I had set out for Ahia-Ohuru open Market in Aba that fateful Saturday morning with my monthly grocery list. After driving around for a while in search of parking space, I finally managed to squeeze in somewhere at the back of Enyimba Sports Stadium and started the short walk towards the market.

Up ahead, my attention was quickly drawn to gathering of people ahead of me. Whatever was going on there seems to have its audience enchanted.

As I drew closer, the crowd erupted into frightened shouts.

Register for Tekedia Mini-MBA edition 20 (June 8 – Sept 5, 2026).

Register for Tekedia AI in Business Masterclass.

Join Tekedia Capital Syndicate and co-invest in great global startups.

Chineke!

Ogbu o le ya!

Jesus!

Some ran away temporarily only to return. Curiosity killed my cat and I joined the circle of onlookers.

At the centre, what looked like a skillfully cut-out human tommy sat face down on a semi-open discarded Peak Milk carton. A half-clad Medicine Man, eye ringed in white chalk, was muttering incantations in Igbo with his legs spread over the tummy.

A teenage boy who looked like an apprentice pick-pocket nudged me at the bum. I instinctively transferred my wallet from my back pocket to my left hand, where it is safer.

Some fellow onlookers, converted to customers, were buying piece of herbs and roots from the Medicine Man’s Assistant at to the right from where I stood.

Apparently, the magic of turning his second assistant into a seating tommy has convinced them of the efficacy of the Medicine Man’s wares. As the white eyed man was slowly pulling out a live python from underneath the seating tommy amidst momentary shrieks, my attention is drawn to smaller crowd that had just gathered beside the bigger one.

Being a lazy Saturday, I overcame my temptation by joining the smaller crowd.

Forget about the Bollywood movie, I had planned to watch when back from the market, this was a live Nollywood scene. Why not? There in front of me was an elderly man of about sixty-something just won wades of clean N5,000 notes simply by putting down N500 and then identifying the Joker among three cards placed face down after a clever shuffling of hands by the Artist.

I volunteered a mere N200 and won N1,000. Venturing further, another N500 earned another N5,000. Business was sweet. This artist guy must be a fool, I thought. It was so easy sporting the right card if you have attentive eye.

The guy then placed on his make-shift table a hundred thousand naira – mint bundle of one thousand notes with its bank paper wrap still intact. He invited us to play with N10,000.

Greed called my name, I resisted.

My village people muttered words of encouragement. But I was adamant still.

I resisted every temptation to go further, stuffed my profit into my wallet and started quietly meandering my way to where I was going. Nobody made any attempt to woo me back.

God bless Mama Nkeiru!

As always, she helped source all the things on my list while I seat reading a newspaper. She was pretty fast today. My bill was N35,550.

I dug into my wallet only to pull out wades of neatly folded plain papers. Gang…gang!

No, the devil himself must have carefully arranged these god forsaken papers where the money I left home with this morning and my card profits were supposed to be resting. I realized immediately that an exchange must have taken place between I and the card guy whom I thought was a fool. I was the fool really and have always being! I sat down to recover my nerves.

I offered Mama Nkeiru the option of returning the items or driving with me home for her money. She wisely went for the later. As we walked to where I packed my car, the crowd seemed to have disappeared into thin air. How can I tell Mama Nkeiru this was where I subjected myself to African Abracadabra – a Saturday morning show of ‘the more you look the less you see?’

How can I?

That was in my other life many years ago.

I learnt to be wary of trading money for money after my reincarnation. Or so I thought until…until…wait for this!

After my reincarnation, I decided that the best place to make profit was earning unambitious interest on my meager savings in then Gulf Bank as a student aspiring for admission. The savings was started two years earlier to raise money for my school tuition. But in 2004, Gulf Bank went underground just at the point I got admission.

