The CEO and CFO of Etisalat Nigeria, Matthew Willsher and Olawole Obasunloye, respectively have resigned.

This is coming some days after the resignation of the Chairman, Hakeem Bello-Osagie and some Mubadala directors of the United Arab Emirate (UAE) firm.

A new board has been constituted. The new board appointments are: Dr. Joseph Nnanna (CBN), Mr. Oluseyi Bickersteth (KPMG), Mr. Ken Igbokwe (PWC), Mr. Boye Olusanya (former DMD of Celtel) and Mrs. Funke Ighodaro (former CFO, Tiger Brands)

Their resignations came on the heels of the protracted loan impasse of the $1.2 billion the telecommunications firm is owing a consortium of 13 banks, which has subsequently led to the pull out of the parent body and major investor, the Mubadala Group.

The role of the Chief Product Officer has become popular over the last few years, especially in technology-enabled startups. Few people can hold this title and fewer people should even be responsible for the duties. In the time of change, and organisation continuity redesign, founders are the best positioned to lead product development and evolution.

Chief product officer (CPO), sometimes designated as chief production officer, is a corporate title referring to an executive responsible for various product-related activities in an organization (Wikipedia)

As we saw in Twitter when they had product problems, they brought back Jack Dorsey. In IROKO, when the radio business had some issues, Jason Njoku took over. In both cases, the founders became custodians of businesses they helped to create.

Founders bring vision, authority and trust necessary to change things when they are necessary. In this video, I explain why the best chief product officers are founders and if a founder cannot do that job, the startup should simply close the door.

It is very hard to setup a technology startup, in Africa. One reason is the dearth of investors with capacities to make visions become realities. Across most African cities, technology-enabled entrepreneurs continue to struggle, without capital to scale. They look for investors, they rarely find them.

It is well established that some of the richest men in Africa did not make money through technology. The implication is that most do not understand that sector. So, they are cautious to put money in areas they do not have good domain expertise. You do not blame them – they cannot play chess games with their resources.

There is also the fact, in some countries like Nigeria where some politicians and ex-military men are extremely rich, but yet fearful to invest in companies, because they could be asked to show the sources of their funds. (One evidence against Olisa Metuh, former PDP spokesman, in his trial, was an investment.) To avoid that beaming of high voltage searchlight in their lives, they simply “bury” the money in their yards or build houses no one can afford to rent.

So without much support from home, African entrepreneurs begin the journey of looking for capital in North America and Western Europe. After all, they do read how companies have raised capital and they are certain, they have got great business plans to compete. Unfortunately, informally, 99% fail because at that level, there is really nothing to invest in. from the angle of the investors.

Nature of Global Venture Capital

One of the most challenging sectors in the world is the VC sector.It looks easy from the outside – get money from rich people, distribute same through investments to smart people building companies. Then follow-up and then wait for the value to be created. Sooner or later, everyone is rich! It is largely a sweet world, except that is not really what happens.

The VC industry is merciless. Most doing it fails miserably. And that makes them so fearful to invest in unknown entities or markets like Africa, with no largely demonstrated records of generating huge value.

