If you count the number of times you find the word “disruption” within a sentence containing “fintech in Africa”, you will think that disruption is a lottery number, to join the elusive African middle class. The conversation centers on mPesa, the Kenya’s mobile money transfer ecosystem, and how it has redesigned Kenya’s economic architecture. Quickly, just like that, everyone is extrapolating that Africa will experience the same.

This is an illusion: It will take a really long time for fintech to disrupt most African economies. However, fintech can provide sustaining innovation in Africa.

A Disruptive innovation is one that changes the basis of competition in an industry – for example in watches, Swatch change the basis of competition from accuracy to fashion. A sustaining innovation is one that perpetuates the current dimensions of performance – for example, Intel developing faster and faster chip speed.

In Africa, the fintechs are innovating, but they are not disruptive, across most of the markets. That you make it easier to send money in 24 hours, instead of 48 hours, does not mean you are disruptive. That you can make it easier to receive payments via better websites over what the banks offer is not disruptive; you are simply improving the process.

The Kenya mPesa Case

Kenya is unique because mPesa was actually a disruptive product. It drastically offered a new way of moving money, not improving how it was done hitherto. mPesa did not work to reduce the time to move money from one bank in Kenya to another; it offered an entirely new concept, through mobile devices. It changed the basis of competition. It worked, because the banks did not anticipate that. I call mPesa a perception product which offered value beyond needs and expectations of Kenyan citizens.

But what happened was as soon as mPesa changed Kenya, most African banks redesigned their business processes. They were ready to chip out most of the values mPesa offered to Kenyan citizens which the banks, then, did not anticipate. So, if you try mPesa in South Africa, it would be a wasteful endeavor because South African banks had already advanced beyond the perceived values of mPesa. Or better, the economic structure of South Africa was well advanced for mPesa to add much value. Simply, mPesa failed in South Africa.

Mobile phone usage is high – nine in 10 South Africans own a mobile phone – and a third of these are smartphones, according to figures from the Pew Research Center. Yet South Africa has the most technologically advanced, financially liquid and accessible banking system on the continent.

Why Mobile Money Failed in Nigeria

Besides trust, which is a huge challenge in Digital Nigeria, the Nigerian banking sector, for those that have money, works. There is nothing mPesa offers that you cannot do on mobile apps and web apps. You can move money instantly in bank branches and send money to people via ATM instantly. As you chip out these benefits, the construct of mobile money does not make much sense to many people. People are fearful of Yahoo boys and lumping phones and money may not appeal to most of the citizens, irrespective of the promises you can make on your technology. Most of the pioneers of money money have seen pivoted, because the market did not welcome them.

CBN Governor Godwin Emefiele

Sure – mobile money could have worked. The problem was that mobile money came when banks had already provided substitutes for most of the values, it could have offered. Mobile money will surely benefit the poor and under-banked, but in Nigeria, those people are the least to trust that their bank accounts will be in the phones. The pillow with a loaded dane gun is a better option despite promises by the Central Bank and partners.

Sustaining Nigeria’s Financial Order

There is no firm that will kick the banks out of business soon – not even close. Sure – they will chip out some revenues, which must concern the banks. But at the end, the banks will be fine. The problem is that anything anyone introduces now can be quickly replicated by the banks, because you are “innovating” within the economic structures which enable present banking institution to function. They own the game and can define the future. That is why you cannot be disruptive.

But you can get your sustaining innovation by improving speed, efficiency and many other things to win some customers from them, but the system in Nigeria is one you cannot destabilize them.

The fintech startups are not working to extend service beyond those within the banking sector already. This means, they are fitting into the banking order. The under-banked and poorly served are not part of the equations. mPesa solved that problem, in Kenya, but the Nigerian fintechs are not thinking about that. Simply, they cannot disrupt GTBank, UBA, and all these great institutions by “plugging into their systems”. It will not happen.

The herdsmen who move tens of cows have more values to a bank than college students who barely have enough for three square meals. But the college students are accessible while the herdsmen are not. Find a way to reach them and provide banking services and boost your revenue.