I prayed and fasted to no avail. I was forced to source my tuition from other avenues until three years later when Uncle Charles Soludo skillfully connived with UBA to return my money that was trapped in Gulf Bank. Indeed, God answers prayer! I started believing again in regulatory agencies such as CBN and Dora Akuyili’s reformed NAFDAC.

Buoyed by the successful return of my money by CBN through UBA, I picked up a savings (I don’t view it as an investment as it was basically a way of keeping money I didn’t want to touch) product that same 2008 with AIMS Assets Management Ltd in Kano. After four years of monthly savings with AIMS Assets, I turned up one day at their Kano office to stare back at some giant padlocks staring back at me.

Several phone calls to my account Manager and AIMS Assets head office ended in a frustrated attempt to seek redress from Security and Exchange Commission (SEC) in 2012. As I write, SEC has not been able to do anything about that.

Being an incurable belligerent he-goat, I still got myself into another financial dilemma by taking up an assurance policy with Industrial & General Insurance (IGi) in 2013. After several unprintable poor customer experiences, I decided I had had enough and surrendered for claim in October 2018. After three months of silence from IGi, my lawyer sent in a letter. Within the same period, IGi sent me a penalized value voucher for early surrender. It is now over 9 months since I surrendered for claim and IGi is yet to pay my money.

Their Kano office is also in locks. My account officer has joined a competitor. The current Branch Manager has no idea of what customer service is. Head office contact lines will not pick calls. Except for two occasions, mails are not being responded to.

For an industry that is viewed with an unbelievable skepticism by Nigerian, one will at least expect the insurance industry in Nigeria will raise the bar to build positive customer experience. Alas, the reputation of that sector is such that almost all employees in that industry wear a certain look of dissatisfaction. I had my compulsory undergraduate industrial attachment in this industry. So, I know they even struggle to attract quality professionals.

The job of their salesmen has become such a horrible daily experience due to the difficulty of convincing Nigerian to take up policies. Abroad where industry outlook are far better owing to better regulations and practice, insurance sales persons still grapple with negativism not to talk about a place like Nigeria where the word insurance is dreaded. A search on social media such as Twitter and Facebook will shock you at the number of people recounting their unpleasant ordeals in the hands of insurance companies in Nigeria.

The industry regulatory body, National Insurance Commission (NAICOM), like their counterparts in several other industries remains in an unbelievable docility proving unable to help ordinary citizens that have ventured to put their trust in them. There seem to be this ‘sidon dey look’ posture that even simple complaint mails do not receive any personal response.

Someone recently posted his unpalatable experience with one of the Air lift companies in Nigeria aviation industry with myriads of commentators unanimously agreeing that there is no such thing as regulatory bodies in Nigeria. Organizations such as NAICOM, SEC, among others basically seem contented with collecting salaries. My aim is not to call them out on this piece but it is my wish that more attention be paid to regulatory agencies effectiveness in Nigeria. This will lighten the pains of ordinary Nigerians like yours truly.

If steps are not taken to hold the leaders of these agencies accountable to their duties, faith in the system will keep eroding.

Oh, you may be wondering why I am not talking about legal redress. The legal system is a several years dance in the market square by the end of which the Ngwo tree may have being scourged dry of its last pint of palm wine. That in itself has to be a last resort, in this financial and regulatory circuit show, of the more you look, the less you see.

Nigeria needs better regulatory systems and NAICOM must step forward to help deepen the growth of the insurance sector.

More customer experience narration

The guy is a smooth talker.

I had noted that while watching him diffuse the anger of other customers from where I sat. Though I couldn’t quite make out the conversations, I could tell an angry customer when I see one. I admired Smooth Talker’s skill – at least, until it got to my turn.

As I narrated what brought me to their head office, all the way from Kano, he listened with rapt attention.

‘You mean you surrendered your claim since 10 months ago?’ Smooth Talker asked and went ahead to paraphrase all I said earlier.

