Right here when the Central Bank of Nigeria (CBN) pushed the banking sector recapitalization, and voided the use of bank profits as part of the paid-up capital requirements, I lamented that the process will make existing shareholders poorer, by diluting them, on the voyage of looking for “vapour” foreign investors or new funds. That policy made capital inefficient as the apex bank excluded retaining earnings. I was not happy about that, understanding the implications on existing investors.

If you read AO Lawal’s O’Level Economics textbook, he did not divide Capital into two forms when he explained Factors of Production. Yes, capital is capital, and should be treated that way, but when you begin to make capital to have tiers, you distort market equilibrium, and smart investors will punish you, especially in a public market.

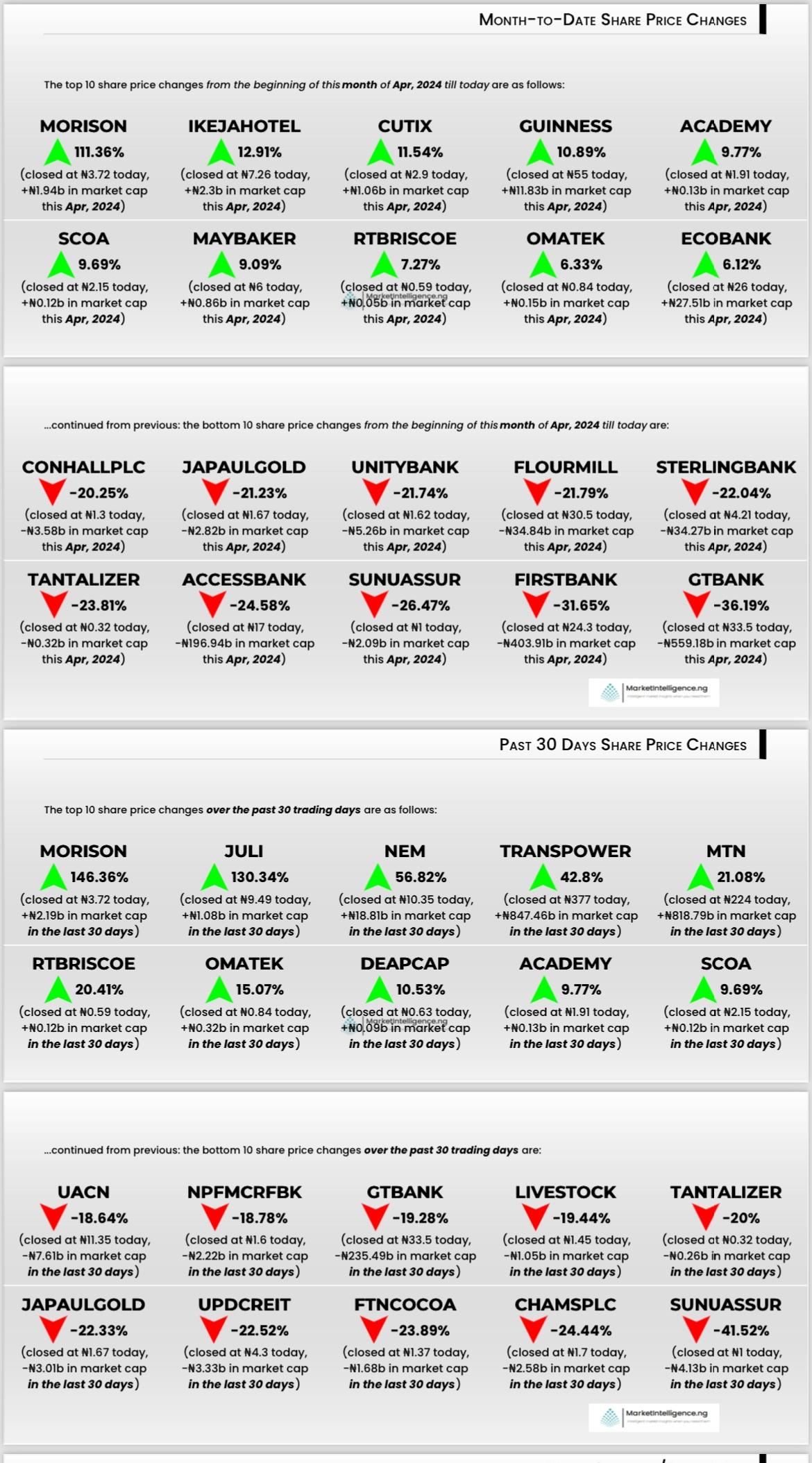

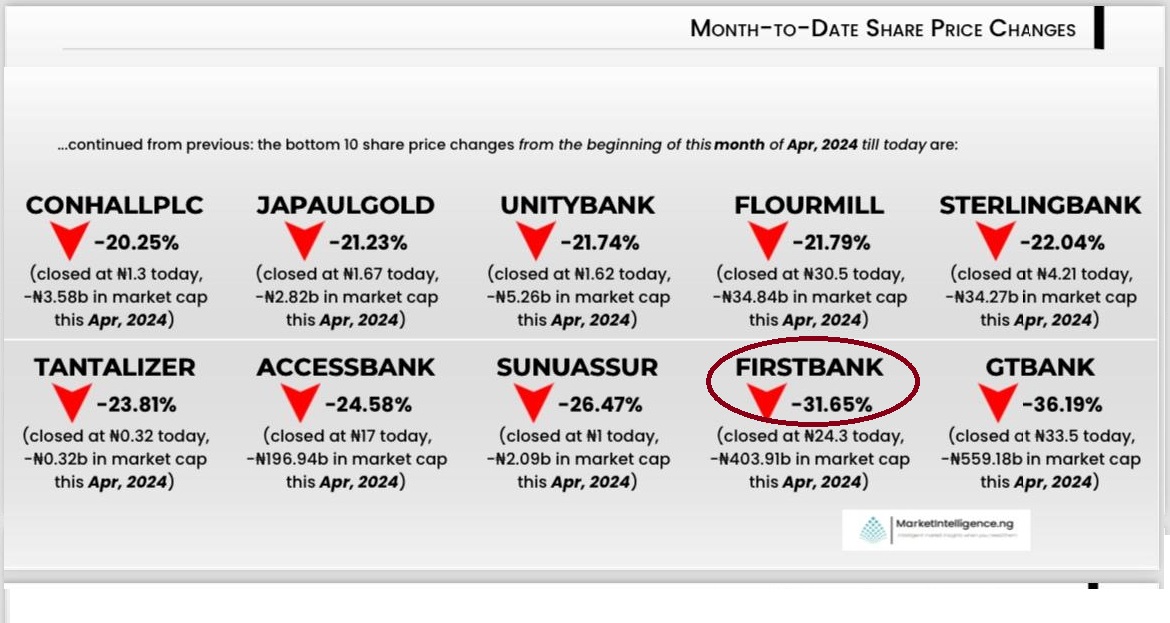

Since I dropped my note -”Bank Recapitalization In Nigeria Could Make Capital Inefficient Through Exclusion Of Retained Earnings “ on April 1, 2024, this is how some banks in Nigeria have performed (full report on click). I ended my April 1 2024 piece with a call: “I agree, this is a village boy, but I want someone to educate me why the retained earnings cannot be used for this playbook.”

Needless to add that no one explained that to my satisfaction. But today, investors have explained, and the report is a massive trauma on the valuations of banks in the Nigerian stock exchange (NGX). You can also extrapolate that the exit of FirstBank CEO could be linked to the loss of 31% of the company value since April 1, 2024!

My concern was also what investors saw: you do not punish existing investors because you want some “foreign investors” in London, New York, etc to come. Today, they have made way, and in the process, causing problems for the banks.

It is arrogant to tell investors that you cannot get dividends and the retained earnings cannot be used for recapitalization. In other words, they get nothing for their risks even as they’re being diluted!

Right here when the Central Bank of Nigeria (CBN) pushed the banking sector recapitalization, and voided the use of bank profits as part of the paid-up capital requirements, I lamented that the process will make existing shareholders poorer, by diluting them, on the voyage of… pic.twitter.com/xiTnHloVja

— Ndubuisi Ekekwe (@ndekekwe) April 21, 2024

Comment On Feed

Comment 1: Prof. Ndubuisi Ekekwe Though I am not an economist by profession, but with the little I learned about it, I will specifically state here that the implementation of the apex bank policy, particularly in the banking sector recapitalization, had profound implications for existing investors, notably in diluting their holdings and hindering the retention of earnings within the system. By restricting the use of bank profits as part of the paid-up capital requirements, the policy effectively marginalized existing shareholders, compelling them to navigate a landscape seeking foreign investors or new funds, often leading to a diminishment of their wealth and influence in the market.