Agency banking with proprietary technology supported with tokens, phones, BVN and mobile kiosks will deliver the magic. The transactions will be capped to avoid fraud and risk-management tools embedded. As these agency banking systems mature, banks can close and sell off expensive branches which may not be necessary in 5 years as the immersive digital economy evolves.

Disrupting Banking in Nigeria

You will notice that I have equated financial sector with banking sector. That is by purpose because we do not really have an insurance sector. So there is no need wasting space including insurance. For any fintech to disrupt the banking sector, that fintech has to build an entirely new architecture that is totally different from what we have today: a new basis of competition is a requirement.

The trade by barter was disruptive because cash offered an entirely different system where you do not need to “find” or know a person to exchange goods and services. You can have a stranger pay with cash unlike looking for a neighbor interested in your goods to exchange by barter. That was disruptive, a new path was created.

In Nigerian banking, someone can create a system where the under-banked citizens may not have to do anything with banks to do banking. Once that is done, you can systematically chip out the people in the banking system. Over time, the banks will know what has fallen them. But right now, what is happening is that fintechs are starting with what the banks are doing and that cannot disrupt them.

Rounding Up

Disruption requires the change of the basis of competition. It is like digital cameras to film cameras (think Kodak). The digital cameras did not even care if there was anything like film in the world: it pioneered a new path. Google disrupted the physical directory business by creating an alternative path without making better papers. When Amazon took down the bookshops, it did not build better bookshops, it changed the basis of competition – digital purchase. For the fintech to take down and disrupt Nigerian banks, they must change the basis of competition. At the moment, they are sustaining innovators which are fortunate the incumbents are not doing what they are doing.

In this piece, I explain the Aggregation Construct using many case studies. Two Nigerian startups OgaVenue, event venue marketplace, and Printivo, digital printing, firms are included.

Under the aggregation construct, the companies that control the value are not usually the ones that created them. Google News and Facebook control news distribution in Nigeria than Guardian, ThisDay and others. Because the MNCs tech firms “own” the audience and the customers, the advertisers focus on them, hoping to reach the readers through them. Just like that, the news creators have been systematically sidelined as they earn lesser and lesser from their works. But the aggregators like Facebook and Google smile to the bank. The reason why this happens is because of the abundance which Internet makes possible. Everyone has access to more users but that does not correlate to more revenue because the money goes to people that can help simplify the experiences to the users who will not prefer to be visiting all the news site to get any information they want. They go to Google and search and then Google takes them to the website in Nigeria with the information. Advertisers understand the value created is now with Google which simplifies that process.

