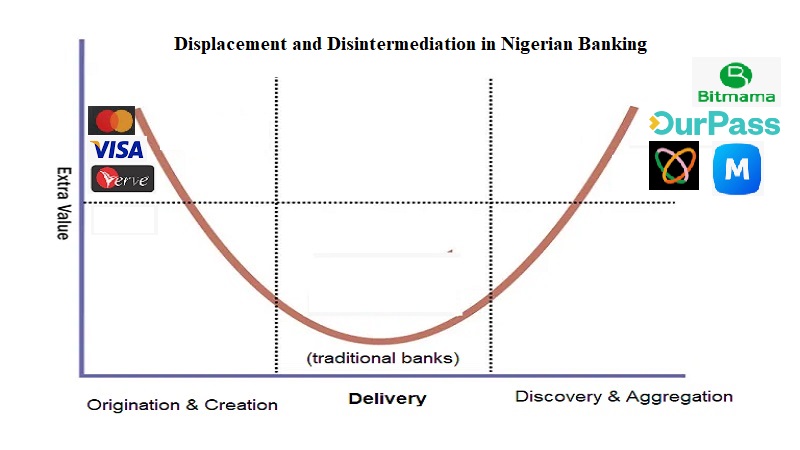

![Displacement and Disintermediation in Nigerian Banking – Why Many Microfinance Banks Will Continue to Fade [video]](https://www.tekedia.com/wp-content/uploads/2023/05/MFB-smiling-curve-768x432.jpg "Displacement and Disintermediation in Nigerian Banking – Why Many Microfinance Banks Will Continue to Fade [video]")

In this video, I respond to some of the questions on the piece where I noted that more microfinance banks in Nigeria will continue to fade. And the banking institutions which will win will be technology companies which offer banking services, and NOT banks which use technology. This is the video for this article.

(In Tekedia Mini-MBA, I explained the Smiling Curve deeper with positioning implications across sectors like manufacturing, etc)

Cessation of Non-Permissible Activities of Microfinance Banks in Nigeria

The Central Bank of Nigeria (CBN) on the 19th of August, 2021 released a circular in response to observed activities of microfinance banks that went beyond the limits of their operating licenses.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

This article will be looking at the provisions of this circular which focuses on the non-permissible activities most commonly engaged in by microfinance banks(especially digital microfinance banks), mainly wholesale banking and foreign exchange transactions. These transactions are as follows :-

– The CBN Circular is based on the consideration of comparatively low capitalization of microfinance banks dealing in FX and wholesale banking transactions which carry a huge risk for financial system stability.

– The circular is thus as a result of the need to remind Microfinance Banks (MFBs) to comply with the 2012 CBN MFB Guidelines.

– Consequently, MFBs are prohibited from FX transactions.

– MFBs are to focus on rendering services to retail clients and micro-clients.

– Microcredit and retail transaction services rendered or carried out by MFBs are limited to 500 Thousand Naira per Tier 2 unit MFB transaction and 1 Million Naira for other MFB categories.

– Microcredit facilities shall constitute a minimum of 80% of total loan portfolios for MFBs.

– A disregard or violation of the directions contained in this circular can lead to sanctions that include the revocation of an MFB license.

---

Connect via my

LinkedIn |

Facebook |

X |

YouTube