In the startup world, we like growth and always spend time planning how to make it happen. Job titles like VP, Growth; Manager, User Growth; and Team Lead, High Growth are now common. There is nothing wrong with that: growth is the heart of any business. In web business, because of the elements of network effects and the benefits of invertibility construct, the thinking is that growth drives the business. Yes, growth is important; but without an important margin in business, over time, the business will die. The profit margin is the most important element in any business formation and operation. It is the fuel that gets a business going. It is the enabler, catalyst and the anchor of the corporate long-term vision.

Largely, we are in business for profit margin. It may not be obvious because there are many companies which operate for years without profitability, by raising tons of money, in successions. But even with that, over time, the companies will be expected to make money. Even if the companies are sold, the buyer must still have to find profitability in the operations for the following reasons:

Running and Growing Companies: It is only by making profit that a business can be sustained over time. Without profit, the mission is stalled. The vision of accelerating prosperity and the welfare of people can only happen when a firm makes money

Corporate Social Responsibility: Doing good as a business does not happen with free water or air. Money funds great ideas to help communities and societies. To do that, a firm must make profit

Investors Part: When investors put money in your company, they are really investing in your profitability. It is irrelevant if you are making money today or not. The fact is that they do believe that you will make money in future. It is from that profit that you would pay dividend. If the firm is publicly traded, profitability provides a good metric to the health of business. Generally, it does impact the growth of the stock.

So, as you work on the mission to change the world, it is important to understand that you must make money doing so. Making money, ethically, is the core business you are in, because without making money, you may be unable to help society. The passion for profit has pushed even typical non-profits to explore ways to make money so that they can serve communities better.

The Kenya Red Cross is a very good example: the charity runs a hotel business in Kenya and invests in education, farming and more. At the end, it generates good profit margin that it does not need any donation to support its mission. With ventures generating profits, executing the mission of Kenya Red Cross has been simplified. I spent a day with the CEO early this year and was thrilled on how they have fused business with helping communities, at scale. They have more functioning ambulances than the Government of Kenya, and they run a top-rate school on hotel management with students coming from far away China, Nigeria and India.

If a charity can see that profit margin is vital, it means that for-profit startups have no hiding place. Indeed, “No Margin, No Mission”, as Fortune aptly captured it, recently. You must find ways to have good margin because that is the first mission in business. Other missions emanate from it.