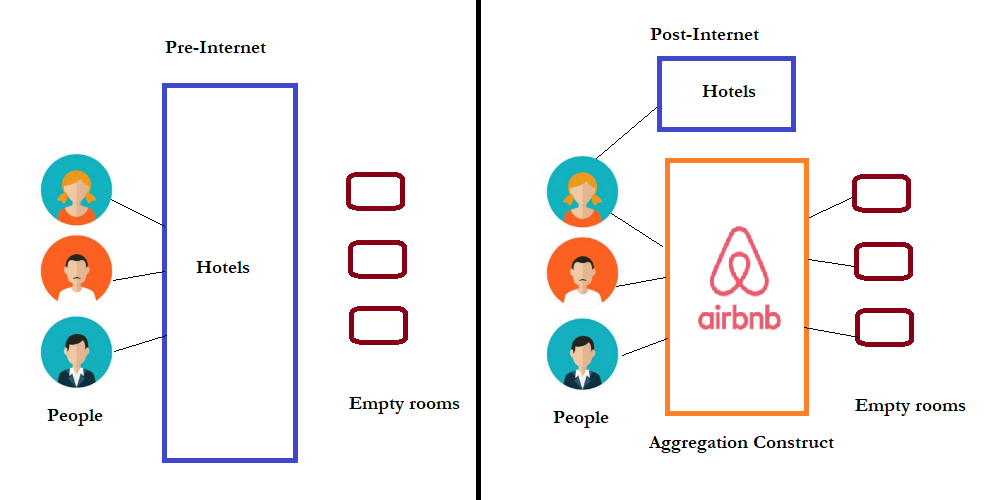

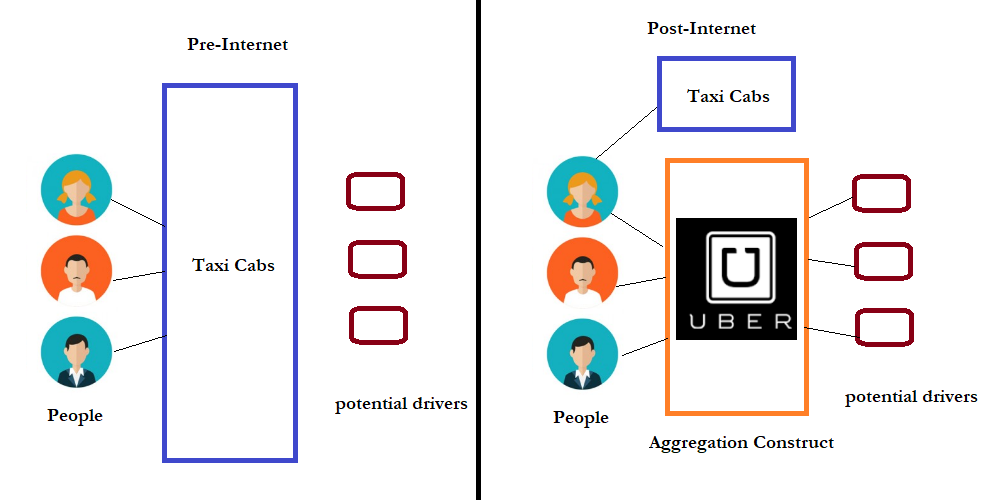

Airbnb and Uber are discussed; they respectively aggregate available temporary accommodations and taxi services, at scale, while necessarily not creating them.

Author’s Note: This piece has generated so much confusion; I am adding this section to summarize the thesis. The focus of this piece is not that Internet destroys all value, but rather that it destroys taxable revenue value in the SHORT-TERM, for those not creating the companies destroying the value. For government, that is a challenge.

If a call from Lagos to Boston is $20. And using Skype, you can make that call for free. Ok, I give you $2 since you have to pay MTN for broadband access. Simply, $18 has been (effectively) destroyed and Nigeria cannot recover that. While Skype can make $1 through adverts while you are there, Internet has destroyed at least $17. Consumers enjoy, but govt and non-digital firms will struggle. This applies across sectors. Internet will destroy massive value as it permeates across industrial sectors. That value is not transferred to the firms destroying them. Skype does not get the whole $17 destroyed from MTN. My point here is that Nigerian government has lost the capacity to tax that $17. In the short-term, it is a problem and that is what I am trying to pass across.

This does not mean that customers have not benefited. Please note that it is possible the savings of $17 by the customers can create $30 in future. Sure, but that is FUTURE; in the short-term, government has to deal with loss of that tax Naira. That is the future. I am focusing on the short-term.

Case Study I: NITDA gets 1% of all profits from Telcos. MTN has been the most reliable to NITDA as it makes profit. But MTN declared loss last year owing to the huge fine it paid. Others like Etisalat (9Mobile), Glo, and Airtel rarely pay or pay very little, because they rarely make much. For NITDA, in the short-term, it has to look for other ways to fund its activities. Had Airtel, ET and Glo made money, NITDA would be fine. Sure, customers enjoyed their Skype and WhatsApp, but the government agency gets its zero revenue.

Case Study II: In U.S., as Amazon.com expands its e-commerce empire, many U.S. cities are seeing the devastating impacts on their real estate taxes as physical stores close. With the real estate taxes gone, some cities are closing libraries, schools etc because they do not have the funds to run them. This supports my notion: those cities did not anticipate what Amazon’s business could have on their tax revenues. This does not mean they are not benefiting from the cheap books they can buy on Amazon. They could be happy as consumers, but for the local governments, there is no money in the bank.

This does not mean that this is all bad, in general. It is creative destruction. I just want us to have a conversation on this from the taxation angle. Government cannot afford to wake up and see empty treasury because banks, telcos etc have seen the erosion of value while the ones destroying them are not compensating for same. Now, read the piece…

Internet is one of the greatest technologies ever invented. It reduces friction in the business processes, enabling a better inter-relationship among nations, firms and citizens. From the private sector to the public sector, Internet has radically changed our world. Many industries are re-structured as a result of new business processes which Internet is enabling.

