Common Attacks Against Enterprises Well, just like pollution was a consequence of the Industrial Revolution, there are several security vulnerabilities that come with the advance usage of the internet. Cyber attacks are exploitations of those vulnerabilities. For the most part inevitable, persons and enterprises have found ways to defy common attacks with a range of […]

20.1 – Planning & Managing Enterprise Network Structure

Managing Network Addressing & IP Addresses One of the basic skills needed for an administrator for successful programming and installation of IP network devices is IP addressing mastery. Every device connected to the network must be appropriately addressed, otherwise it will not be able to communicate. The administrator must be able to check the IP […]

20.0 – Planning & Managing Enterprise Information System

Enterprise systems planning looks at the entire business to decide what information system the enterprise requires to satisfy its objectives. For large businesses, this can be a costly procedure involving specialists and consultants, but smaller businesses can usually carry out analysis and planning in-house. Fundamentals for effective enterprise systems planning are the survival of a […]

The Prevalence of Half-hearted Digital Banking Practice Among Nigerian Banks: A Look at Access Bank and FCMB

Despite recent reforms in the Nigerian banking industry to make them more robust in securing the money of their depositors, customers and other stakeholders, there are clear indications that the sector needs a closer look in terms of its customer relationship management. The banking industry, as a service sector, is generally characterised by three of the five recognised features of service. These include intangibility, inseparability and heterogeneity. While intangibility refers to the non-physical nature of services, inseparability means that the rendering and consumption of services are done at the same time. This makes a bank-customer relationship an emotional/customer experience driven process where the quality of service is measured by how the customer is treated in the course of interacting with the bank.

Heterogeneity, which is the last of the three features, identified the role of human beings involved in the consumer service process. This feature sees service as an act of performance that cannot be repeated the same way when performed by the people involved in attending to consumers. Even in sectors, such as the banking industry, where there are standardized procedures of attending to clients, yet, human interaction makes service rendering a heterogeneous venture. From the analysis, it is argued that the management of Nigerian banks should understand the context of their operations especially for those commercial banks.

It is equally important to have a clear understanding of the process of the customer experience while patronising a bank. There is pre-service stage, service stage and post-service stage. The pre service stage is the point where customers are looking for a banking firm to bank with. Here, they have the alternatives to select from. The actual service encounter is the point at which customers relate with the banks in order to meet their financial needs. In short, it covers service requests, interaction with the personnel of the service provider and service delivery. The post service stage is the stage where the consumers review their experience with the service encounter. It is the point where the consumer’s expectation is reflected against the quality of the service outcome. The consumer evaluates the service experience against the perceived expectations. At this stage, future intentions to purchase are also determined.

A satisfied consumer whose perceived expectations are met by the quality of service may not only return to make a repurchase of the service but also tell others about their experiences and vice versa. This shows that banks, as a service sector operator, must have an efficient, seamless customer relationship management. But, the question is – is this the experience? The answer to this question is in the negative drawing from personal experience and complaints from some bank customers.

The first complaint is that of Mutiu Iyanda. He is an account holder with Access Bank who has not been able to resolve a 3-month complaint of a blacklist of his account. According to the angry and dejected customer of the bank, he has not been able to meet his financial responsibilities which has affected him badly. He detailed his attempts to get the issue resolved and the stumbling blocks he has continued to meet both at the branch where his account is domiciled and even from the head office of the Herbert Wigwe-led bank. How could the resolution of a compliant could still be pending three month after it was lodged? Why should a digital problem require an analogue situation? These are questions for Access Bank, Nigerian Deposit Insurance Corporation and the Central Bank of Nigeria who are the regulators of the banking sector.

