The AI boom, which has been the main driver behind the growth of the largest U.S. technology companies for several years, is beginning to change the balance of power in the stock market. Previously, investors were willing to support companies that actively increased spending on AI infrastructure, but now investors are increasingly questioning the effectiveness of such investments. While the payback period for multibillion-dollar investments remains uncertain, the market is gradually shifting its attention to companies that are already profiting from the ongoing shortage of semiconductor components.

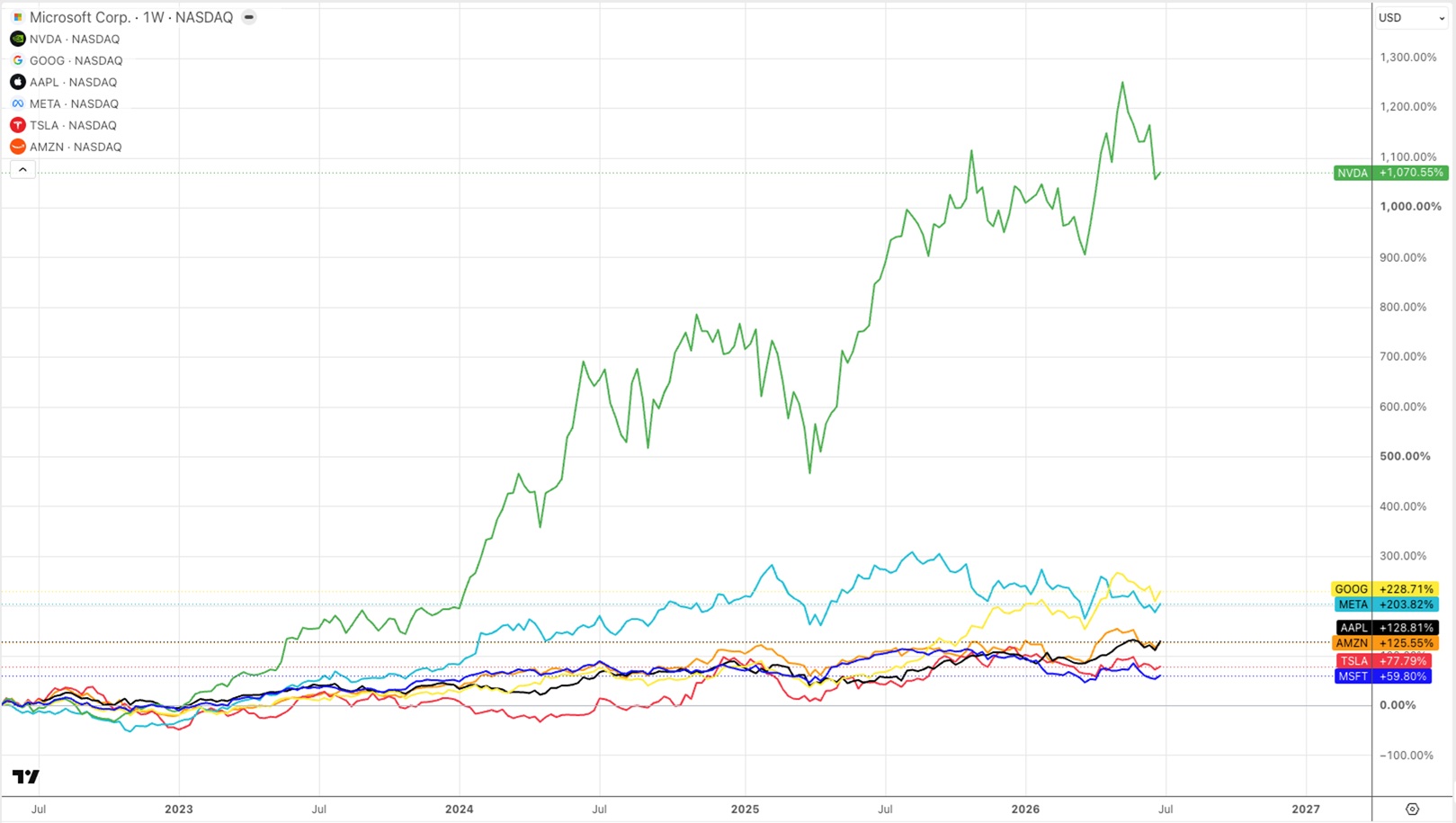

In June alone, the combined market capitalization of the seven largest U.S. technology companies — Microsoft, Nvidia, Alphabet, Apple, Meta, Tesla, and Amazon — fell by about $2.3 trillion. As a result, the conditional index of the magnificent seven lost about 10% over the month.

Microsoft posted the steepest decline, falling 20%, while Nvidia stock fell by roughly 13%. Apple and Amazon declined by about 8%. Notably, even Nvidia, which has long been considered the main beneficiary of the AI boom, is already resorting to raising debt to finance individual projects, while less financially secure market participants are forced to increase their debt burden even more aggressively.

Investor sentiment toward the largest technology companies is gradually changing. Previously, they were viewed as high-margin businesses requiring relatively little capital investment, but now multibillion-dollar investments in AI development are beginning to be seen more as long-term investments in automation and the replacement of human labor. The potential return on these investments remains high, but the market is demanding more and more evidence that they will translate into tangible profits.

Yet the AI boom itself shows no signs of weakening — only its main beneficiaries are changing. While the largest cloud providers continue to invest heavily in building data centers, manufacturers of semiconductors and chipmaking equipment are outperforming the broader market.

Further evidence of resilient demand came from Micron’s recent quarterly report, which once again showed strong business growth amid the ongoing shortage of memory chips for AI systems. The revenue of the largest cloud operators is expected to continue growing, supporting demand for semiconductor products. This could also push the company higher in the stock screener, with its market capitalization approaching Meta’s.