But behind all these exciting things about the Internet, Internet will destroy value in Africa, even though it will create value in some areas, over time. In the short time, Internet economy will cause challenges to most African economies as their companies experience erosion of value and associated tax receipts.

It will be all well, because the net impact of Internet, will be positive. The citizens will benefits but companies and nations will have to adjust in order to also benefit. Over the long-term everyone will benefit, but in the short-term, there will be severe challenges.

Africa does not create many technologies, which means the value created, at the share capital side, will not benefit us. Of course, we will benefit as consumers. However, our traditional companies will struggle, because their values will be destroyed. If we do not build enough competitive digital companies to compensate, very fast, we may be in real problems.

The Internet Value Destruction

Internet creates value but Internet also destroys value. For all the money Amazon.com has made for its shareholders, many bookshops are gone. For all the simplified lifestyles Google has made possible for all of us, many directory companies have gone bankrupt. That is a good thing, as the users or consumers are benefiting. But that does not mean that governments, especially those without these big companies in their domains, will not struggle. Those governments will lose tax receipts, over time. The following explains how Internet destroys value

Diminishing Abundance: Internet is a global village. It brings the constructs of abundance. Simply, it commoditizes everything within it. Before Internet, this blog and New York Times have equal rights. When a material is posted on the Internet, that material is available globally. This means that Internet offers abundance in anything which can be available online. The implication is that those that make money through controlled scarcity of goods and services will struggle. (Think regional newspapers.) Also, because of the global pool, the challenge to be the best to compete becomes critical. A Lagos graphics designer does not have any special advantage compared to a man in Pakistan who can offer the same service via UpWork. What happens is that competition heats up, globally, and everyone has to reduce price. When that happens, the global regions with the best talent win. For the Nigerian case, if the job goes to the guy in Pakistan, Nigerian government has lost the tax associated with that revenue. The risk for Nigeria is huge, if it cannot produce enough people that can bring the jobs to Nigeria, to avoid net negative in this cross-border commerce which Internet enables.

Aggregation Construct: Under the aggregation construct, the companies that control the value are not usually the ones that created them. Google News and Facebook control news distribution in Nigeria than Guardian, ThisDay and others. Because the MNCs tech firms “own” the audience and customers, the advertises focus on them, hoping to reach the readers through them. Just like that, the news creators have been systematically sidelined as they earn lesser and lesser from their works. But the aggregators like Facebook and Google smile to the bank. The reason why this happens is because of the abundance which Internet makes possible. Everyone has access to more users but that does not correlate to more revenue because the money goes to people that can help simplify the experiences to the users who will not prefer to be visiting all the news site to get any information they want. They go to Google and search and then Google takes them to the website in Nigeria with the information. Advertisers understand the value created is now with Google which simplifies that process. Google does not pay tax to Nigeria (sure the small Google Nigeria may do, but get the idea, we are talking of real tax here), but it does depress earnings for Nigerian companies. The news production is now commoditized. This affects the total tax government can collect from these companies.

Marginal cost: In a perfect market, the marginal cost of a digital product is zero. This means the price of a digital product tends to zero: welcome freemium and ad-supported business. However, only firms with network effects dominate, making it hard for Nigerian government to benefit, via tax, as we do not have those companies.

In this piece, I explain why it is very hard to monetize digital products in Nigeria and indeed Africa. The core reason is that in a perfect market, the marginal cost of producing digital product is zero. This implies that its pricing will inevitably go to zero. This is the heart of the freemium model where you get many things free, which is possible because of the aggregation construct, where companies provide those digital products and then create an ecosystem to sell adverts. They benefit more than the suppliers by providing the platforms. As noted in the plot, great companies deliver the $0 marginal price even at high value, making it challenging for anyone that carries a non-zero marginal cost to compete, exacerbated if the product is even not top-grade.

Case Studies

I will use four companies in four different sectors to explain how this new digital economy will erode and destroy value in Nigeria, and also how Nigerian government will lose tax receipts. This is not really all bad, we just have to understand the short-term challenges and work to mitigate them.

