Do you ever look back at your portfolio and wonder how you missed the exact moment a project transitioned from an unknown idea into a market leader? It is a heavy realization, especially when you watch others capture life-changing gains from assets you had on your watchlist but never pulled the trigger on. The history of crypto is paved with stories of those who hesitated on projects like Hyperliquid (HYPE) when they were still in their early stages. While everyone was busy doubting the decentralized exchange model, a small group of early believers quietly accumulated, eventually watching their positions multiply as the platform became a cornerstone of DeFi infrastructure.

The truth is that regret in this space is almost always a byproduct of waiting for the perfect moment that never arrives. Projects like HYPE succeeded not because they were lucky, but because they solved a massive, specific problem in liquidity fragmentation. The missed opportunity here was not about a lack of information; it was about a lack of conviction at the right time. Every successful cycle offers a fresh chance to identify the next infrastructure-heavy asset before it hits mainstream exchanges, but you must be willing to distinguish between noise and actual utility.

Why DOGEBALL Is Setting A New Benchmark For Utility-Driven Presales

DOGEBALL is moving beyond the standard expectations of a token by integrating a custom Ethereum Layer 2 solution known as DOGECHAIN. This ecosystem is engineered to solve the real-world friction of cross-border finance by combining GameFi and PayFi into one seamless flow. Users can send crypto and have the recipient get fiat directly into their local bank account anywhere in the world, effectively bypassing the delays and high costs of traditional banking and remittance services.

What makes this project different is its focus on tangible application rather than just speculative hype. By offering zero FX fees, sub-second transaction finality, and a specialized offramp for over 30 currencies, it addresses a genuine pain point in the global economy. This is a project designed to function as an actual payment rail, making it a serious candidate for anyone tired of projects that offer nothing but empty promises.

Analyzing The Presale Growth And Potential ROI Of DOGEBALL

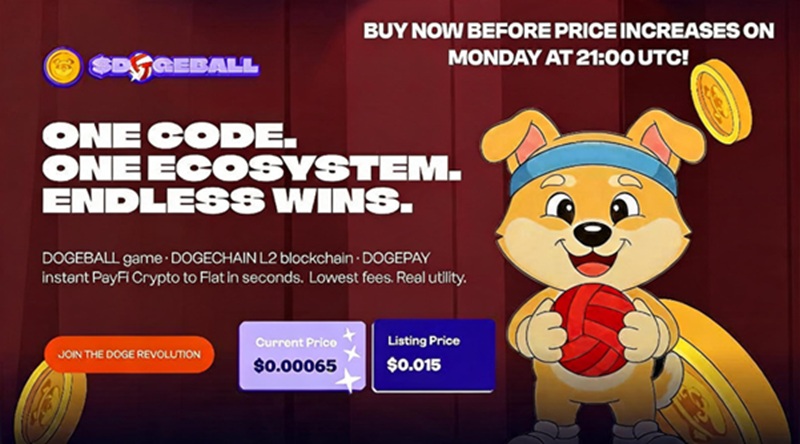

The trajectory for the DOGEBALL crypto presale 2026 is currently defined by a disciplined, time-sensitive expansion. With more than 295K raised and 1,000+ participants already on board, the project has transitioned into a 20-stage timed phase where prices increase every Monday at 21:00 UTC. To show their long-term commitment, the team recently burned 4bn tokens—representing 20% of the total presale supply—to ensure scarcity and protect early value.

If you act during the current stage at $0.00065, you are positioning yourself at a significant advantage before the planned launch at $0.015. To put the potential profits into perspective, consider the math: an investment now could lead to a 23x multiplier, which translates to a potential return of 2207%. With the presale stages moving fast and the official exchange launch partnership already secured, the window to get in at these entry-level prices is closing rapidly.

Simple Steps To Join The DOGEBALL Crypto Presale

Participating in this opportunity is designed to be efficient for anyone with a Web3 wallet. You simply need to ensure your MetaMask or Trust Wallet is funded with ETH, USDT, or BNB, then connect to the official DOGEBALL website via their secure dashboard.

Once connected, you select your payment currency, input your contribution, and complete the transaction. Your tokens are then ready to be held, and you can monitor the project’s progress directly through the live presale widget. There is no complex process here; it is a straightforward path for those looking to secure their position before the next price increase occurs this coming Monday.

Conclusion On Strategic Positioning And Future Growth

The reality of the crypto market is that the most significant wealth is often generated by those who act when the rest of the market is still debating. Just as early adopters of HYPE found success by recognizing utility before it became obvious, today’s investors have the same opportunity with the DOGEBALL crypto presale. By integrating a custom L2, near-zero gas fees, and a global fiat offramp, this project is built for long-term relevance.

The upcoming launch, supported by a specialized Web3 partnership, is designed to ensure the token becomes a mainstream utility. Do not let this become another story of “what could have been.” The current stages are designed to reward early action, and with the price rising every week, the opportunity to enter at the lowest possible cost is a time-sensitive window that will not remain open indefinitely.

Find Out More Information Here

Website: https://dogeballtoken.com/

X: https://x.com/dogeballtoken

Telegram Chat: https://t.me/dogeballtoken

FAQs For DOGEBALL Crypto Presale

Which presale crypto is best?

The best presale is one that solves a clear, real-world issue. DOGEBALL is a top choice because it uses its own custom L2 to eliminate the high fees and slow speeds typically found in global remittances and gaming.

Which crypto has 1000x potential?

Assets that build their own essential infrastructure carry the highest growth potential. DOGEBALL is positioned for massive scalability because its token powers an entire ecosystem of gaming and instant payment services.

Is it good to buy presale crypto?

Buying a presale is a smart strategy when the project has an audited contract and clear utility. DOGEBALL is a low-risk, high-value choice because it provides a working, testable L2 blockchain for all its users.

What is the biggest crypto presale in history?

The most successful presales are always ecosystem builders. DOGEBALL follows this model by creating a full-stack gaming and payment environment that fills a massive gap in the current financial market.

Which meme coin will reach $1 in 2026?

Reaching $1 requires strong, consistent utility. DOGEBALL is superior to standard meme coins because it facilitates high-frequency global payments, creating real, organic demand for the token across its entire platform.