The year 2026 could see the Ozak AI token outperform Ethereum. This is primarily because the Ozak AI ecosystem has established a strong roadmap starting from the $OZ presale stage. Ozak AI has already generated a 12× ROI for Phase 1 investors and is estimated to deliver over an 83× ROI for Phase 6 investors. In comparison, ETH may only achieve around a 5× return in 2026.

Also, Ozak AI is backed by strong and modern technical specifications, like the fusion of AI tools and tokenized growth. These are in addition to the decentralized infrastructure, which still supports the overall structure for $OZ.

$OZ Outperforming ETH and Presale Progress

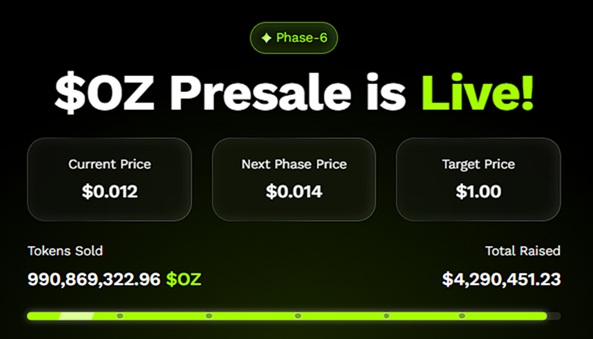

Ozak AI is currently in Phase 6 of its presale, with the $OZ token priced at $0.012. So far, the project has raised over $4.02 million by selling more than 969 million tokens, marking a 1,100% increase from the Phase 1 price of $0.001.

It is estimated that $OZ could outperform ETH even if ETH reaches $10,000 in 2026. For example, a $1,500 investment in ETH at today’s price would yield a 6.67× return if ETH hits $10,000. In comparison, investing the same $1,500 in $OZ at its current price of $0.012 could potentially grow to $75,000 if the token reaches its $1 target—a 50× return.

Even with more conservative growth, such as a 10× increase, the investment would still rise to $15,000, providing higher profits and a larger relative gain than the same investment in ETH.

Still, more presale phases will be lined up till all 3 billion tokens are sold out. This represents 30% of the total supply of 10 billion tokens. The remaining portion of the supply is allocated to Ecosystem & Community (30%), Future Reserve (20%), Team (10%), and Liquidity & Listings (10%). The $OZ offer value will be revised to $0.014 from $0.012 after it commences Phase 7.

Technical Attractions of Ozak AI ($OZ)

Outperforming ETH in 2026 is also backed by the strong technicalities of the Ozak AI ecosystem. This includes DePIN design, cross-chain functionality, and token utility, to mention a few features. For starters, DePIN design works to lower the chances of data tampering and loss by leveraging blockchain and IPFS nodes. It essentially distributes data across a network of nodes.

Cross-chain functionality enables seamless operations for Ozak AI across multiple blockchains. This paves the way for $OZ to grow with stability. Token utility entails the power to participate in governance and contribute to the expansion of the ecosystem. Moreover, the holders of $OZ can engage in staking activities and exclusively access AI Agents & a real-time analytics feed.

The AI-powered infrastructure boosts automation, optimization, and smart analytics. Security and transparency are ensured by Certik and Sherlock through the deployment of advanced tools that frequently audit smart contracts to identify and address vulnerabilities.

Key Partnerships of Ozak AI

Ozak AI recently entered into a partnership with Meganet and Phala Network. A partnership with Meganet covers architecting an efficient and distributed computing capability that can fetch real-time financial insights. Ozak AI and Meganet have also agreed to work to save costs on AI processing.

A partnership with Phala Network is aimed at enabling secure and private AI prediction models specifically for financial markets. Ozak AI will contribute with Prediction Agents, and Phala Network will bring a stack of CPU-GPU-TEE to the table.

$OZ Over ETH in 2026

Suffice it to say, the Ozak AI token has the potential to generate a higher ROI compared to ETH in 2026. This is after considering that $OZ reaches just half of the target price. The technical specifications of the ecosystem, like the fusion of AI tools and decentralized infrastructure, are positioning it to dominate the next year.