MTN (Telecommunication): MTN is a leading telecommunication company in Nigeria which sells voice telephony and broadband services to the large spectrum of the Nigerian market. MTN will lose value through the OTT (over the top) services like Skype, WhatsApp and WeChat. These are solutions that ride on telecom infrastructure with only a small part of that revenue going to the telecom firms. Most of the value is destroyed, the OTT firms do not absorb or get most of the value. For example, without Skype, one can make a minutes-long call from Nigeria to New York via MTN service for $20. That money is paid to MTN which pays the Nigerian government tax, accordingly. Government benefits. However, with Skype, the money that goes to MTN may be $2 (the person still needs MTN service to be online to use Skype). The $18 is totally destroyed as Skype has not converted it to itself. That is how Internet destroys value. It has caused Nigerian government to lose tax on the $18 even though Skype did not get that money. Skype, owned by Microsoft does sell adverts but that call could not have generated $18 for Microsoft via ads (it is possible it will be less than $1)

P&G (Consumer Packaged Groups): P&G does many things to get its products to our homes in Nigeria. It invests in R&D to engineer the products. After that, it puts money in branding and advertisement. Then, it works with supermarkets/shops/etc to help stock the items as part of its distribution and retailing. Value is created along the line for Nigerian government. Tax is paid and money is made. But imagine a situation where say Konga can import one of the products (say razor or shaving stick) from another country and sell it directly to the Nigerian people. The value especially at the R&D will be destroyed because Internet has made it possible to use another country, entirely, and still sell directly to Nigerians, without distributors. A good example is the Dollar Shave Club in U.S. which used Internet to deliver a service which is far cheaper to what P&G Gillette give to men on shaving. Dollar Shave Club is far cheaper and takes away most of the perceived value P&G thinks it creates on shaving products. Before Internet, Konga can still import say shaving stick, but the ease of selling that via online will push pressure on what P&G can command with its expensive high-value product. The e-commerce company and cloud computing which makes it possible provide disintermediation which erodes value for P&G and which ends up hurting Nigeria with the traditional value chain cannibalized. The new one created will not create as much tax value.

Wema Bank (Banking): Wema Bank runs treasury business which helps it do many things including money transfer. It earns huge amount of money in the process and pays tax on the fees to the Nigerian government. But with fintechs like Paystack and Flutterwave, value will be destroyed on the whole remittance/money transfer sector. These startups will do the transfer more affordably thereby destroying the value for Wema Bank, as trying to match them will result to lower fees from Wema Bank. This is not really a bad thing for the user, but for government, it is not a smiling matter, because the low-cost fees will mean low tax Naira.

Guardian (Media/Publishing): Guardian sells advertising to the Nigerian suppliers, earning good revenue. Today, some of those ads are moving online. While Guardian will continue to compete online, the bulk of the ad Naira is going to the aggregators like Facebook and Google. Guardian online is largely commoditized, as it has to compete with this blog for revenue from Google Adsense which is runs. For Guardian to be in the same network with this blog is a bad thing. Traditionally, it ought to have the capacity to sell all its available ad spaces. But this is what Internet does well – it respects no one. The point is that Google ad revenue will drop and the Nigerian government will have less revenue to tax.

Implications

Nigeria is not paying attention to the potential risks of value destruction to the economy which Internet will bring to the nation. We will continue to see the erosion of tax Naira as more industries are disrupted. The telcos are first, but our banks are not immune. If the banks face this problem and fail to compete, the tax Naira will go as more value will be destroyed.. The challenge is that value is destroyed, and our local digital companies do not actually drive the destroying process – most times, foreign firms do and get the value. I project that Internet will erode more than 17% of Nigeria’s total tax revenue over the next decade. This does not mean that the absolute tax revenue will drop, rather, some sectors where government makes money, via tax, will earn less. If the telcos earn less because of OTT, they will pay lesser tax. Period. But government can still get more artisans and farmers to pay tax (I want to make that clear – my prediction is not the absolute tax which can be compensated if more people join the tax paying base. I am focusing on taxes from those paying tax right now. While those paying now can drop, proportional to growth, the total absolute tax could be higher because of bringing more informal sector participants into formal sector).