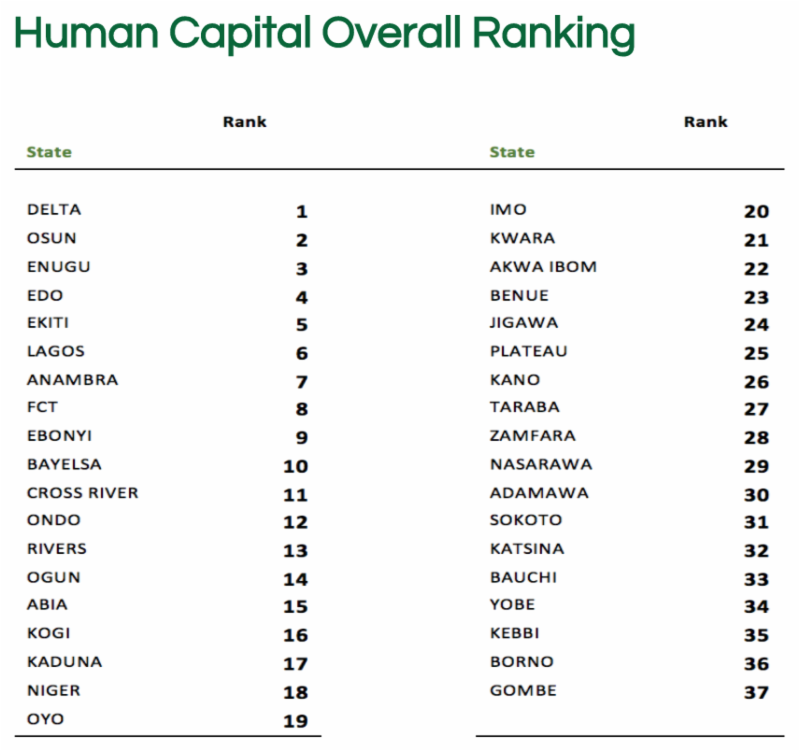

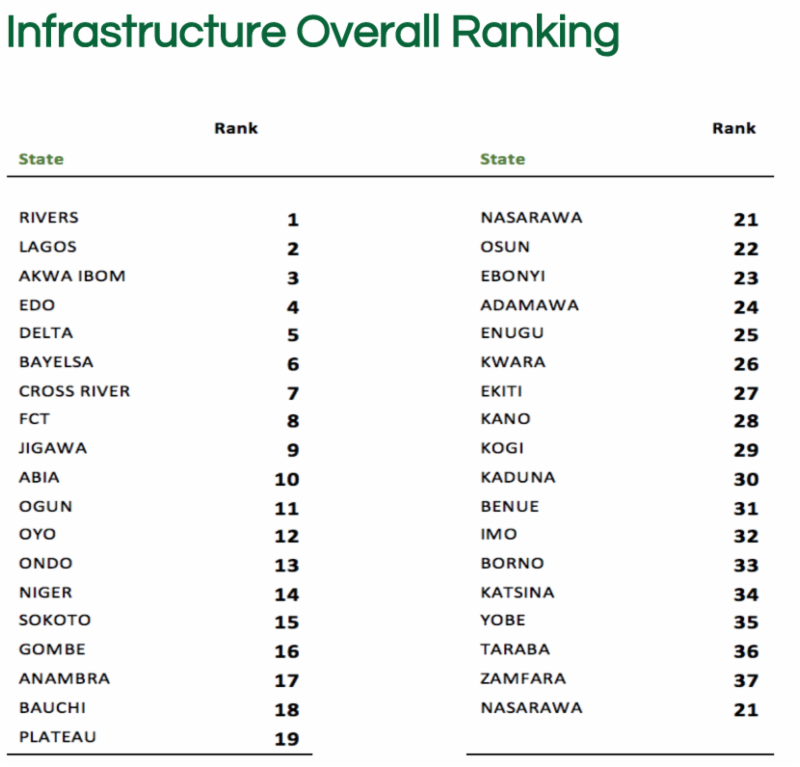

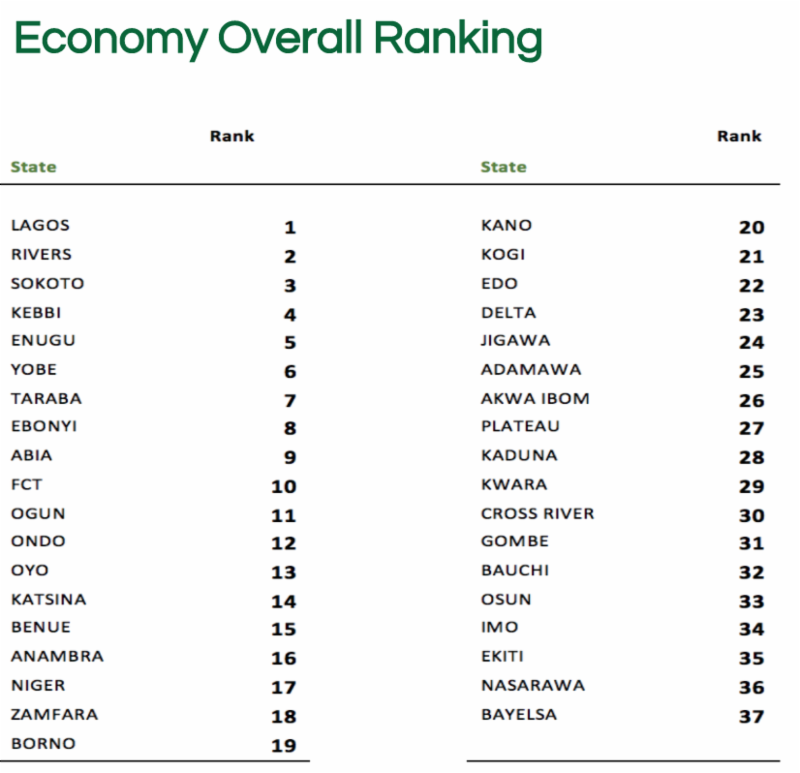

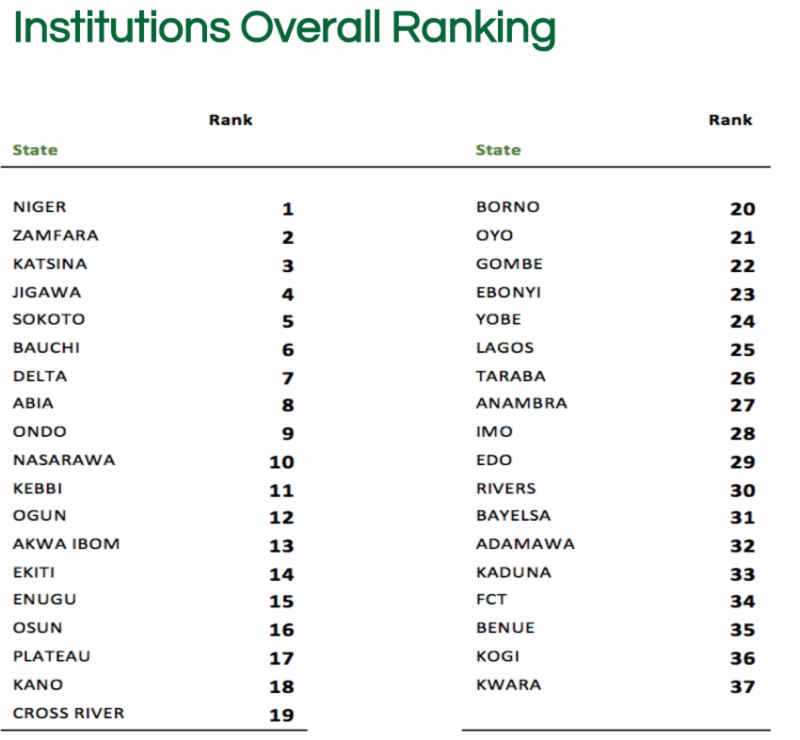

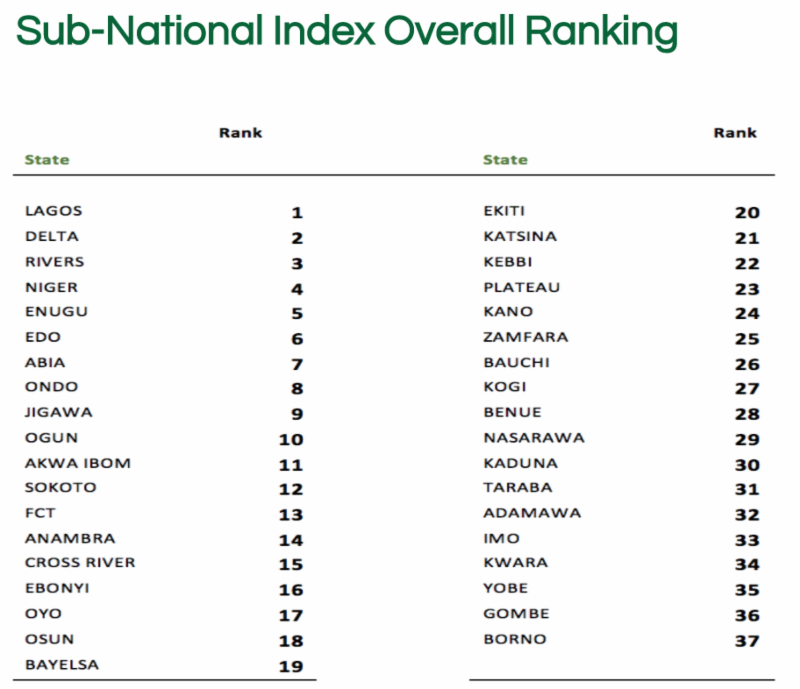

The National Competitiveness Council of Nigeria has released Nigeria’s first Sub-National Competitiveness Index. It is a two year research into the factors that drive competitiveness in Nigeria’s 36 states and the FCT. Ford Foundation and the Tony Elumelu Foundation funded the research. The research covered more than 2,000 businesses, 8,000 households, 400 indicators and 4 pillars.

Pillar #1 is Human Capital which covers education, migration, gender equality and heath: Delta State is #1 and Gombe is #37.

Pillar #2 is Infrastructure which covers roads, electricity, airport, telecom, waste and water: Rivers is #1 and Zamfara is #37

Pillar #3 is Economy which covers access to finance, state finances, business-sophistication and tax: Lagos is #1 and Bayelsa is #37

Pillar #4 is Institutions which covers security, transparency, justice, corruption and permits. Niger is #1 and Kwara is #37.

