My ebook, Africa’s Sankofa Innovation, will be launched on September 1 2017. Besides the book, I will be publishing regular and exclusive articles that focus on business, innovation, and technology, in and around Africa with global perspectives. The articles will explore how entrepreneurs, investors, business leaders and other stakeholders can unlock value. The articles will be longer than the typical ones I share here on Tekedia. Apart from these exclusive in-depth articles and the ebook, Tekedia remains free to the general pubic.

For access to the eBook and the exclusive contents, a $20 annual subscription is required. Interested readers can pay with credit card, debit card, or Paypal processed via Fasmicro Group, my U.S. firm. Those in Nigeria can pay via our Nigerian bank accounts; the equivalent is N7,000.

All proceeds go to African Institution of Technology (AFRIT), my 501(c)3 non-profit with the United States Internal Revenue Revenue, to fund our operations. (Put EIN 30-0752559 on the IRS search site) Just as I assisted many schools in Africa on embedded electronics, I have a plan to assist in the areas of AI and big data. Putting subscription on these contents will ensure I can pay people that will work with us on this community service.

Posting here is a hobby which I enjoy during free pockets of minutes. We are seeing user growth evolving. I am hoping most will join us as we work to support African schools to deepen capabilities in AI and big data.

Most Nigerian insurance companies have websites. And some have small digital stores to make it easier for customers to pay premium. Apart from these two efforts, there is nothing else, on average, at the consumer side, in terms of new internet-based technologies you can see in the industry.

Sure, they have adopted information technology which has delivered productivity gains in the industry. That has also brought good returns to the owners and investors in the industry. The same thing happened in the banking sector where productivity unleashed unprecedented value creation by the new generation banks.

This ICT worked in the Nigerian banking sector. It brought into existence a new generation of banking institutions, about thirty years ago. About three decades ago, some Nigerian entrepreneurs saw opportunities that they could use better service delivery, anchored on technology, to redesign the structure of Nigeria’s banking industry.

The Nigerian insurance industry is largely on stasis. Remove the automobile insurance which people pay just to make sure the Police does not detain the car, every other product is not that popular. Customers that pay for the automobile insurance never really expect to call the insurer when a problem arises. The service quality is extremely poor that no one gets any decent value. They simply tax us with the premium paid because that is what the law of the land says: we must have insurance to drive cars, even if the insurance product has minimal value.

In 2015, according to the Nigerian Insurers Association (NIA), the volume of business underwritten by the insurance industry reached N350 billion ($1 billion), against N294 billion in 2014. This represents an increase of about 19 per cent. The industry remains very small and will need to grow. At $1 billion premium, it is less than 0.40% of the GDP of Nigeria. That is troubling.

The Nigerian Insurance Industry

The Nigerian insurance market is a paltry $1 billion (by premium sold) and that is for a country with more than 180 million people. (By comparison, the global market size is $4.55 trillion.) Over the years, Nigerian insurers have been unable to expand this market owing to lack of innovation.

South Africa accounts for almost 80 per cent of all premiums in sub-Saharan Africa and the country has an insurance penetration rate — the total value of insurance premiums as a proportion of GDP — of about 13 per cent, well above the developed world average. Of the rest, Kenya is among the most advanced, with a penetration rate of 3 per cent. Nigeria’s, in comparison, is about 0.4 per cent, even though it is Africa’s most populous.

The Nigerian Insurance Industry includes the following sub-sectors: Composite, Non-life, Life and Reinsurance operators. Over the last five years, the Nigerian Insurance Industry has grown at a compound annual growth rate (CAGR) of 11%, buoyed by increased capitalization as well as the introduction of policies aimed at promoting the local market.

Nonetheless, the industry remains challenged with low apathy from the Nigerian populace and weak policy enforcement practices, resulting in a low penetration ratio. These challenges however present enormous opportunities when benchmarked with other African countries especially South Africa. The industry has room to grow, if it can innovate.

The Internet Problem

By not getting into the internet, the insurance industry will not have the same level of challenge: the expanded distribution channel which has caused major challenges on media, airlines, education, banking, and other sectors.

While ICT provided unprecedented productivity in the Nigerian banking sector, Internet is seriously “destroying” value. This is a “problem”. ICT made them, Internet could destroy some of them. Internet is bringing the construct of creative destruction in the Nigerian banking sector where values are destroyed and new opportunities unlocked. But those new opportunities are not going to be, exclusively, within the controls of the banks.

