Like WizKid, smile it’s a new week. Like Israel Adesanya, you need to pick your opponent (government policies) apart so that you can win regardless of the size of the threat posed by your opponent, welcome to this week in the capital market.

- At its 22nd September 2020 MPC meeting, the Central Bank of Nigeria’s Monetary Policy Committee (MPC) cut the monetary policy rate (MPR) by 100 bps from 12.5% to 11.5%. This is the second cut since lockdown was eased on 4th May 2020.

- At its 28th May 2020 meeting, MPC reduced MPR by same 100 bps from 13.5% to 12.5%.

- How does a cut in MPR affect you? We will answer this question by looking at the impact on savings account holders, Banks and Investors in the stock market.

- Let’s attempt what MPR is before we delve into its impact. MPR is an interest rate at which CBN lends to commercial banks and other clients. Why should you be concerned?

- MPR goes beyond just lending rate between CBN and Banks. It is the benchmark rate for tracking the movement of other market rates of interest and maintaining economic stability.

Download Slide

Impact on Savings: negative real interest rate widens

As mentioned above, MPR as a benchmark rate tracks other interest rates. E.g, It is used as a benchmark to track the minimum interest rate (“MIR”) on savings accounts, it is used to benchmark what you will earn on your savings deposits with Banks.

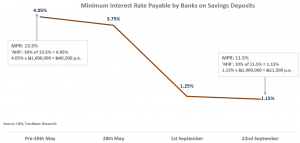

Effective 1st September 2020, you would recall that CBN reduced minimum interest rate payable by banks on savings accounts from 30% of MPR to 10% of MPR.

Please see the illustration on the graph below for a clearer understanding.

- Earlier in the year, when MPR was 13.5%, you could earn as high as 4.05% minimum interest on your savings deposits compared to the current 1.15%.

- From the graph, N1,000,000 savings deposit would earn a minimum interest of N40,500 per annum before the first MPR cut. That minimum interest has now reduced by over 71% to N11,500 per annum on the same amount, N29,000 loss. That’s the impact of the reduction of MPR!

- More painfully, if you consider inflation at 13.22%, your real return on saving with a bank will come in negative at -10.66%.

In this environment of subdued interest rates and rising inflation, there is almost no incentive for saving with a bank.

Impact on Banks: cut in MPR translates to lower funding costs, higher profits

The N29,000 loss by our savings account holder above is a gain to the Banks. Lower interest rate means lower interest expense and higher profits for the banks.

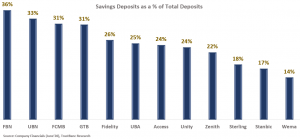

- The main source of funds for commercial banks is customer deposits – savings deposits, current account deposits, fixed and term deposits. Banks typically have strategies to target more savings deposits, because it’s cheaper compared to other forms of deposits.

- The cheaper a Bank’s savings deposit, the lower its interest expense/funding cost. Also, the higher a Bank’s savings deposits as a percentage of total customer deposits, the more it will benefit from a lower interest rate regime.

- Following the reduction of MPR from 13.5% to 12.5% and now 11.5%, the minimum interest payable by banks decreased from 4.05% to 1.25% and now 1.15%. Like we noticed in the half-year financials of some banks, we expect interest expense to reduce further across the Banking sector in the coming quarters.

From the graph, the biggest winners are First Bank, Union Bank, FCMB and GTB, our estimates were based on the 2020 half-year financials of our coverage banks.

We anticipate a drop in funding costs of over N7 billion based on the latest cut in MPR alone. Our estimates based on the MPR cut in May was over N17 billion interest expense savings.

While interest income could also decline due to downward review of rates for loans linked to the MPR, we expect the impact to be insignificant given that not many loans have rates tied to MPR.

In view of the above, we expect sustained upticks in the shares of banks.

Impact on Investors: cut in MPR acts like steroids for a sustained bullish stock market performance

Monetary Policy Rate is an economic indicator closely monitored by the entire trading world including investors in the Nigerian stock market. A change in MPR has a big impact on the stock market with very varied effects.

While it usually takes at least 12 months for a change in the interest rate to have a widespread economic impact, the stock market’s response to a change is often more immediate.

Faced with declining savings interest rate, lower yields on fixed income securities and expanding negative real return, we expect Investors to find their way to the equities market in search of positive real returns.

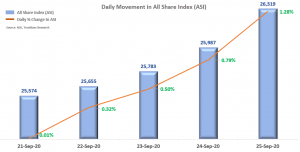

Last week, the performance of the market was flat at .01% on the first day of trade. The market jumped to 0.32% on the day the new MPR regime was announced. Since then, performance almost doubled on a daily basis to close the week with a gain of 1.28%.

Week on week, the equity market gained over 2.90% to record its best weekly performance in four months. Except for a few profit taking here and there to close the books for the month, we expect the market to continue its current bullish run.

Stock Recommendation

We are bullish on the shares of Zenith and GT Bank. Despite the declining macro environment, we believe the structure, adequate capital and liquidity buffers of these two Banks provides them with enough resilience to weather the storm.

The shares of Access, UBA and FBNH also provide near-term speculative opportunities considering their low valuations.

Away from the Banks, we like the shares of Presco and WAPCO. Generally, we advise you to stay with dividend-paying stocks with strong fundamentals and management.

Risks

The virus is still alive. The recent spike in coronavirus infections may stall recovery in the Eurozone and United States. Another round of subdued economic activities in these economies will depress oil prices. This will further compound Nigeria’s weak macroeconomic environment.

As recommended above, invest in undervalued dividend-paying stocks with strong fundamentals and management.

Conclusion

In conclusion, the cut in MPR and its impact reinforces the need to diversify your wealth. If you had some part of your wealth saved and another part invested across different investment options, regardless of the twist in government policies, you will be better off.

Imagine if you had your portfolio under one roof that provides an opportunity to save, borrow, invest and trade securities. A wealth partner that will assist you with picking government policies apart and position you to be better off regardless of policy twists. Talk to us at TrustBanc.

Have a great week in the capital market.

This week in the capital market provides a cocktail of information, education and insights on how you can take advantage of investment and funding opportunities to grow your wealth.

Leave your questions and comments below. If you need private financial advisory, send your enquiries to azeez.lawal@trustbancgroup.com or call 08028379367. Advisory is free.