Wema Bank is on a great mission: the bank wants you to know about ALAT, its digital (mobile) banking solution, even more than the bank itself. It does seem that the bank has decided on what its future will be, and that future is ALAT. If you drive through 3rd Mainland Bridge, Lagos, you will see the ALAT advertisements with barely noticeable logo of Wema Bank. They are positioning ALAT as the future, even providing a website for it, the alat.ng. The following notes are evident with regards to Wema Bank’s ALAT:

Strong Promotion: Wema Bank is promoting ALAT more than the bank itself. I do think over time, the brand ALAT will become bigger than Wema Bank, and Wema Bank will fold into ALAT. Simply, Wema Bank wants the young people to know about ALAT, and not necessarily Wema Bank.

Unique Domain: The bank is one of the few banks in Africa that created a unique domain for its mobile banking solution. This means that ALAT itself is expected to become a bank, but without the traditional branches.

Strong Digital Future: Wema Bank is banking on a strong digital future. And ALAT will provide that to it. They have invested massively to create this product and are also doing more to make people know about it. It offers some of the best deals in African banking with 10% interest rate ( I noticed that one on 3rd Mainland Bridge). This is the future of Wema Bank.

Wema Bank is brilliant on what it is doing with ALAT. I have noted in the past that one of the ways of dealing with the heavy regulations banks face is to create separate fintech companies and run them to support the bank products. In other words, a bank creates a fintech company that markets its products, even when doing other things. The advantage is that the fintech can move fast, without the regulatory challenge. While a fintech can use a press release to be in 54 African countries at once, a bank has to work with the respective central banks before it can operate in the countries. That gives the fintech firms the advantage to move fast and corner the opportunities. But if a bank has its own fintech, sequestered from its operations, and complying with regulations, it can compete more fiercely with the fintechs.

ALAT is the first step for Wema Bank. In the next few years, depending on its progress, ALAT can be divested from Wema Bank, to allow it to compete more aggressively in the African market without being tethered to a bank and the associated regulation. The regulation is important and there is nothing wrong with that: banks like Wema Bank take customer deposits, unlike most fintechs, and should be regulated. So, ALAT can become an operational arm of Wema Bank while the bank remains a dumb pipeline, typical of most traditional banks today (i.e. not much intelligence due to lack of deep insights), to support what that modern banking named ALAT does. Perhaps in 10 years, Wema Bank may even simply change its name to ALAT if this new modern banking solution evolves into its future.

ALAT is a bank, and it can become a truly African banking institution, if it pursues new opportunities in Africa, with growth typical in most highly scalable businesses. I am expecting the management to make ALAT a pan-African “bank”, and use it to redesign the banking experience for young people which it continues to pursue. Wema Bank is working. It is on ALAT now and that is a good thing.

I have written extensively on the implications of Internet on businesses. We are enjoying the tremendous productivity gains which technology has made possible. But in the future, Internet will cause massive economic dislocations in markets and economies. Yes, at maturity level, Internet could enable seamless linkages between sellers and buyers in many industries: the implication is that many companies will disappear. Who needs an accountant when all transactions are powered by blockchain? Many areas we see in fintech (financial technology firms) will go.

While ICT provided unprecedented productivity in the Nigerian banking sector, Internet is seriously “destroying” value. This is a “problem”. ICT made them, Internet could destroy some of them. Internet is bringing the construct of creative destruction in the Nigerian banking sector where values are destroyed and new opportunities unlocked. But those new opportunities are not going to be, exclusively, within the controls of the banks.

What Internet is doing today is expanding distribution of banking services thereby putting pressure on banks to control pricing on their own terms. Before Internet, they could charge huge fees to transfer money for clients to foreign accounts via their treasury departments, but today, with internet, there are options. The customers could simply use their debit and credit cards to settle the bills without first spending money on bank fees.

That future is not going to be very far: IBM has started building the infrastructure, at scale, of the 21st century banking: the blockchain banking. Yes, IBM and its partners have started making a business on what most thought was just an idea. It is now making it possible to move money across borders, seamlessly and efficiently.

In a breakthrough for payments technology, IBM and a network of banks have begun using digital currency and blockchain software to move money across borders throughout the South Pacific.

The significance of the news, which IBM announced on Monday, is that merchants and consumers will be able to send money to another country in near real-time, accelerating a payments process that typically takes days.

The banking network includes “12 currency corridors” that encompass Australia and New Zealand, as well as smaller countries like Fiji and Tonga. It will reportedly process up to 60 percent of all cross-border payments in the South Pacific’s retail foreign exchange corridors by early next year.

The news also comes as an important validation of blockchain technology, which has long promised enormous efficiencies for the financial sector, but has been slow to move from the concept stage to the real world.