For more information about Ozak AI, visit the links below:

Crypto history is full of splendid memories of small investments becoming large fortunes. Dogecoin and Shiba Inu led that revolution, creating waves of millionaires at some stage in beyond bull markets. Their meteoric rises, pushed by means of network strength and viral strength, described the power of early positioning. But as the next bull run gathers steam in 2025, the focus is moving from memes to a significant era.

That’s where Ozak AI comes in—an AI-driven project blending real-world functionality with early-stage opportunity. With its presale price at just $0.012, Ozak AI could be the next big story that turns strategic investors into the next wave of crypto millionaires.

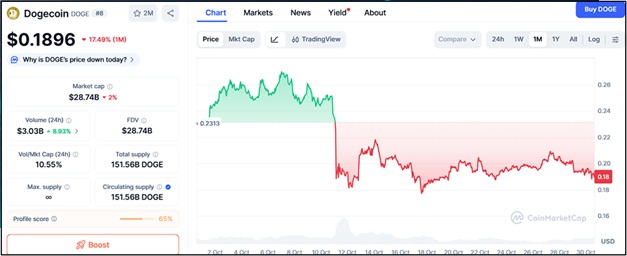

DOGE

Dogecoin, currently trading around $0.1896, remains the most iconic meme coin in lifestyles. Its current technical setup indicates resistance at $0.215, $0.258, and $0.295, while support lies at $0.175, $0.160, and $0.142. These levels suggest that DOGE is still consolidating, but with developing social sentiment and market liquidity, a clean rally will be drawing close.

DOGE’s story is legendary—what began as a joke became a financial phenomenon. Early investors who bought DOGE under a cent saw life-changing gains as the token rocketed to over $0.70 during the 2021 bull run. However, with its massive market cap and reduced volatility, the probability of another 100x move is slim. It remains a cultural and historical pillar of crypto, but the next explosive growth will likely emerge from projects still in their infancy—projects like Ozak AI.

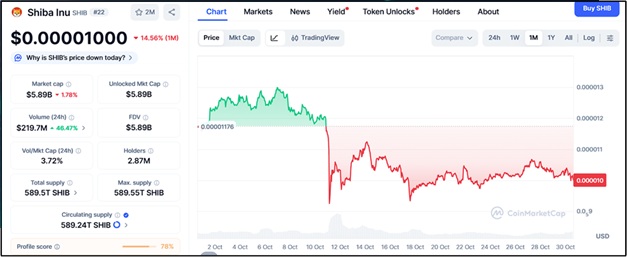

SHIB’s Community Strength and Ecosystem Growth

Shiba Inu, trading near $0.00001, continues to be one of the most lively altcoins within the market. Its resistance ranges are at $0.0000113, $0.0000126, and $0.0000142, whilst help sits around $0.0000093, $0.0000087, and $0.0000081.

Unlike most meme coins, SHIB has evolved beyond speculation. The introduction of Shibarium—its Layer-2 blockchain—has given SHIB real-world functionality, supporting DeFi packages, staking, and NFTs. Combined with regular token burns and a large community of over 1.3 million holders, Shiba Inu remains a top project for steady increase. But again, whilst SHIB may additionally nonetheless deliver 10x to 20x returns, it now does not give the once-in-a-lifetime access capacity that it did for the duration of its early days.

Ozak AI: The Next Big Crypto Breakout in the Making

Ozak AI is changing how investors perceive early-stage projects. Currently in its 6th OZ presale stage at $0.012, Ozak AI has already raised over $4.2 million and sold more than 980 million tokens, signaling strong investor confidence. The project focuses on AI-powered prediction agents—intelligent systems designed to deliver real-time market insights, predictive analytics, and automated trading strategies.

This unique utility sets Ozak AI apart from meme coins. It’s not driven by hype but by innovation—fusing artificial intelligence and blockchain technology to give traders smarter decision-making tools. As AI continues to dominate tech trends globally, Ozak AI is positioning itself as one of the most promising projects of 2025, capable of bridging crypto’s analytical and automation gap.