But they are wrong – the future of commerce will be Internet-based and the earlier the insurance sector begins to move into that domain, the better. They may avoid the competition from InsureTech, insurance technology startups, but the future cannot be avoided. We need to see innovations, in the insurance industry, just as the banking sector is demonstrating on the web. I am very sure that the industry is not avoiding Internet in order to preserve value since Internet brings competition and can destroy value (yes, it does also create value, but the incumbents can see value dislocation). Rather, they are not on the Internet because they do not innovate. They like to blame the customers for not buying insurance, even though they have not put forward a compelling reason, through product innovation, for people to do so. They should be thankful that customers even buy insurance, primarily automobile insurance, because the law requires so.

Internet can help them innovate and evolve product vision that can meet the needs of Nigerians. But for that to happen, the players must show interest on the possibilities of the internet.

All Together

The insurance industry in Nigeria has used IT for productivity gains. Now is the time for the next level of innovation which is taking the insurance industry to the web. What they have been unable to do for decades – industry penetration acceleration – can happen if they digitize their products and make it possible for Nigerian entrepreneurs to participate via InsureTech. Should that happen, new products will evolve, and could actually deliver the aha moment that will make Nigerians begin to like buying insurance. The time is now: Nigeria needs a 21st century insurance industry.

As you read this piece, more business leaders will continue to express disaffection to the president of the United States, Donald Trump, on how he responded to the racist parade in Charlottesville, Va. Over the last few hours, some members of the President’s Council on American Manufacturing have resigned. They do not want to be associated with an American president who cannot stand against racism, even when it is obvious.

Mr. Trump’s remarks came amid a growing rift between the White House and the business community that has emerged since the weekend’s violence in Charlottesville, Va., and criticism of Mr. Trump’s response to it. Six members in two days have stepped down from the president’s Manufacturing Jobs Initiative.

Among those CEOs are Merck CEO Ken Frazier, Intel CEO Brian Krzanich and Under Armour CEO Kevin Plank. .

Without wasting space on what Trump believes as a human being, I want to focus on the lessons, from what is happening. The way leaders behave and conduct themselves can affect pipelines for talent in their businesses. Just as Trump is going to find it harder to find top CEOs who can work with him on whatever he wants to do, it is the same way a business leader could struggle when his/her behavior alienates talent.

That people can run away from the President of the United States tells me that in this age of Internet, with eternal memories maintained by Google, there are limitations on the powers of offices. Indeed, people that occupy those offices matter. Today, Trump is the president and people know that. That means, before the eyes of these CEOs, who are leaving him, they see Trump and not just the most powerful office in the world.

So, do not just assume that holding a position is what matters. People will correlate the power of that office with the dignity the person holding it brings to it. Where there are many deviations, few will like to answer the call. When that happens, instead of working with A-Team, you are going to struggle with B-Team.

We continue to learn on the Trump movie which is still playing. But so far, we can agree that your power in any position means nothing unless you, the person, bring honour, decency and valor to it. The men and women that hold offices are ornaments that decorate the seats of power. The seats lose the efficacy if the ornaments are defective. But radiance emerges out of the seat when the ornaments are made with the finest quality.

Your talent problem – not being able to hire and retain the right people- may be a problem you created yourself. The most powerful person in the building could be so powerful that he/she blows all the fuses along the way. Indeed, the effervescence of power only lasts longer with the vivacity of human dignity.

Speaking with someone today, I came to the realization that, at the moment, many could be confused on the core difference between having an online (yes, digital) store and running an ecommerce company. The industry definition of ecommerce may not help, because they use the term “ecommerce” when transactions take place, only, on the internet.

Electronic commerce or ecommerce is a term for any type of business, or commercial transaction, that involves the transfer of information across the Internet. It covers a range of different types of businesses, from consumer based retail sites, through auction or music sites, to business exchanges trading goods and services between corporations. It is currently one of the most important aspects of the Internet to emerge.

Ecommerce allows consumers to electronically exchange goods and services with no barriers of time or distance. Electronic commerce has expanded rapidly over the past five years and is predicted to continue at this rate, or even accelerate. In the near future the boundaries between “conventional” and “electronic” commerce will become increasingly blurred as more and more businesses move sections of their operations onto the Internet.

Technically, “ecommerce” needs to have been transactions that take place on any electronic medium. This means those POS-, ATM-, and Internet-based transactions could be included, as they are all “electronic” representing the “e” in “ecommerce”. However, the term has evolved that ecommerce is simply associated with Internet-executed transactions. When you pay with your credit card in a store, you do not think of ecommerce even though the card itself is an electronic system which has facilitated that transaction. When you transfer money via ATM, ecommerce does not come to mind. Those other types of transactions are now loosely referred to as digital commerce. The internet has taken ownership of the “electronic” commerce.

That is all fine. Today, we will simply note that ecommerce occurs when transactions are done online.

However, ecommerce is different from digital or online store in terms of business strategy or formation. That you have an online store does not mean that you run an ecommerce business.