I nodded as I handed him a copy of my returned voucher and the letter my Lawyer had written to them about seven months ago. He examined it, went in to verify and came back. I could see he is ‘feeling my pain’ in that professional trained ways as he went on to tell me how that his company is undergoing liquidity challenge. How they have lots of assets but are struggling to get buyers to settle claims. How a court order froze their bank accounts. How they were going to send me an email detailing their payment plan.

I scratched my head at that last one knowing these people don’t even pick calls any more nor do they reply to customer emails. The last time I checked, the globally excusable practice is for the debtor to initial this communication process long before a big-headed creditor like me show up at their corporate head office all the way from over several hundred kilometers.

Notwithstanding, I listened as he went on and on narrating what, from my view, was a pathetic story of a corporate organization that has failed in its responsibility towards its customers. For me, what he was reeling out was a once-upon-a-time tell tale of how some big corporate executives have used customers money to ‘chopulate life’ and now wants to subject mere social expendables like me to their well-practiced corporate bullying.

Once I sensed Smooth Talker’s tank was empty, I dipped into my Great Grand Mother’s Tortoise folklore bag and brought out a few of my personal recollections to refill Smooth Talker’s eardrum.

My wife’s shop rent is four months overdue; the last two terms of my children’s school fees were unpaid and school is resuming in three weeks; all my village people are sick and as their breadwinner, I am been looked on to foot their medical bills; and to cap it all, I borrowed money to make this journey and don’t even have money to return back to Kano. I produced my kwashiokored wallet to validate my story. Finally, I indicated I don’t mind sleeping on the chair where I sat while waiting for them to pay my money for as long as it may take.

From his look, I could tell my moonlight tales was a sucker punch – he sure wasn’t expecting that! He obviously was expecting the same angry reaction like those he has dealt with earlier. I watched as Smooth Talker rose with difficulty. My tale of woes surely was weighing heavily on his shoulders as he walked into their inner office to meet his superiors with a copy of my voucher.

Few minutes later, he returns to say they are cascading it up to see what can be done – even if it means having to pay the money in two or three installments. That news was a left hook on my jaw and I staggered under its force. I was tempted to remind him the law places a limit on the length of time within which an insurance company must settle a customer’s claim. That same law failed to empower customers to claim compounded interest where the Insurer fails to pay within limit. So, like some prey-hunting teething cub, I gathered my wits and waited for them to commit.

For a complainant who turned up exactly 10am that morning, it was till sometime around 4:30pm that another less skilled Smooth Talker came to inform me they will ‘do something but that has to be tomorrow.’

I came prepared to wait.

Accommodation sorted out, I was there the next morning 10am dot.

Smooth Talker came again that morning. This time, he said they are able to raise me about one-third of my money and will give me a written commitment on when the rest will be paid. I protested. Smooth Talker literally told me to either take it or leave it and added with raised voice that ‘it is impossible for them to pay me more than that now. The money was gathered from some office stationary imprest cash.

Corporate bullying was fully in action now.

Having seen how all the other customers who raised voices and threats yesterday left there with nothing and also the presence of some Official Intimidation Dogs in black Uniform waiting for instruction to bundle anyone fool-hardy enough as to make a scene into their Cell, I played it cool and agreed. After all, what can I do to these big bullies in very tall several story building?

Two hours later, Smooth Talker came again.

This time he informed me they are sending someone to the bank to process the payment but added, more importantly, that they can’t issue me the already agreed commitment letter (he had obviously forgotten their bank accounts were supposed to be frozen and the money ought to be coming from cash impress). At that, thick black smoke came out of my ears, nose and mouth – I was now ready to end in that Police Cell.

Wise Smoothie sensed that they can’t twist my hand again and went back to produce they letter. When it arrived, it had the presupposed balance split into two further installments in three-to-four-month time.

“That balance has to come in one lump sum. You can’t make a total mess of my plan because of your corporate inefficiency,” I thundered. “What kind of circuit trick are you guys playing on customers here?”