Partnerships Strengthen Ozak AI’s Foundations

Ozak AI’s credibility is further reinforced through key partnerships with Perceptron Network, HIVE, and SINT. These collaborations improve scalability, data accuracy, and integration across decentralized networks. Additionally, Ozak AI has undergone security audits from CertiK and Sherlock, ensuring transparency and investor protection—two elements crucial for long-term sustainability.

Dogecoin and Shiba Inu proved that timing, belief, and community can create unimaginable wealth in crypto. But Ozak AI is now evolving that narrative. It represents the next generation of high-upside tokens—combining early-stage entry with groundbreaking technology.

As the 2025 bull run intensifies, DOGE and SHIB may continue to deliver solid returns, but Ozak AI could be the one rewriting crypto’s next millionaire story. For traders ready to flip hype-driven gains into intelligent innovation, Ozak AI stands as the smartest bet of this cycle—and potentially, the next name whispered in every crypto success story.

About Ozak AI

Ozak AI is a blockchain-based crypto project that provides a technology platform that specializes in predictive AI and advanced facts analytics for monetary markets. Through machine learning algorithms and decentralized network technologies, Ozak AI enables real-time, correct, and actionable insights to help crypto fanatics and companies make appropriate decisions.

The U.S. Department of the Treasury has announced a new composite interest rate of 4.03 percent for Series I savings bonds issued between November 1, 2025, and April 30, 2026.

The updated rate represents a modest increase from the previous 3.98 percent yield that was offered through October, marking another adjustment in response to inflation data and broader shifts in the bond market.

According to Treasury data, the new rate includes a variable portion of 3.12 percent, which reflects recent inflation figures, and a fixed rate of 0.90 percent that will remain constant for the life of the bond. The combined composite rate of 4.03 percent is the result of these two elements after rounding. The fixed rate is slightly lower than the 1.10 percent announced in May, but analysts note that it remains competitive given the current environment of easing inflation and declining yields across Treasury securities.

Series I bonds, introduced by the U.S. Treasury in 1998, are designed to protect investors from inflation while offering the security of a government-backed asset. The composite yield is recalculated every six months, in May and November, based on the Consumer Price Index for All Urban Consumers (CPI-U). Each bond’s variable portion adjusts in step with the rate of inflation, while the fixed rate — which represents the real yield above inflation — remains constant throughout the bond’s 30-year lifespan.

Under this structure, an investor who purchases an I bond in November 2025 will earn the current 4.03 percent annualized rate for the first six months. After that, the variable component will reset based on inflation at the time, while the fixed portion remains locked at 0.90 percent. For example, a buyer who purchased an I bond in March 2025 at a 1.2 percent fixed rate saw the variable portion adjust from 1.90 percent to 2.86 percent in September, yielding a new composite rate of roughly 4.06 percent. The mechanics are designed to ensure that I bond returns reflect inflation trends while offering some stability through the fixed-rate element.

Interest on I bonds compounds semiannually and can be earned for up to 30 years unless the holder redeems the bond earlier. The Treasury requires that I bonds be held for at least one year before redemption, and if an investor redeems before five years, they forfeit the last three months of interest as a penalty. Interest income is exempt from state and local taxes, though it is subject to federal income tax, which can be deferred until redemption or final maturity.

I bonds have a $10,000 annual purchase limit per individual when bought electronically via TreasuryDirect.gov. They are nonmarketable, meaning they cannot be traded on secondary markets and can only be redeemed by the original purchaser or a designated beneficiary.

The new 4.03 percent rate continues a period of moderation following the historic surge in I bond yields seen in 2022. In May of that year, the Treasury set the composite rate at a record 9.62 percent, prompting a rush of investors seeking a safe and inflation-protected return during a period of soaring consumer prices. Since then, inflation has cooled, and I bond rates have steadily declined in tandem. Still, the combination of a stable fixed rate and the inflation-linked variable component has continued to attract long-term savers seeking diversification and safety.

The fixed rate is often considered a key determinant of long-term appeal. At 0.90 percent, it remains significantly higher than the near-zero levels that prevailed between 2020 and 2022, when the Federal Reserve kept interest rates low to support the economy during the pandemic. Analysts note that the fixed portion has become more attractive as real yields in Treasury Inflation-Protected Securities (TIPS) have stabilized, offering investors a modest hedge against inflation over time.