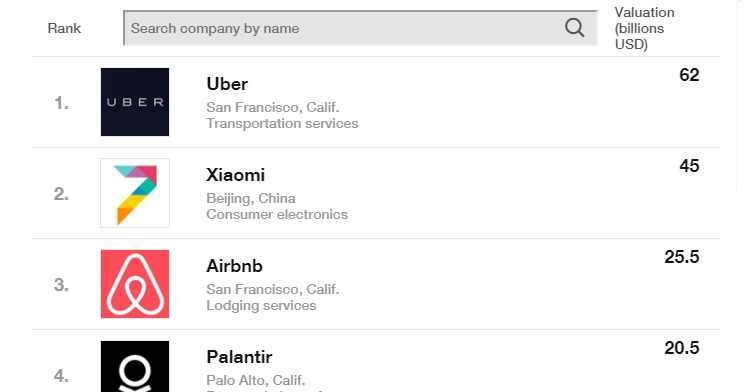

If you visit the Fortune Magazine’s The Unicorns List, you can see a very interesting trend – nothing of huge interest happens outside of the top 20 companies; the top 20 unicorns account for more than 50% of the entire list of 121 companies. (A unicorn is a tech-enabled private company with a valuation of at least $1 billion.)The top five or so (Uber, Xiamio, Airbnb, Palantir, Didi Kuadi) take more than 20% of the entire list.(I removed Snap which had since gone public in the list). In other words, the value in most private companies are concentrated in the top 20. Though I have focused on using the Fortune unicorn list which tracks technology private companies with valuations of at least $1 billion, the trajectory is correct because that list is global.

Some unicorns in Fortune Unicorns List

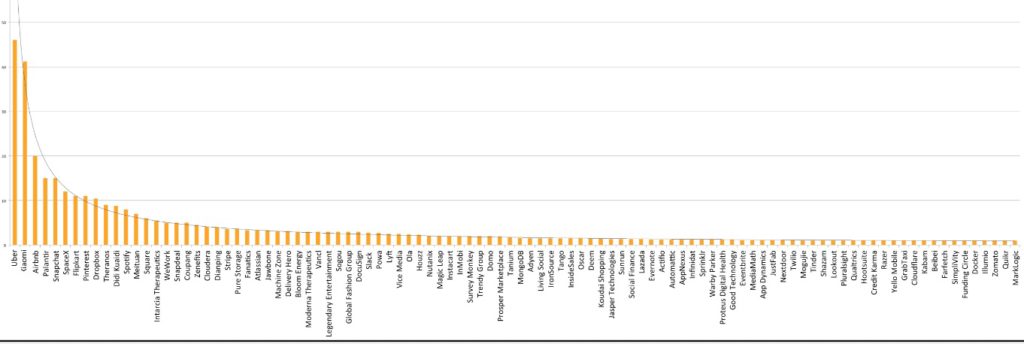

A power curve of the whole 121 unicorns shows that is concentrated at the top 20

If you take those valuations into a power curve, the trend becomes more visible, as noted in the plot above.. So, anyone that is outside the top 20, as an elite VC, is not doing well. Since a VC will not likely invest in all of them, the play is to make sure that it is in one. They have this feeling that they do not want to miss out, so all efforts are concentrated at the top, because that is where the value is created.

Uber’s valuation is largely the same as the GDP of Kenya.. This means that you cannot necessarily be having Uber in Kenya. (Sure, this statement can be challenged since Uber is asset-light and can be born in Kenya. Yet, even if Uber was made in Kenya, they could have considerred the size of the home market in its valuation.) But the fact is: while will an elite VC pursue opportunities in Kenya, if it can get into top companies like Uber, where that is possible? With these mindsets, they can take Africa as a secondary market which becomes like a backup when the sources of great returns, usually in America, are out of reach.

Besides, most times, it is winner-takes-all. Most times the unicorns dominate their areas and domains. Once they have taken control, no one around the world and especially Africa will be of relevance in that category. It is that mindset that makes it challenging to breakthrough when you want to raise money from foreign investors. By the network effect in most technology areas, the number of potentially great companies are limited. You have few great ones and then all-rans because one, the category-king, the winner, had locked the value, in a category.

The African Challenge

We have a really challenging issue because top VCs have the methodologies to win big or lose big. The greatest VCs lose, most times, the most money, but they also win BIG. That winning big compensates for all the misses. For example, you can invest $10 million and lose it but another $10 million investment can turn into $500 million. An average VC will not bet like that, being so cautions not to lose that $10 million. However, it rarely has the opportunity to make that $500 million, also. Owing to this scenario, what matters is the market size. If they do not see how the size of the market can justify that winning big, they do not show interests. It simply means, win, they lose, and loss, they lose, since even what you may think is winning may not be enough for them. Owing to that, they show no interest to business plans addressing small markets or market segments.