Blockchain, which relies on a disparate network of computers to create an indelible, tamper-proof record of transactions, is most famously associated with the digital currency bitcoin. But it can be used in many other applications such as tracking shipments or, as in this case, to record a series of cross-border transactions.

If IBM gets this right, every bank in the network will be paying IBM tax to use its solution. This also means that the remittance business will likely collapse for most African banks. The very product which no fintech or bank in Africa has been able to build will now be made possible. I have discussed of the need to build a truly pan-African digital remittance/transfer banking product which is agnostic of location or currency in Africa. None of the products we have today meets that standard. Largely, I envisage a situation where all you need to buy and sell across Africa is one bank account in just one African Union country. With that, you do not have to even think about the specific currency of that account as technology will seamlessly make it possible to access other African markets for payments, transfer etc. The banks or fintech companies must still comply with all regulations related to inter-national transfers, forex etc. The only difference is that customers will not see them as they will be hidden with technology. What IBM is doing could potentially fix that friction and that means it will take major revenue base from African banks.

The IBM Banking

IBM has moved into banking without necessarily being a bank. That is a very good position to be. If it can pipe transactions across its systems, the real banks will pay taxes to use its networks. IBM will become the 21st century SWIFT (society of worldwide interbank financial telecommunications), a global payment network, assuming that the international payment network and enabler does not evolve. Many have written on the power of Amazon on consumer commerce, and the implications to markets.

But Amazon’s unprecedented logistics and delivery infrastructure, paired with access to personal data about Americans’ purchasing habits, means it is unique in the history of global commerce. No company has ever wielded this combination of consumer insight and infrastructure, say historians and legal analysts, which means the company grows stronger and less assailable with every purchase.

But what Amazon is doing will be small if IBM can make itself the category-king for blockchain banking. In other words, if IBM can build a system that essentially makes SWIFT irrelevant, IBM will have the highest impact in modern banking and commerce. The influence of Amazon in America cannot even come close because the implication is that IBM can just provide the infrastructure and over time move into other areas like insurance, legal contracts and more. The key thing is becoming #1 to enjoy the network effects and the benefits of invertibility construct.

All Together

This is a total redesign in the structure of digital commerce. Blockchain will have consequential impacts. There is nothing that it cannot power including making it possible for Finnair, an airline, to weigh its customers in Helsinki airport to ascertain that its estimated total weight, fuel, and safety are accurate. Of course, banking is going to be the first area that will be affected because that is where the money is. I do think African banks should work hard to form their own consortium with local technology leaders for intra-African remittance, at least, and get the African Union to charter that blockchain network. We need the regulation that makes transactions on blockchain to be legally enforceable and binding and that means governments may need to make that clear to avoid any uncertainty. This becomes necessary because at the onset of the web, most banks were not accepting email documents as legally binding. But over time, nations upgraded their laws to make it clear that emails and digital documents are valid in courts. We need same for blockchain and I hope Africa Union leads there. If they do, local banks will have the opportunity to build the capacity before the foreign ones define the markets.

Amazon plans to dominate the retail world by using its best product: the e-commerce operation. This product will be accumulating losses even as it takes retail market share from physical stores and malls. The strategy is that over time, Amazon will deliver fatal wounds to many physical stores that few will exist.

But that is just part of the equation. As Amazon bulldozes and dismantles physical stores, more of them will move online. Amazon hopes to provide the platform through its Amazon Web Services for most of these companies. Yes, Amazon has the best solution for these physical stores to operate online, after they have lost any relevance in the physical domain.

Simply, Amazon’s ecommerce operation can make losses, provided that incurring the losses will create new business opportunities for the AWS which will have more customers as offline retails move digital. With this model, it does not really matter if the e-commerce ever makes profit since its impacts are generating businesses for another unit of Amazon.

Amazon has no choice: if it does not pursue its loss-enabling market share against physical stores, they will not move online to require the services of the AWS. (Of course, I am exaggerating here. There are many other areas AWS can make money, including supporting non-retail businesses. But I hope you get the point.) So, there is a big correlation: the more businesses move online, the more potential opportunities for AWS, the cloud services industry leader. It does not matter if the ecommerce makes any money as it causes havoc in the markets.

This Amazon’s strategy is the reason why any African ecommerce company that is copying it will likely struggle. None has a unit that can deliver this kind of reverse gain that Amazon enjoys with AWS despite its losses in the ecommerce business. Without an equivalent of AWS, any Amazon’s cloning strategy becomes half-baked because the strategy will fail to have the profit-enabling element.