This happens all the time. A new technology is introduced and you think more value will be created because of the innovation. But the reality is that most times, despite the efficiency, technology destroys monetary value for the industry even though the consumers benefit significantly.

Consider WhatsApp, it is destroying monetary value for telecoms in Africa even though WhatsApp itself, directly we may say, is not creating further value by making money (being profitable). Sure, the valuation of Facebook which owns the product is indirectly associated with the number of users but the hard fact is that WhatsApp is not translating the value destroyed to itself in simple revenue numbers.

In the past, Skype reduced the revenue base of most telecom operators in Europe on international calls. But Skype as a company did not absorb that lost revenue into its balance sheet. What happened was the value was destroyed even though customers enjoyed largely free product.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

McKinsey Study

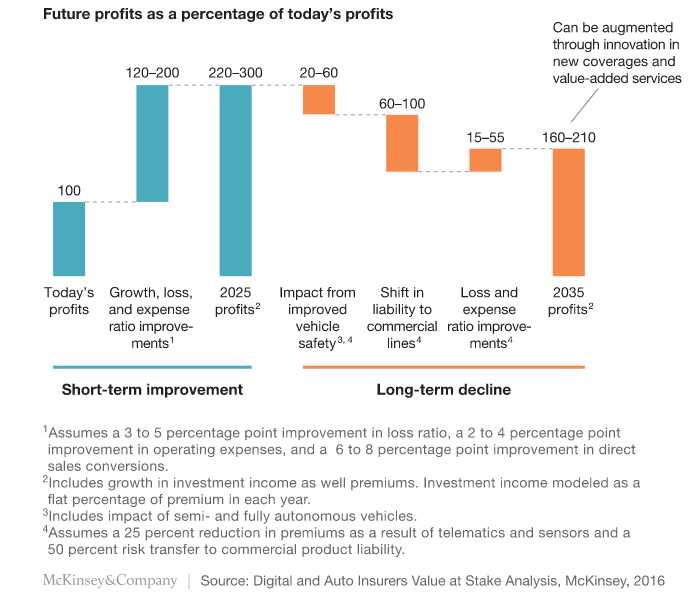

McKinsey, on the same construct, has the view that the digital dawn in insurance actually destroys value—transferring power from the carrier to the customer and eroding profits. In the United States, McKinsey estimates auto insurance premiums could decline by as much as 25 percent by 2035 due to the proliferation of safety systems and semi- and fully-autonomous vehicles.

For a long time, the traditional insurance business model has proved to be remarkably resilient. But it too is beginning to feel the digital effect. It is changing how products and services are delivered, and increasingly it will change the nature of those products and services and even the business model itself.

Data and analytics are changing the basis of competition. Leading companies use both not only to improve their core operations but to launch entirely new business models. Insurers have valuable historical data. Yet in a few years’ time, will they be able to keep pace and still add underwriting value when competing with newcomers that have access to more insightful, often real-time new data culled from the Internet of Things (IoT), social media, credit card histories, and other digital records. Knowledge about how fast someone drives, how hard they brake, or even (more controversially) what they get up to as displayed on social media is arguably more revealing data on which to assess risk than simply age, zip code, and past accident record. (Facebook recently moved to prevent its users’ online activity being used by insurers in the United Kingdom—proof of the potential power of access to good data.)

And what if those with the necessary data and analytical skills and platforms that reach millions—a Google or an Amazon—not only offered well-targeted, tailored products, but also began to cherry-pick low-risk customers? If they did so in significant numbers, the insurers’ business model, whereby premiums collected from low-risk policyholders contribute to the claims of high-risk ones, could fall apart.

Auto manufacturers are arguably close to changing the game for insurers. The fitting of connected devices as standard in cars is not far off, potentially giving manufacturers unique access to data that could accurately ascertain the risk of their customers, as well as ready-made access to drivers in need of an insurance product.

The Future

In the near future, it is possible that insurance may not need to be offered by insurance companies. Google has a better chance of selling home appliance insurance with all the sensors coming from Nest. The same argument that car companies can simply use the collected data from their OBD sensors to sell insurance to car owners.

What happens to insurance companies? They will be cut-off of the loop.

Insurance companies may need to aggressively redesign their business models to ensure they can compete in this age because while we need insurance, we do not necessarily need insurance companies.