Our digital companies are supposed to help us cushion the impact from this Internet-enabled value destruction. Yes, but they will need to grow and blossom first. I will explain how they can do this.

What Nigeria Can Do

Simply, Nigeria has to pay attention to its capacity to build these companies of the future. The efforts by the Bank of Industry to fund largely asset-driven companies must be revisited to include digital businesses. There is no apparatus for most DFIs (development finance institutions) like Bank of Industry and Bank of Agriculture in Nigeria to support digital companies. Government could even do better: offer free tax to Venture Capital firms for 10 years to enable them come and help us build the businesses of the future.

It is very hard to setup a technology startup, in Africa. One reason is the dearth of investors with capacities to make visions become realities. Across most African cities, technology-enabled entrepreneurs continue to struggle, without capital to scale. They look for investors, they rarely find them.

It is well established that some of the richest men in Africa did not make money through technology. The implication is that most do not understand that sector. So, they are cautious to put money in areas they do not have good domain expertise. You do not blame them – they cannot play chess games with their resources.

Nigerian moment is now to plan because Internet will redesign our economy.

Update: There is a brilliant suggestion in LinkedIn on what Nigeria can do. I am adding same below with the full comment.

Governments use taxes to scale up social amenities – corruption aside, that’s what taxes do for us. With declining oil revenues and lower than expected revenue e.g. from telcos courtesy internet bases innovations Governments will fail to keep up and the masses will suffer poor roads, intensified power outages, poorer healthcare and more. I postulate that the value the internet based innovations give us may be ripped away via declining amenities. Hence Government has to wake up to this reality – a forward looking cabinet should have a committee working on this for the sake of the people. What good is lower call costs when higher transportation and diesel for gensets wipe it away? ndubuisi ekekwe is talking solutions and here are my thoughts in addition to his.

1. Widen the tax bracket – all should contribute for the common good.

2. Remove/lower any tax holiday in industries that don’t fit that core national agenda and where the benefits don’t trickle down to the masses.

3. Shore up the FIRS – go digital, hire smart graduates/poach from the private sector, train them to death, develop a tax strategy and flog the process into efficacy levels never seen before.

4. Offer tax amnesty so arrears are paid and non conformer are on the books.

5. Start a tech revolution in our education system so in the medium to long term our own companies will reap maximum value in Nigeria.

6. Woo big tech companies to set up in country so they pay tax here (hard I know but worth trying after all we have the clout)

7. Fund collaboration incubators to facilitate birth & growth of big Naija tech firms who will offer alternatives (Made in Naija apps) & who will pay taxes here. Enough before I go off point. We just need to redesign how things work to win as a country.

Rounding Up

Internet provides many benefits but we must not lose the sight that Internet will destroy value in the short-term in Nigeria, before it creates it. Government needs to model these challenges and ensure that we have the capacity to overcome them. Investing to be creators of the future will be strategic for Nigeria. Our digital economy must have local content and participation for us to benefit from what Internet promises. If not, Nigeria will experience the most consequential moments in its history with decreasing crude oil revenue and erosion of tax base. That is called double whammy.

I run a Practice in Fasmicro Group through which we help clients redesign their organizations, via technology. My work helps clients make technology work for them, We ensure that IT not just run your organization, but also transforms it. I work, usually, at the level of senior IT leadership, Executive Management, and Board, on technology-driven strategy, in Africa, and beyond, across different sectors. Our clients include leading African banks, governments, insurers, and more. Below is a synthesis of some of the things we will help you handle.