So, what happens – you are now left with lower tier VCs who cannot get into the left-hand side of the power curve where the game is played and where most of the value is created. Unfortunately, those lower tier VCs are extremely cautions – they hate to miss a strike. That is their inherent characteristics. The implication is that they waste your time, and at the end, you get the message that they cannot invest.

The market makers that hit big and lose big need to show interests for us to get our moments. Until we get their attentions, the struggle will continue. We need people who can take risks, not overly cautious investors that largely add marginal value, who always want you to be post-revenue, when it is obvious you cannot execute without capital.

Making Them To Come

I do think governments across Africa must offer tax-holiday on VC capital over ten years to get them interested in Africa. We need to offer something to unlock capital so that we can build our future companies. The money invested will not be taxed along with the proceeds from exits. If we do so, Africa will see massive growth in the VC sector.

Rounding Up

Africa will continue to struggle in attracting investments in technology-enabled companies until we can attract a new category of investors that really want to win big. At the moment, we are getting attention of over-cautious investors who are not necessarily the elite. The elites play hard and also win or fail hard. They make category-kings possible because they invest in things most have never invested on. In other words, they know how to take risks. They do not over analyse scenarios and run due diligence for months, hoping during that time, you might have magically succeeded only for them to join the party. People like Peter Thiel, Andreessen Horowitz and John Doerr are desperately needed to show interests in Africa. They are people that can catalyze the local entrepreneurs to take more risks and also unlock the untapped opportunities in Africa by giving them resources. Without such investors, African will continue to struggle in scaling great ideas in our continent. I recommend for African Union to lead a 10 year tax-holiday on VC capital and associated proceeds in Africa.

South Africa is going through an economic redesign. The mining sector is seeing new changes. Over the last few years, more than 70,000 jobs have been lost in the mining industry. Thirty years ago, mining accounted for 20% of the country’s economy.Today, it is about 7.3%.

But beneath these challenges, South Africans are changing their countries. Services are up and they are leading Africa with great companies like Stanbic Bank, DSTv, MTN and Shoprite. They innovate, ferociously. Owing largely to better infrastructures, e-commerce is one area South African companies are finding values.

Few years ago, I wrote in the Harvard Business Review on the challenges of e-commerce in Africa. In that piece, I mentioned the struggle of one of South African companies, Kalahari, which had largely pioneered e-commerce in Africa.

We were not alone. Old local giants like the e-commerce business Kalahari, the advertising firm InMobi, and e-classified site Mocality retrenched, reorganized, or closed down. In closing some of their e-commerce properties, Naspers, a media and internet empire, noted that it was a “sad day for e-commerce” in Africa and cited “unprofitability” as a reason.

The fact was Kalahari retrenched because it could not compete. But over the last few years, that company has redesigned itself to find ways to compete, at least in South Africa. The Naspers-owned digital company merged with another firm, Takealot. Takealot had started operations in 2011, after it bought Take2, through funding support of Tiger Global and Kim Reid. This strengthening has deepened Takealot capabilities, making it the biggest South African digital firms.

Naspers is Africa’s leading company and the most valued. It is traded in the Johannesburg Stock Exchange. The firm failed in its efforts on Kalahari. But then has been plotting how to win in the e-commerce market. It s common knowledge that e-commerce is a promising sector, in Africa.

One thing Naspers figured out was the need for scale in the business. And that was the strategy it had adopted. Naspers had since signed agreements to take controlling stake (53.6%) of Takealot, valued at $73 million, pending regulatory approvals.

In April 2017 the group signed an agreement to acquire a controlling stake in its associate Takealot Online (RF) Proprietary Limited (Takealot) for approximately R960m (US$73m). Following the investment, the group will consolidate Takealot as a subsidiary and will hold a fully diluted interest of 53.6%. The transaction is subject to

regulatory approval.

South Africa’s E-commerce Sector

With this new re-positing, Naspers suddenly becomes an important element in the e-commerce sector, in South Africa, overtaking Amazon and eBay.