At the same time, the effects of the memory shortage are increasingly being felt across traditional segments of the electronics market. Shipments of personal computers in the United States decreased by 7% year-over-year in the first quarter, the worst result since the third quarter of 2023. One of the main reasons was the sharp rise in memory chip prices, as a significant portion of production capacity has been redirected toward manufacturing products for AI servers.

The segment of affordable computers costing up to $500 was particularly hard hit, with shipments dropping immediately by 18.7%. The consumer market as a whole declined by 9.5%, while the corporate segment proved to be more resilient due to the ongoing Windows 11 upgrade cycle and the desire of companies to purchase equipment in advance before further price increases.

Meanwhile, the average cost of a PC continues to rise. While selling prices increased by about 4% in the first quarter, analysts expect growth to accelerate to 12% in the second quarter, with even steeper increases possible in the second half of the year. Premium AI-enabled PCs now account for 44% of all shipments.

The changes also affected the balance of power among computer manufacturers. HP immediately cut shipments by 21.6% during the quarter, giving way to Dell, whose share grew to 25% of the U.S. market. Lenovo also strengthened its position, increasing its presence to 20%, while Apple’s share fell to 16.9%, despite the continued growth in popularity of MacBooks in the corporate segment.

At the same time, investors continue to rely on manufacturers of equipment for the semiconductor industry. Following the publication of long-term investment plans of Samsung Electronics and SK hynix, which call for more than $500 billion to expand memory production, the market began to reassess the prospects of companies supplying equipment used in chip manufacturing.

Against this backdrop, shares of the Dutch ASML reached a new all-time high, gaining 6.8%, while Applied Materials and KLA rose by about 5%. Analysts expect the global semiconductor manufacturing equipment market to reach about $250 billion annually by 2028.

Now investors’ attention is gradually shifting to the upcoming quarterly reports from ASML and TSMC. The results from the world’s largest supplier of lithography equipment and the leading contract chipmaker are expected to provide fresh insight into the strength of demand for AI infrastructure. In the meantime, the market is increasingly demonstrating a new trend. If a few years ago investors focused primarily on developers of AI services and cloud giants, today capital is increasingly flowing toward the companies that provide the technological foundation for artificial intelligence itself.