The recent abduction of schoolchildren and teachers in Oyo State has ignited a fierce national debate, exposing a deep rift in public opinion over how to secure the release of the captives. As the victims remain in the custody of bandits, Nigerians are increasingly divided between those advocating for immediate ransom payments to save lives and those warning that such actions constitute a criminal overstep that further undermines national security.

For many, the primary concern is the immediate welfare of the children and their teachers, who are currently enduring the harsh conditions of the forest. Proponents of negotiation argue that the “stress will be getting too much for them,” making any move to secure their release the “best idea”. One popular suggestion circulating on social media is for the government to engage in a tactical manoeuvre: pay the ransom “in disguise” to ensure the victims are safely returned, and then deploy security operatives to “pursue the bandits to any length”.

However, this sentiment is met with significant scepticism. Many Nigerians fear that payment provides no guarantee of safety, with some observers bluntly warning that the kidnappers “go still kpai” (will still kill) the victims even after receiving the money. There is also a growing suspicion that the bandits’ demands may be “beyond [the government’s] power” and involve more than just financial compensation, suggesting a more complex and “powerful” motive behind the abduction.

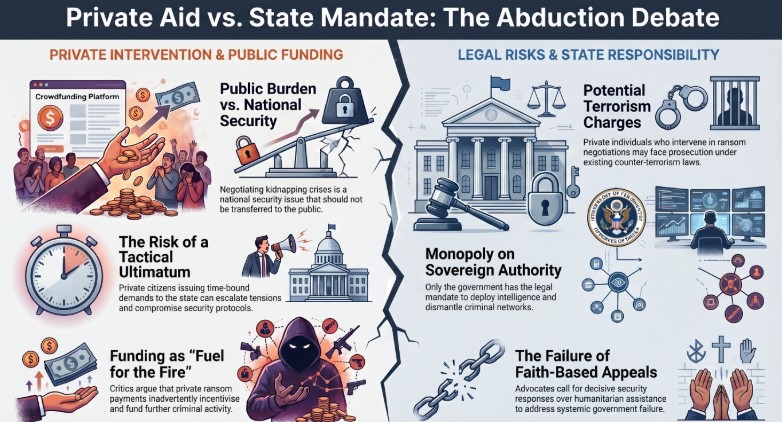

The debate has also taken a sharp legal turn following reports of a public figure, referred to as VeryDarkMan, issuing a four-day ultimatum to the Federal Government. This move has been widely condemned by critics who label it as “illiteracy” and a dangerous challenge to state authority. Legal experts and concerned citizens have pointed out that “only government has that authority” to negotiate with terrorists. Under current laws, any private individual who attempts to crowdfund or pay a ransom could find themselves facing terrorism charges. Critics of VeryDarkMan’s approach argue that “nobody is more powerful than the government” and that such private ultimatums “indirectly [put] more fuel on the fire,” incentivizing future kidnappings.

Amidst these legal warnings, a significant portion of the public is directing its frustration toward the government’s perceived inability to fulfill its primary duty of protection. The abduction has sparked a backlash against the tendency to rely on religious appeals during national crises. “We should stop attaching everything to faith,” one citizen argued, noting that despite Nigeria having more worship centres than factories, the security situation continues to deteriorate. The call is now for the government to “do the needful” by deploying intelligence and security resources to dismantle criminal networks rather than waiting for divine intervention or public donations.

Specific questions are also being raised regarding state-level accountability. In Oyo, residents are questioning what happens to the “huge security vote” the Governor receives every month specifically “to protect the people”. There is a burgeoning consensus that the burden of this national security crisis “should not be transferred to the public” through crowdfunding. Instead, the public is demanding a “decisive security response” that improves protection for schools and rural communities.

The crisis has also indicated a painful socioeconomic divide. Commenters have noted with bitterness that bandits often target the “less privileged” rather than senators or the “well-to-do” who could pay ransoms “sharply”. This perception of the poor being used as pawns has only increased the pressure on the Tinubu administration to act. Some have even suggested that if the President continues to borrow money for other state functions, he should “borrow… to save those children in the forest”.

As the standoff continues, the collective mood in Nigeria remains one of desperate urgency tempered by a fear of long-term consequences. While some individuals have expressed a willingness to “gladly be a part of the donors” to save the children, others maintain that such humanitarian impulses, while noble, cannot replace the sovereign responsibility of the state.

Our analyst notes that Oyo schoolchildren and teachers remain at the centre of a storm that is as much about the future of Nigerian law and order as it is about their individual lives. The government remains under immense pressure to find a solution that balances the immediate need for a rescue with the imperative to avoid “fueling the fire” of the nation’s kidnapping epidemic.