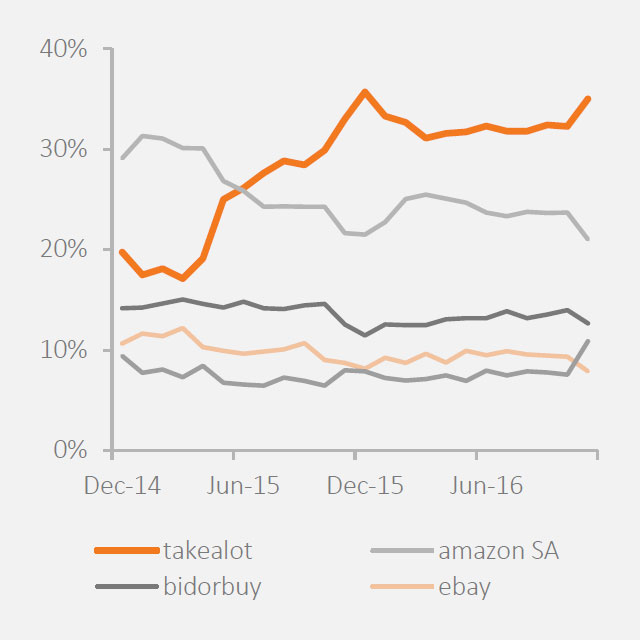

The investments and Takealot’s merging with Kalahari has made it the biggest eCommerce platform in South Africa. When Takealot was founded, its vision was to be the largest, simplest, most customer-centric online shopping destination in Africa. Naspers’ financial results show that Takealot has achieved its goal of being the largest online shopping destination in SA.It is much larger than its local competitor Bidorbuy, and is bigger than Amazon and eBay in South Africa.

The plot below presents the market share with Takealot doing far better than Amazon and eBay.

Source: Naspers, Broadband.co.za

Lessons for E-Commerce African Entrepreneurs

E-commerce is not an asset-light business. To do well, scale is very critical. The pockets of many e-commerce startups across Nigeria can do better, if they find ways, to come together. Nigerians do not like mergers and acquisitions as we do not like to own parts, we like to own 100%. But in a business like e-commerce, that is what is necessary.

The lesson is that Takealot can take up Amazon SA and others by coming together with Kalahari. This dominant position is what will give them opportunities to compete. Going it alone will be challenging because of some of the factors I noted in the HBR post (referred above).

Note that it is irrelevant that this is Amazon SA or eBay SA. The fact remains that it is Amazon or ebay. South Africa’s economy is largely matured and sizable enough to be a big U.S. state. So losing in South Africa means Amazon and eBay are losing in one strategic state in U.S. Should they decide to venture into Nigeria, banging together by pulling resources will provide the best opportunity to challenge them competitively. From Uber to legions of foreign competitors across African capitals, we lose because of fragmentation which denies us scale, to hold our turfs.

Rounding Up

I am looking for the day when Nigerian e-commerce entrepreneurs will come together instead of everyone becoming a CEO. That will help them pull ideas, resources, and energies together to get meaningful scale that will give them traction and success. As seen by Takealot strategy, scale is critical. Amazon or eBay or indeed any foreign brand, can be competitively defeated, in Africa.

Few days ago, I wrote about the massive latent opportunities for the telcos in Nigeria. In that piece, I explained that MTN, Glo, Etisalat and Airtel could build a new business in the agricultural sector, focusing on linking and connecting farms and farmers.

Yet, these companies have opportunities to unlock more value if they can move into certain new industries like agriculture. They need to move into providing services that help farmers improve their businesses and that will help them find new sources of revenue.

Today, I will like to discuss how they can execute this mission from a product evolution phase. I will propose they introduce a new currency which will help them manage the challenges which are inherent in an informal sector like Nigerian agriculture, without being tethered to the innovation-challenged Nigerian banking, which for generations have failed to provide services to millions of citizens, especially in rural communities.

But before we do that, let me refer you to a quote by the President of African Development Bank and former Agriculture Minister of Nigeria, Dr Akinwumi Adesina.

