Business Review. He was recognized by The Guardian as one of 60 Nigerians Making “Nigerian Lives Matter” on Nigeria’s 60th Independence Day (Oct 1, 2020).

Nigeria’s cryptocurrency regulatory framework has expanded further after the Securities and Exchange Commission (SEC) admitted seven additional companies into its Accelerated Regulatory Incubation Programme (ARIP), marking another milestone in the government’s efforts to bring the country’s rapidly growing digital asset industry under formal regulatory supervision.

The Commission disclosed the development in a statement issued on Friday, announcing that the newly admitted firms have been granted Approval-in-Principle (AIP), allowing them to operate within the regulatory sandbox under defined conditions while remaining subject to ongoing regulatory oversight.

The newly admitted companies are Bitbarter Technologies Limited, Luno Fintech Nigeria Limited, GetEquity Limited, Koinkoin Global Network Limited, Wrapped CBDC Ltd, Trovotech Ltd, and Blockvault Custodian Ltd.

The latest approvals significantly expand the number of digital asset businesses operating within the SEC’s supervised framework, following the admission of Quidax and Busha into the programme in August 2024. The move forms part of the Commission’s broader strategy to create a structured regulatory environment for cryptocurrency exchanges, custodians, tokenization platforms and other virtual asset service providers operating in Nigeria.

The SEC said the Approval-in-Principle confirms that each company has successfully met the admission requirements for participation in the Accelerated Regulatory Incubation Programme, but clarified that the approval does not constitute a full operating license.

“An Approval-in-Principle confirms that an entity has satisfied the Commission’s admission requirements for the Programme. Please note that it is not a final license and remains conditional on the entity’s continued compliance with all applicable regulatory, operational, and supervisory obligations,” the Commission stated.

According to the regulator, the admissions demonstrate its commitment to encouraging responsible innovation in Nigeria’s capital market while maintaining investor protection, market integrity and regulatory oversight as the digital asset ecosystem continues to evolve.

The latest approvals also signal the SEC’s determination to replace years of regulatory uncertainty with a clearer licensing pathway for cryptocurrency operators. Nigeria has emerged as one of Africa’s largest cryptocurrency markets, driven by widespread retail adoption, cross-border payments, remittances and growing institutional interest, even as the sector has experienced periods of policy uncertainty.

One of the newly admitted firms, Luno, described the approval as a significant step in its long-term operations in Nigeria. In a separate statement, the cryptocurrency exchange said the Approval-in-Principle followed an extensive engagement process with the SEC and provides a clearer regulatory framework for its expansion plans.

Luno, which began operating in Nigeria in 2015, said the approval strengthens its ability to serve both retail and institutional customers as demand for regulated digital asset services continues to grow.

Luno Nigeria Chief Executive Officer, Ayotunde Alabi, described the development as an important validation of the company’s regulatory approach.

“This is an important milestone for Luno Nigeria and a strong validation of our commitment to building responsibly in one of Africa’s most important cryptocurrency markets,” Alabi said.

He added that the regulatory approval would deepen the company’s engagement with customers and institutional partners while supporting its expansion into business-to-business (B2B) services.

Luno said regulatory clarity has become important as banks, fintech companies, payment providers, asset managers, and corporate organizations continue to explore digital asset products and blockchain-based financial services. The company disclosed plans to broaden its institutional offerings, including digital asset infrastructure, stablecoin applications, treasury management solutions and crypto-as-a-service products designed for businesses seeking regulated exposure to digital assets.

The latest admissions build on regulatory milestones achieved over the past two years. In 2024, the SEC granted Approval-in-Principle to Quidax and Busha, making them the first cryptocurrency exchanges to receive formal recognition under the Accelerated Regulatory Incubation Programme.

At the same time, the Commission admitted four companies into its Regulatory Incubation (RI) Programme to test their business models and technology under controlled regulatory supervision. Those firms included Trovotech Ltd, Wrapped CBDC Ltd, Dream City Capital and HousingExchange.NG Ltd. With Trovotech Ltd and Wrapped CBDC Ltd now progressing into the Accelerated Regulatory Incubation Programme, the companies move a step closer to obtaining full regulatory authorisation.

The SEC has consistently maintained that additional approvals will be granted on a case-by-case basis as applicants satisfy its regulatory requirements. It has also emphasized that Approval-in-Principle serves only as a precursor to full registration and does not represent a final license to operate.

The Accelerated Regulatory Incubation Programme functions as the Commission’s regulatory sandbox, enabling digital asset service providers and other investment technology firms to operate within a supervised environment while regulators assess their business models, governance structures, technology and compliance systems before issuing permanent licenses.

The framework is designed to help the SEC balance innovation with investor protection by allowing emerging financial technologies to develop under regulatory oversight rather than outside it.

The expansion of the programme comes as regulators worldwide continue developing comprehensive rules for digital assets, stablecoins, tokenized securities and other blockchain-based financial services. This comes amid growing institutional participation and increasing integration between traditional finance and digital asset markets.

in New York City")