Picture:

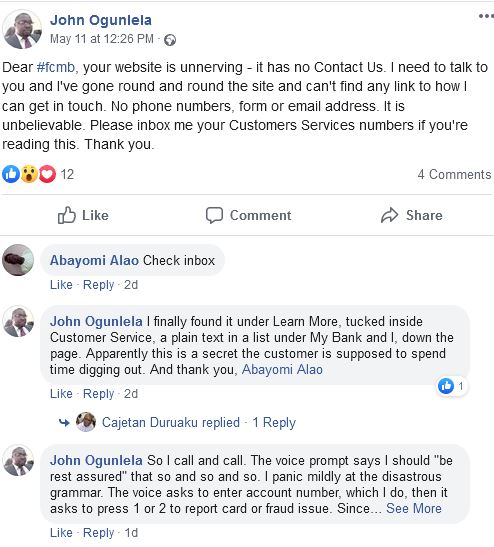

The second complaint comes from a colleague, John Ogunlela. He holds an account with First City Monument Bank. He had some issues to be urgently resolved, he found it difficult reaching the customer service. He quickly came to his Facebook page to call out the bank. He queried, “Dear #fcmb, your website is unnerving – it has no Contact Us. I need to talk to you and I’ve gone round and round the site and can’t find any link to how I can get in touch. No phone numbers, form or email address. It is unbelievable. Please inbox me your Customers Services numbers if you’re reading this. Thank you.” Upon help from a Facebook friend, who sent a Direct Message to him on how he could locate the buttons to get across to his bank on its own website, he still had a terrible experience. He narrated : “I finally found it under Learn More, tucked inside Customer Service, a plain text in a list under My Bank and I, down the page. Apparently this is a secret the customer is supposed to spend time digging out. And thank you, Abayomi Alao.”

It did not end there. He recounted his experience further: “So, I call and call. The voice prompt says I should “be rest assured” that so and so. I panic mildly at the disastrous grammar. The voice asks to enter account number, which I do, then it asks to press 1 or 2 to report card or fraud issue. Since I am not reporting fraud or a card issue, I disregard the statement. Pronto the call terminates. Then, I try the Whatsapp contact option. The faint double tick shows the message is diverted to the device. Seven hours later I am still waiting for a reply. The email I sent is also seven hours old. FCMB customer service desk used to be one of the best and it was midnight here. They kept on top of it and called me ceaselessly until I was okay. I am sad for them this is how they now operate. I will have to start all this tomorrow because I just won’t brave those Covid queues and crowds in the banking hall.”

It is easy to punch this argument based on the small number of the dissatisfied customers cited. However, the seriousness of the situations for the two banks would be better appreciated when the efficacy of the words of mouth especially in this digital era is taken into consideration. John Ogunlela has not less than 4,458 followers on Facebook where he shared his predicament. Mutiu Iyanda too has access huge following on an international blog that he writes for and where he has written an open letter to the Access Bank’s CEO, Herbert Wigwe. He has as well lodged a complaint with the Federal Competition and Consumers’ Protection Commission.

Again, considering the environment of the banking service, it is critical that banks ensure memorable experience for their customers. Whether on digital platforms or in the banking hall. The two complaints are representative of the issues an average bank customer deals with in Nigeria. Discomforting and hurtful experiences of the customers, such as the ones narrated above, has the tendency to affect financial inclusion drive of the Central Bank of Nigeria.

Insights drawn from a study reveal that despite the fact that Nigerian commercial banks have digitalized their operations, their customers still face a great deal of issues as they process their daily banking transactions. The customers still have to fill forms, queue within the banking halls waiting to be attended to. This is against the 2017 cashless policy of the Central Bank of Nigeria. That Nigerian commercial banks are claiming digital prowess but operating on an analogue mode is counter-productive to the financial inclusion drive of the apex bank. In a 2017 Global Findex Database, 40% of Nigerian adults have an account with a bank or a mobile money provider. The report further revealed that Nigeria and six other countries contribute nearly half of the globe’s unbanked population of 1.7 billion.

In conclusion, it is important to continue to ask questions on the digital banking practices in the Nigerian banking industry. How would a bank whose processes have been digitalized find it difficult to enable a seamless digital consumer service contact? In the same vein, how could Access Bank not able to resolve a complaints for three months? Where is the intelligent bank as claimed by the bank’s Chief Executive Officer? The complaints of the two customers are different in scope but are tilted towards the same direction- the digital platforms should ensure issues are resolved with customers’ minimal or no contact with the banking halls.