Dr Adesina made it clear that Agriculture is huge and it is indeed the biggest money making sector in Africa. It employs more people in the continent, more than 60% of the working population. But yet, unlocking the value is hard because of the infrastructural level infancy – electricity for storage, roads for farm equipment, etc. The telcos have huge opportunities in agriculture. Agriculture accounts for 17.8% of Nigeria’s $493 billion (nominal) GDP. In other words, it is an $88 billion sector, in Nigeria.

New Architecture for Nigerian Agriculture

In the referred post above, I explained that sensors and market data will be critical. The telcos can build a modern infrastructure to power the systems.

The telecom companies will help the sensor partners handle connectivity issues with a national standard set in the nation for the agriculture space. This is good business; NCC, the regulator, should not be anywhere close. We just suggest the telcos work together and build a new business segment. Bringing a network and a platform together will quickly help drive this innovation process.

In addition to providing farmers with the ability to track everything that’s happening in their fields such as irrigation, and efficient fertilizer application, the telecom firms working with smartfarm sensors will aim to provide farmers with prescriptive and predictive recommendations based on the combination of historical, geospatial and on-farm data via dashboard. This is not just for farmers, even local gardeners will be on board and the telcos will benefit.

They need to build connectivity systems but most importantly, they need to help pioneer a new way of doing business that may do less with today’s banking system which has minimal presence in most Nigerian communities and villages. Expecting banks to support such a system will be waste of time, owing to their cost models, which may not be profitable serving farmers. For that, I propose a new “currency” that is not Naira, but pegged to the Naira. I name it Nia.

The telcos need to decouple this from the Naira to enable them innovate out of the Nigerian banking sector which has failed to serve the under-served and reach out to rural communities over generations. Having the Nia will ensure the telcos can push the limits without concerns with the Central Bank of Nigeria and the banking institutions.

The NIA Currency For Nigerian Agriculture

Nia will power every aspect of Nigerian agriculture, providing a payment system that will reach any farmer without sophisticated banking systems and processes. Nia will be the farmers’ currency; it will be pegged to the Naira. The farmers cooperatives will be the custodians. Nia will begin like a voucher which is printed by the cooperatives and distributed to specific outlets across the country. These outlets will be Cold Storage Warehouses, Farmers Hubs, Equipment Outlets/Hire etc where farmers can go and exchange produce for the voucher. For example, a tomato farmer can visit a warehouse and “sell” the tomatoes. He will be given a Nia voucher as compensation. That Nia is pegged to Naira, meaning the farmer is paid.

Modern farming requires measurements with sensors

That Nia is as good as money. The farmer can also use the voucher to buy new seeds, rent equipment etc. I want government to remove all levels of taxation for transactions done on Nia. We want Nia to be structured for only agriculture. That will stimulate investment in agriculture which is at the moment less than 1% of commercial lending.

For the agriculture system, it will form a legal tender. People can buy Nia from the cooperatives. The farmers group will put the money in interest bearing account and over time use the proceeds to invest in Cold Rooms across Local Governments in Nigeria in partnerships with telcos who will provide connectivity and technology for farmers. The vision is to build a modern layer for agriculture in Nigeria.

Every Nia in circulation must expire within two years. This will ensure we keep it off as a means of storage of value, and escalating risk of the Naira. It is expected that any farmer no matter the location will have the opportunity to convert its Nia to naira within the two years. Any unused one will expire and irredeemable.The Nia will be pegged to Naira and the cooperatives will work with banks to close the settlement.

Nia will be digital and traded online so that buyers and sellers can exchange with the currency. Printed Nia will start once implemented and end within five years. Then all Nia will move digital. It will then be traded as a currency. It will be still be pegged to the Naira. The farmers cooperatives will administer it with experts working with them.

The core vision is to make it easier for farmers to innovate and for government to provide clear incentives for investors in agriculture knowing that NIA-denominated transactions have zero taxation.