Simulating Composite Returns Under Various Inflation Scenarios

If inflation remains moderate, averaging around 2 percent annually over the next year, the variable component of I bonds would likely stay close to 3 percent, producing a composite yield in the range of 3.8 to 4.2 percent. Should inflation rise to 3.5 percent, as some economists expect if oil prices remain elevated, the composite rate could move closer to 5 percent in the next adjustment cycle. In a high-inflation scenario, such as a 5 percent annual increase in the CPI, I bonds could again yield more than 6 percent, reflecting their direct link to inflation data.

Conversely, if inflation falls below 1.5 percent, the composite rate could decline to between 2.3 and 3 percent, which would make I bonds less attractive compared to other fixed-income instruments like short-term Treasury bills or high-yield savings accounts. However, even in such a case, the fixed portion would ensure some minimal return above zero — an advantage over many inflation-protected instruments that can yield negative real returns during periods of low inflation.

Compared to Treasury Inflation-Protected Securities (TIPS), I bonds have several advantages for small investors. I bonds are free from price volatility because they cannot be traded on secondary markets, whereas TIPS fluctuate in price as market yields change. I bonds also offer tax deferral until redemption, whereas TIPS generate taxable income annually. However, TIPS allow for larger investments and can provide liquidity for institutional investors seeking exposure to inflation hedges within diversified portfolios.

As of mid-October 2025, five-year TIPS are yielding about 1.75 percent above inflation, while the 10-year yield stands around 2 percent. That suggests that I bonds, with their 0.90 percent fixed rate plus inflation, remain a competitive alternative for long-term, low-risk investors — especially those who value simplicity and tax advantages over secondary market flexibility.

Financial analysts generally view I bonds as most suitable for conservative savers looking for guaranteed, inflation-adjusted returns rather than speculative capital gains.

Overall, the Treasury’s latest adjustment to the 4.03 percent composite rate underscores the stability of I bonds as a core instrument in the government’s savings program. While the days of near double-digit yields from 2022 are long gone, I-bonds continue to offer a balance between inflation protection and safety, standing out as one of the few investment products that directly ties returns to the real cost of living in the U.S. economy.

Our business has been using PayPal for years. This week I received the first “email” from the CEO of the company. I mean for more than a decade, the CEO of PayPal has not directly written in any email our company has been included in this way. But this week, he made a case why merchants must plan for the future of agentic commerce. In other words, he considers the shift very important to sign that email. Read the note:

“Hello Ndubuisi Ekekwe,

The way people shop is changing fast. AI-powered agents are starting to help consumers discover and buy products in entirely new ways — and we want to make sure your business is ready to be part of it.

That’s why we are building PayPal’s new agentic commerce services — simple, powerful tools that make your products discoverable on leading AI platforms without extra setup or technical work. With just one PayPal connection, your store can appear across multiple AI shopping channels, while orders flow straight into your existing systems.

You’ll be able to accept payments instantly through PayPal, just like you do today — no new integrations or code required. Behind the scenes, our trusted and secure infrastructure takes care of everything from payment validation to routing, so you can focus on what matters most: your customers.

And through it all, your business stays your business.

You keep full ownership of your customer data — PayPal protects it.

You control your brand’s visibility and communication with every buyer.

You remain the merchant of record for every transaction.

We’re not here to replace your connection with customers — we’re here to help you reach more of them, faster.

This next chapter of digital commerce belongs to those who adapt quickly, and we’re making it simple for you to do just that. With PayPal as your partner, you can integrate once, reach everywhere, and grow confidently into the age of AI-driven commerce. Be the first to be a part of this exciting transformation and reach out to your PayPal account executives or visit our website today to sign up.

Thank you for choosing PayPal to power your business — we can’t wait to see what you do next.

Warm regards,

Alex Chriss

President and CEO, PayPal”

Tekedia Institute and our companies have joined the waitlist. With PayPal, you can register and pay for Tekedia Mini-MBA, AI Lab, etc while within ChatGPT, Google Gemini, and other ecosystems offered by Perplexity, Anthropic etc. Largely, the battle for conversational commerce and who will power the payment stack has started.