This departure from conventional economic principles, as exemplified in AO Lawal’s O’Level Economics textbook, where capital is traditionally viewed as a singular entity within the factors of production, underscores a distortion of market equilibrium. Dividing capital into tiers not only deviates from established economic paradigms but also invites scrutiny and aversion from astute investors, particularly in public markets where transparency and stability are paramount.

Ultimately, the policy’s repercussions extend beyond mere financial ramifications…

Comment 2: Prof, you need to think about this like a Central Banker with a Financial Stability mandate. The best form of capital for a bank is Common Equity Tier 1 (CET1) Capital: This is the highest quality capital, consisting mainly of common shares and retained earnings. It is the most effective capital to absorb potential losses. In this case, the CBN decided to back out retained earnings to have an even better quality capital, given it is an accounting form of capital which has been subjected to principle-based assumptions (accounting principles). CBN’s focus is on the best possible capital base in the capitalization drive. It’s all about financial stability. I hope this helps.

Comment 3: Prof, I beg to differ markedly from your position. Using AO Lawal’s textbook published 4 decades ago to measure CBN’s decision in 2024 is rather inappropriate, respectfully. Financial management is not artificial intelligence, a lot is dependent on human factor which is highly dynamic and largely unpredictable. Yes AO Lawal never divided capital into many forms because of what was available then. 25 years ago Venture capital was largely nonexistent globally. Today venture capital is virtually the only source of capital for start ups.

History is the study of change, ironically used as a map for the future. Financial indexes hardly behave like electromagnetic waves whose direction are determined by movement of electrons.

The import of the scenario lies in the objective of what CBN wants to achieve, they need FDI in foreign currency. They should be encouraged to pursue their objective with zest.

If the govt policies are consistent and uncertainties are reduced to the barest minimum, they will succeed, however there is room for error. My take is that the govt should sync their policies with the CBN objective especially in dealing with insecurities.

My Response: There is no capital form you mentioned that was not around when Lawal wrote his book. Yet, you might not have gotten my message. I am simply saying: Naira is Naira, do not start saying this is from London or New York or Umuahia or Kano. If you start doing that, you will offend some people. CBN was doing that when it told banks: you cannot pay dividends, but go and get new investors, and after that you can do that. You know what? Those NEW investors will then partake in the dividends, created months before they joined. Read that piece again…