The Roles of Telcos And How They Benefit

We want the telcos to facilitate the infrastructure to power Nia, providing the connectivity and systems that will make it possible, Waiting for the banks to do so will take another 40 years. Also, the printing of Nia will be supported by Telcos since they have experience with prepaid card. They already have the biometric of most farmers, so they can roll this out faster.

Modern farming is a digital system

This is not mobile money because you want it to be out of the controls of the Central Bank of Nigeria. We want farmers to just find a way to connect members who have been neglected for generations by Nigerian institutions and governments. It sounds crazy but I do think this can work. We do think this will double the size the telecom sector within a decade of implementation.

Implementation of Nia

The following steps will help to implement Nia:

Telcos must come together and work together like the ways the Bankers Committee in Nigeria do. They have to agree on cooperative agreement to use Nia to deploy massive support to Nigerian agriculture.

Use the biometric data which have been collected during SIM registration and build a credit system specifically used to help offer telecom services to customers. The goal is that people that take services and do not pay will be easily tracked and penalized

Use the credit file to open opportunities for farmers to acquire digital systems while making sure there are local community anchors to educate and train them. Those community anchors will be compensated

Push for all monthly-payment billing where every phone line is contracted. This will happen because of the data coming from the credit system. People that take the services and do not honour the spirit will be denied SIM card access until they pay compensation. (Telcos can still keep the Pay As You Go but make it more expensive.)

Deploy the Nia currency to make it easier for farmers to do business within the networks. At the top convert that currency into the Naira.

Liberate agriculture and reach farmers at their levels with massive infrastructure made possible through zero-tax investments on warehouses, cold rooms etc across Nigerian communities. Telcoms can bring partners to invest therein. Only telcos in Nigeria have the best chance to help agriculture owing to their experiences in developing infrastructures in our challenging environments.

Rounding Up

Our banking system has neglected agriculture. A new currency will help bypass the stasis of not providing services to farmers.by the banking sector. Nia, powered by the telcos, will open a new dawn in Nigerian agriculture. We will see a fusion of technology and farming innovation, at scale. That will result to better welfare to our citizens.

Updated: A reader posted this comment on LinkedIn, which I responded below. This will help provide more insights on Nia.

Comment: The agriculture business is not for Telcos. The Sensor partners as you called them should own the business and look for the best network in their location to carry their traffic. Yes! Telcos have infrastructures, they have mobile money in place and this traffic will be an opportunity for them. Therefore they should assure quality network to capture it. Note that Google, Facebook and even LinkedIn and etc.., didn’t wait for association with Telcos to start. And I do not figure very well how this Nia Currency will work. If it is going to work like recharge card, why not continue with the existing recharge (Note that physical recharge card is a cost to them for which they are willing to totally replace by virtual recharge). And if Telcos are coming together like you proposed, they will need another body like CBN in the banking sector to do compensation. And you are rejecting NCC, the regulator, in this operation. May be you need to clarify again Nia. My personal point of view is that The Telcos are already supportive and they will continue to work along with partner that have taken step ahead.

Ndubuisi Ekekwe: Sure – Google, FB, LinkedIn etc did not wait for telcos because they had a govt. People tend to forget that US allowed many barons to make money to build U.S. infrastructure. Carnegie etc made money in steel and railway so that they can use their assets to provide infrastructure. Farmers need someone to make that money but offer them infrastructure in NG. I do not want Nia to be under the control of CBN because banks have done nothing for agriculture. For generations, they have not seen a need to find ways to reach out to them and offer services. See Nia as a currency that the govt will allow for zero taxation. It is not a recharge card. The regulator should not be against it because telcos will only facilitate not own – the cooperatives of farmers will own. On sensors – the fact remains that the sensors people can select from the telcos available, the very reason I want them together. Just as BVN works – all banks agree. Opening UBA bank account with BVN captured in GTBank does not rob GTBank. Best network quality without expanding market size does not help that much. You can have the best network for 60m people and you will reach a ceiling. It is better to expand that 60m people to 120m. On NIA, I will put out a whitepaper on that. I was struggling with space and never wanted the blog to be a tome