Madagascan Covid-Organics: A Challenge to Nigerian Herbalists

The controversy surrounding Madagascan COVID-19 cure is throwing Nigerians and other Africans into a frenzy. Some stood against it while some are die-hard fans of the medicinal drink. Those that have their reservations are viciously attacked by its fans. Medical practitioners and scientists have called attention to the fact that Madagascar has not published any clinical trial data on the drug. They also revealed that the drug has not passed through any peer review and third party verification and approval. However, their observations are discredited by many Africans, who claimed that these medical practitioners and scientists only wanted to save their jobs. The advocates of this drug also claimed that the medical practitioners and scientists condemn it because it is made in Africa. They refused to listen to reason.

The drama surrounding this cure started when the Madagascan President, Andry Rajoelina, claimed that WHO’s hesitation to declare the drug, branded COVID-Organics, as a potent cure for COVID-19 is because Madagascar is an African country and the 60th in world poverty ranking. He claimed that 55 Madagascan COVID-19 patients were treated with the herbal drink and they have all been cured. He also explained that COVID-Organics was developed by a research institute known as Malagasy Institute of Applied Research, but he failed to answer the questions surrounding clinical trials and tests.

The accusations by the Madagascan president is unfounded because WHO has not approved any reported newly developed drugs for COVID-19 and should, therefore, not jump in to approve those whose contents, indications, contra-indications, effects and adverse effects are not known. But this accusation played both political and economic role for the country. By playing the victim, the country has turned the world’s attention towards her and has used the campaign to offer to the world that which it craved for – cure and prevention of COVID-19. Many African countries have purchased the medicine for the treatment of their COVID-19 patients. Even Nigeria has joined the bandwagon of buyers though Lauretta Onoochie, the Personal Assistant to President Muhammadu Buhari on Social Media, revealed in her Twitter page that the consignment Nigeria is flying to Madagascar to pick is “a gift” from the generous country.

As we wait for verification, approval and confirmation from the countries that purchased this Madagascan COVID-19 cure (which should be out within the next ten days according to Rajoelina), let us turn to our numerous agbo sellers, agbo makers and herbal drug mixers and ask them, “HOW FAR?”

There is no market in this country that doesn’t have megaphones mounted in strategic places for herbal drug sellers. These people continue to remind us that we have everything it takes to heal diseases embedded in plants and that we should stop patronising “chemical drugs”. They also discourage people from going to hospitals because doctors make sickness worse, or that they treat symptoms without treating the sickness. Don’t get me wrong, I know that herbal drugs work, at least I used Dogonyaro to treat malaria during my service year in Zamfara because I noticed that most of the drugs sold in Kaura Namoda were uncertified by NAFDAC. My point here is that these people need to come out to prove their worth.

When COVID-19 started its ravage in the country, some herbal healers came out to claim that they have the cure for the disease and invited the people and the government to send patients to them. Even some religious “healers” made their own claims too. The herbalists’ claims were not tested as the government did not send patients to them nor take them to patients. Of course, even if they healed any private individual, they wouldn’t come out to say so because they may be arrested. But with the discovery and the release of COVID-Organics, the herbalists have their opportunities to show their skills.

Concerning Nigerian herbalists being given the opportunity to also show their skills, BBC Pidgin reported that the DG of NAFDAC, Prof. Mojisola Adeyeye, invited interested traditional medical practitioners on Wednesday, 13 May 2020 to submit their applications and drugs for clinical trials. She said that Nigerian traditional medical practitioners and academics only claim the potency of their drugs on social media and other media outlets without approaching NAFDAC for testing and approval. She revealed that of all the people claiming expertise on treating COVID-19 only one person has submitted an application. She, however, noted that the individual that submitted the application wishes to treat the symptoms of COVID-19 and not to cure the disease.

So here is an open door, and window, for all the owners of the megaphones blaring away in our markets. They need to hear about this opportunity and make use of it. All they need to do is conduct research, which they have obviously been doing before, and then bring up a cure just like Madagascar did. Nigeria too has herbs and roots that can cure everything.