When small business owners need real-world advice, they rarely start with a sales pitch; they go straight to the people who’ve been there before. In the age of digital networking, Reddit has quietly become one of the most valuable forums for entrepreneurs seeking peer-to-peer insight on everything from software tools to employee management. Lately, one topic in particular has been dominating discussion threads: health insurance.

Owners are increasingly turning to community threads like Reddit Small Business Health Insurance Recommendations to share experiences, compare plans, and help one another navigate the maze of policies, premiums, and regulations that make health benefits such a complicated puzzle.

What makes Reddit unique is that it provides unfiltered, firsthand accounts of small business owners talking directly to each other without a sales agenda. This grassroots exchange of ideas is helping shape how entrepreneurs evaluate and select health insurance plans that fit their budgets and values.

The Rising Need for Peer-Driven Advice

Healthcare coverage is consistently ranked among the most complex and stressful aspects of running a small business. Between the Affordable Care Act (ACA), state requirements, and countless plan variations, even well-established owners find themselves overwhelmed.

Traditional routes such as consulting brokers or navigating online marketplaces often leave entrepreneurs with more questions than answers. While these resources can provide technical details, they rarely offer perspective on what actually works in practice for businesses of similar size and industry.

That’s where Reddit steps in. Communities like r/smallbusiness, r/entrepreneur, and r/insurance host active discussions where thousands of users dissect plan options, share cost-saving strategies, and warn each other about pitfalls. The advice isn’t sanitized or curated, it’s grounded in experience, often from people who’ve learned through trial and error.

Why Reddit Has Become a Go-To Resource

1. Transparency and Real-World Context

Unlike promotional websites, Reddit discussions tend to be candid and detailed. Business owners break down how much they pay per employee, which carriers are easiest to work with, and how customer service compares between insurers. The posts often include context, company size, industry, location, and employee demographics giving readers a sense of how applicable the advice might be to their own situation.

This level of transparency is rare in the insurance industry, where most marketing focuses on generalized claims about “affordability” or “coverage flexibility.” Reddit users replace that vagueness with hard numbers and practical tips.

2. Collective Problem-Solving

Threads like Reddit Small Business Health Insurance Recommendations function as collaborative problem-solving sessions. One user might post about rising premiums under a traditional group plan, while another suggests exploring a Health Reimbursement Arrangement (HRA) or joining a local business association that offers group rates.

In this way, Reddit becomes more than a place for opinions; it acts as a living database of crowdsourced knowledge, constantly updated by business owners facing the same challenges.

3. Accessibility and Anonymity

Discussing employee benefits can be sensitive, especially when it involves sharing financial details. Reddit’s semi-anonymous structure allows users to ask frank questions without fear of judgment or backlash. This openness leads to more honest conversations than one might have in a professional network or broker meeting.

Many users describe Reddit as the only place they feel comfortable admitting what they don’t understand about health insurance. That candor has created an environment where practical education flourishes.

Common Themes Emerging from Reddit Discussions

By examining the most popular small business health insurance threads, several consistent themes stand out:

1. Affordability Is the Top Concern

Nearly every discussion begins with cost. Owners share frustration over rising premiums and unpredictable rate adjustments. Many are looking for alternatives to traditional small-group policies, such as:

Level-funded plans, which combine aspects of self-funding and fully insured models.

Association health plans, allowing multiple small businesses to pool together for better rates.

Individual Coverage HRAs (ICHRA), which let employers reimburse workers for individual health plans rather than offering a group policy.

Reddit users frequently exchange recommendations for brokers or digital platforms that specialize in helping small companies evaluate these newer options.

2. Flexibility and Simplicity Matter

Small business owners wear multiple hats, and they often don’t have the bandwidth to manage complex benefits administration. Many Redditors emphasize the need for plans that are easy to understand, enroll in, and manage without requiring a dedicated HR team.

Plans that offer straightforward digital portals, responsive support, and clear billing structures earn consistent praise. Conversely, users warn against carriers known for confusing policies or sluggish claims processing.