When I say ecommerce business, for those that read my writing, I have in mind companies that do nothing but sell online as a business model. The essence of the business is facilitating trade and commerce online by bringing buyers and sellers together. It could be the seller or it could enable other sellers to participate in its ecosystem to reach buyers. Amazon.com, Alibaba (a marketplace ecommerce), Konga and Jumia are all ecommerce companies. Largely, except Alibaba, most of these noted examples are hybrid ecommerce firms: they combine the pure ecommerce business with the marketplace ecommerce business. In the pure ecommerce, the company keeps inventory and sells directly to buyers. In the marketplace version, the company does not own any inventory, it merely links sellers and buyers in its portal, acting as an intermediary.

When you have a website and have a small online store on the website, I do not consider that an ecommerce business. I see that as a digital store to help you expand your distribution channels. What I write does not apply to you. Your business is not ecommerce. Rather, you are using the Internet as a tool to grow your business. An ecommerce business is living on the web and that is all it does. If Internet stops working, the business will collapse.

Let me make it clearer with an example. A soap company with a website where people can buy soap is not an ecommerce company. You simply have an online store. The fundamental challenges of ecommerce do not apply wholly to you.

Distrust: Rich Africans have yet to embrace online shopping, due to online fraud.

Cost of broadband

Logistics

African open market: In Africa, there are “markets” everywhere, starting with the security guards who run stores in front of their masters’ mansions.

Fragmented markets: For all the efforts to make Africa appear as one market, it is not.

Literacy rates: Even if all the infrastructure and integration issues are fixed, illiterate citizens may be unable to participate directly on e-commerce sites that require reading and writing skills.

The Core Difference

A company online store has largely few products, mainly owned or marketed by the company, while an ecommerce company has expansive list of products, in hundreds, and usually not produced by it. Sure, like Amazon, the company can produce some of the products under its labels. However, the key difference is clear. In company digital store, you have few products made/marketed largely by one firm or few while in an ecommerce firm, you have multiple brands available. If government bans internet in that country, the ecommerce company will fold, while the company in this example can still operate, except that its online store will be gone.

Recommendation

Please go and add digital stores in your companies. Online stores will help grow your business. That website you are paying for domain hosting and renewal can bring more revenue if there is a store there. Everything you read about ecommerce does not apply to you. I want to make it very clear. You need a digital store – no argument on that. Your online company store is not the same as ecommerce. While you sell your products online, you business is not selling things online as the sole living mechanism. A lawyer that asks people to pay for consultancy fees online is not running an ecommerce company, and all the challenges affecting ecommerce should not concern that person.

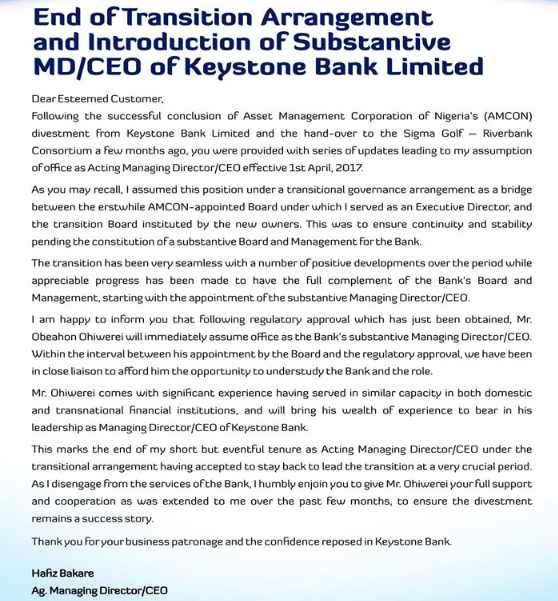

Obeahon Ohiwerei is the new MD/CEO of Keystone Bank Ltd, Nigeria. He takes over from the acting MD/CEO Hafiz Bakare. This is his profile

Mr Obeahon Ohiwerei holds a first degree in Mathematics and a Masters Degree in Business Administration. He began his professional banking career with Guaranty Trust Bank Plc in 1991, and his exceptional performance saw him rise to the position of Manager within six years. After a successful career with GTBank, he worked with Standard Trust Bank (now UBA Plc) where he was appointed the Pioneer Group Head, Consumer Banking in 1998.

He resigned in 2002 as General Manager in charge of Lagos and West to join Pacific Bank Limited (then on Central Bank of Nigeria’s holding action) as Managing Director. He repositioned the bank with his new team within 15 months and moved on to take up a new appointment as the pioneer Managing Director of Standard Trust Bank Ghana (now UBA Ghana).

He was a Group Executive Director with Access Bank Plc for 7 years, and a Director in 3 of Access Bank’s offshore subsidiaries as well as FITC, Lagos.