Smoothie ventured further but I immediately let him know that will be calling for trouble there and then. He must have noticed I was past caring and quietly went in to alter the letter as I requested. Even with the letter, I knew it was nothing else but a promise that can be broken with further stories that touch the heart.

Other unprintable dramas followed regarding the about one-third they agreed to pay so much so that I had to spend the next 3 in Lagos days before receiving that annoying and pacifying Bank alert confirming the part payment.

All these trouble, time and monetary expenses just to recover one-third of money I should normally receive without lifting a finger in climes where things are done properly. I thought of a prominent US personality who said something pertaining to ‘shit holes.’

Where things are properly done, Insurance customers would receive their settlement maximum 48hours after returning voucher.

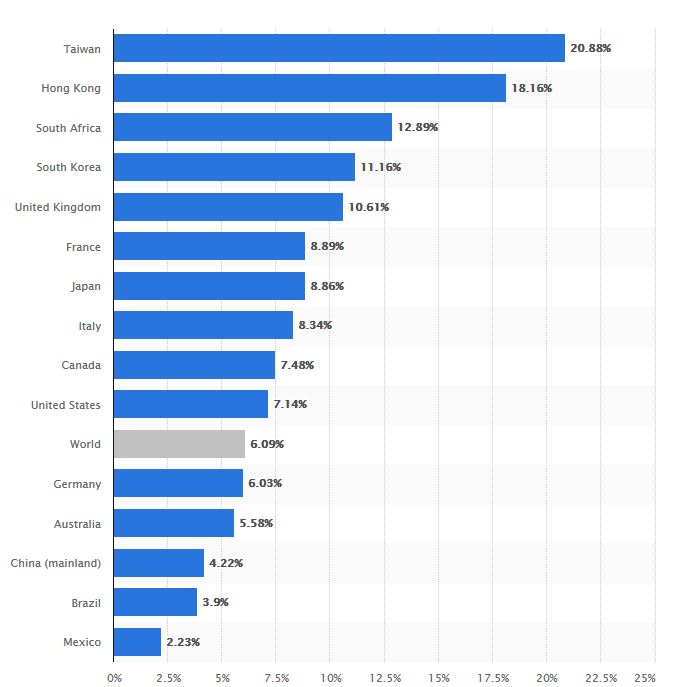

Little wonder, the reputation of Nigerian Insurance industry is in tatters. Little wonder Nigeria Insurance sector still have one of the lowest insurance penetration levels in Africa at 0.3% against South Africa’s 12.8% as at 2018. Little wonder industry gladiators hold several conferences and yet are unable to positively influence the poor awareness and perception of the industry. Little wonder what is supposed to be a great way to save and provides security against risk and uncertainty has turned out to be such terrible customer nightmare.

Where things are properly done, the law and the supervisory body ought to have swung into action after receiving my complaint.

For emphasis, Section 70 of the Insurance Act 2003 requires that claims must be settled within 90 days of the insurance company accepting liability and issuing its discharge voucher. If the company fails to pay within this period, as IGi has done, I as a customer have the right to approach the insurance supervisory body, National Insurance Commission (NAICOM), and ask the Commission to pay me. May be I will have to remind the commission that about this right.

Where things are properly done, and by law, IGi should have notified me in writing on why they are unable to pay in 90 days, and again, if I am not satisfied I can approach the regulatory agency for settlement. But that is only where things are properly done.

As I noted above, NAICOM has failed to even respond formally to my complaint, except for an automated computer response. Where does this kind of industrial irresponsibility leave our insurance industry?

It still beats me why NAICOM are still lingering on the recapitalization that is long overdue.

While they are at that, I am collecting stories of poor customer experiences in this sector, with a focus on IGi, to share with readers on this platform. I will keep shouting through my keyboard until someone do things right in Nigerian Insurance Industry.

Meanwhile, if you want me to write about your plight and raise awareness on the bad practices of our Insurance service providers; you can share your poor customer experiences in this and other industries with me via 08129901475.

What a harrowing experience, that is.