3. Employee Retention Drives Decisions

While cost is a primary driver, many business owners acknowledge that offering decent health coverage is essential for keeping talented staff. Redditors discuss how even partial premium contributions or basic health stipends can make a major difference in morale and retention.

Some small firms opt for hybrid approaches combining traditional medical coverage with flexible benefits like wellness stipends or telehealth memberships. Others use HRAs to give employees freedom to choose their own coverage while controlling costs.

4. Regional Differences Shape Outcomes

Reddit discussions also highlight how dramatically insurance experiences vary by state. For instance, employers in California or New York often face different regulatory landscapes than those in Texas or Florida. Reddit’s large, geographically diverse user base helps business owners understand what’s normal in their area versus what might be a red flag.

The Power of Peer Validation

Photo by Hakim Menikh on Unsplash

One of Reddit’s greatest strengths is how it validates decision-making through collective experience. Small business owners can float an idea, say, switching from a small-group plan to an HRA-based model and immediately get feedback from others who’ve made the same move.

That peer confirmation builds confidence. Instead of relying solely on a broker’s pitch, owners can see how similar businesses have implemented the change, what obstacles they encountered, and whether employees reacted positively.

It’s a form of community-driven benchmarking that traditional consulting simply can’t replicate.

The Role of Brokers and Professionals Still Important

While Reddit is becoming an invaluable research tool, most users acknowledge that professional guidance remains essential. The best outcomes often come from combining community insights with expert help.

Brokers, financial planners, and benefits consultants can clarify legal details, ensure compliance with ACA and state laws, and tailor coverage to the company’s budget. The difference is that Reddit users now come to these professionals more informed, with pointed questions and clearer expectations.

This shift means the relationship between small business owners and advisors is becoming more collaborative and less dependent on one-sided sales conversations.

Real-World Examples Shared by Redditors

Several Reddit threads feature practical case studies from owners who’ve successfully revamped their health benefits:

A 12-person tech startup in Colorado switched from a group plan with unpredictable renewals to an HRA model that reimburses employees for individual ACA-compliant coverage. Result: stable costs and improved satisfaction.

A family-run retail business in Florida joined an industry trade group that negotiates collective health plans for members, cutting premiums by nearly 20%.

A remote-first design agency discovered that offering employees a monthly health stipend instead of formal coverage improved hiring outcomes, as it gave staff flexibility across multiple states.

These examples show how the best advice often comes not from marketing materials, but from other owners solving similar problems in real time.

The Broader Impact on the Health Insurance Landscape

The influence of Reddit’s small business discussions is extending beyond the platform itself. Brokers, insurers, and HR software providers are beginning to monitor these threads to better understand pain points and emerging needs.

Some carriers have even started simplifying language in their policies or developing digital tools that reflect the priorities echoed in these conversations: transparency, affordability, and ease of use. The grassroots discussions happening online are effectively reshaping how the insurance industry approaches the small business segment.

Balancing Community Insight with Due Diligence

Despite its value, Reddit isn’t a substitute for professional due diligence. Not every recommendation applies universally, and some advice while well-intentioned may overlook state regulations or tax implications. Business owners are wise to treat Reddit as a starting point for exploration rather than the final word.

That said, the platform’s impact can’t be understated. It has democratized access to knowledge that was once locked behind broker relationships or corporate jargon. For small business owners juggling multiple responsibilities, that’s a major win.

A New Way Forward for Small Business Health Coverage

As the cost and complexity of employee healthcare continue to rise, small business owners are finding power in collective experience. Platforms like Reddit provide something traditional channels rarely offer honesty, relatability, and empathy. The stories, numbers, and opinions shared by other entrepreneurs give real substance to what was once an opaque process.

Threads such as Reddit Small Business Health Insurance Recommendations represent a shift in how modern business owners make decisions. Instead of relying solely on sales-driven conversations, they’re turning to their peers for guidance rooted in experience and authenticity.

In the end, the best health insurance solution for a small business isn’t just about premiums or deductibles, it’s about confidence. And for many entrepreneurs, that confidence now begins not in an office meeting or a broker’s presentation, but in an online thread filled with honest, firsthand advice from others walking the same entrepreneurial path.