IT Strategy: Conduct a review of the Firm’s current IT strategy, and identify the current gaps considering the business needs and market best practices and make recommendations to implement the strategic gaps with fit for purpose solutions in line with Global Best practices and local realities

IT Governance: Conduct a review of the current IT Governance practices in all areas in line with International and Local Regulatory standards like COBIT and identify the gaps in implementation/Compliance to standards. Recommend the necessary detailed steps to align with the International standards. Review the IT Organogram for HQ and at Country level and recommend an Effective Governance Framework to effectively manage the HQ and Country technology Organizations interface

IT Skill Capabilities: Conduct an IT capability and competency mapping of key IT Tasks/roles against available skills in the Firm and make recommendations where there are shortages or excess capacities. This should be done using acceptable frameworks like Skills Framework for the Information Age (SFIA). Establish how to appropriately deploy the human resources to have an agile IT Organization. Produce a framework that will help the Firm to develop and retain the core IT skills required by the Firm. Recommend a Robust Outsourcing strategy and in key areas to complement inhouse skills and a governance framework to manage the Outsourced Vendors.

IT Value Realisation: Conduct a detailed Benefits Realisation assessment of the Firm’s Key IT investments in Software and Hardware Projects. Make specific recommendations on how to measure Benefit/value realised from IT and identify and recommend the Key Levers for Value Realisation of the Existing IT investments. Develop a framework for the establishment of IT Value realisation practices for future projects and investments.

IT Projects: Conduct an assessment of all IT Projects in the Firm during the last three years. Determine how many of them were delivered on time, how many are still ongoing, how many are failed, etc. Identify the Strategic reasons for their failures and recommendation for successful execution of projects. Make recommendations on how to better handle ongoing IT projects and develop an enterprise project management and governance framework for managing the Firm’s IT projects in a cost effective and timely manner.

IT Process Documentation and Performance Management: Conduct a review of all IT and Cross Functional process in the Firm against available documentations and make recommendations. Identify the key gaps in the processes leading to failures in IT Operations service delivery. Assist to align the IT processes with specific business processes and produce a report showing the mappings of IT process against business processes. Create Standard templates for the creation of Standard Operating Procedures (SOP) for IT Processes. Identify the Key Vital Performance Metrics which IT operations should monitor to manage the service delivery and operations of IT. Identify the Specific and Measurable Key Leading and Lagging Indicators KPIs for all the units in IT organization.

IT Processes Documentation:Document the Firm’s IT processes to improve change/succession management, build IT knowledge base and institutionalize the Firm’s processes by making them individual-agnostic.

Center of Excellence: Assist the IT Organization to develop and implement a framework for the development of the Centre of Excellence (CoE) concept within the IT Organisation in the Key Domains consisting of best practices standards in Solution Delivery, Governance, Service Management, Project Management, Data Centre Practices, etc. Develop a CoE Maturity framework. Assess the current state and identify the gaps and benchmarks required to move towards Journey of Excellence.

Digital Products: Review the performance of the technology-enabled products against the uptake and value realized. Review the products/channels to recommend infrastructural and other changes needed to generate desired traffics for the products.

IT Spend: Review the IT spend for last 3 years and provide strategic assessment of the Firm’s IT cost structures compared to global and Local benchmarks. Recommend Value add IT cost reduction approach that provides a competitive edge to business while reducing overall costs.

Data Consolidation: Develop data governance and framework for the Firm to enable efficient management of the Firm’s data and ensure data is robust, accurate and reliable. Design and execute the Firm’s data consolidation plan.

I lead my team and we handle engagements with absolute commitment to quality. Our clients receive the highest level of value. Our pricing is industry-competitive.

If you would like a conversation on our service, please drop a line to info@fasmicrogroup.com or nekekwe1@jhu.edu

I study two men – Franklin Templeton and Carlos Slim – for my family investment strategies. Templeton began a firm in 1947, against all odds, at the ruins of World War II. Mr Slim bought anything in his sight at one of the lowest points in Mexican history – the peso was down and markets in ruins. Templeton trusted the human race and bought “useless” stocks. Slim’s father told him that countries do not fail; they always come back. I read about these two.

At the lowest point in Nigerian stock market, I deployed Slim’s message. I loaded believing the Nigerian people. I trusted my fellow citizens will figure out Nigeria and no matter what, markets will rise again. With all the noise in Nigeria, some did not know in that last 18 – 24 months, one bank stock had returned 4X .

Becoming successful in life is not about being busy – it is understanding things and making sense of them, more meaningfully. There are acres of diamond in Nigeria today, across many areas. Look for them. If you do not believe in humans and nations, it is unlikely you can see opportunities in life.