When the Central Bank of Nigeria (CBN) announced the policy of recapitalization of Nigerian banks, I noted that if these banks should go through rights issues, existing shareholders would lose value, as they would be diluted: “Rights issue will increase the number of outstanding shares even though the valuation has remained the same, thereby diluting current shareholders.”

As Nigerian banks begin the playbook on how to raise capital, investors are calibrating the implications of many moves. In the last few weeks, bank stocks have lost value in the Nigerian Stock Exchange (NGX). We have seen double digit percentage losses for most banks on their valuations. That is expected: if they plan to dilute, you can get out, with big returns, and then rejoin later.

For the low-tier banks, there is also going to be an issue of survival. In other words, the pressure will be huge on them to raise funds in a world of the big players.

Furthermore, there is another structural challenge. If banks raise these huge sums, they would be expected to inject them into the economy via loans and other product classes. As that happens, we can see increased inflation in the land.

So, the monetary policy of the apex bank which has been to curtail inflation via rate increases could be muted as banks release more funds into the economy to stay within standard ratios on loans and broad assets. Largely, investors are modeling that inflation will stay high over the long-term and are making changes on their portfolios.

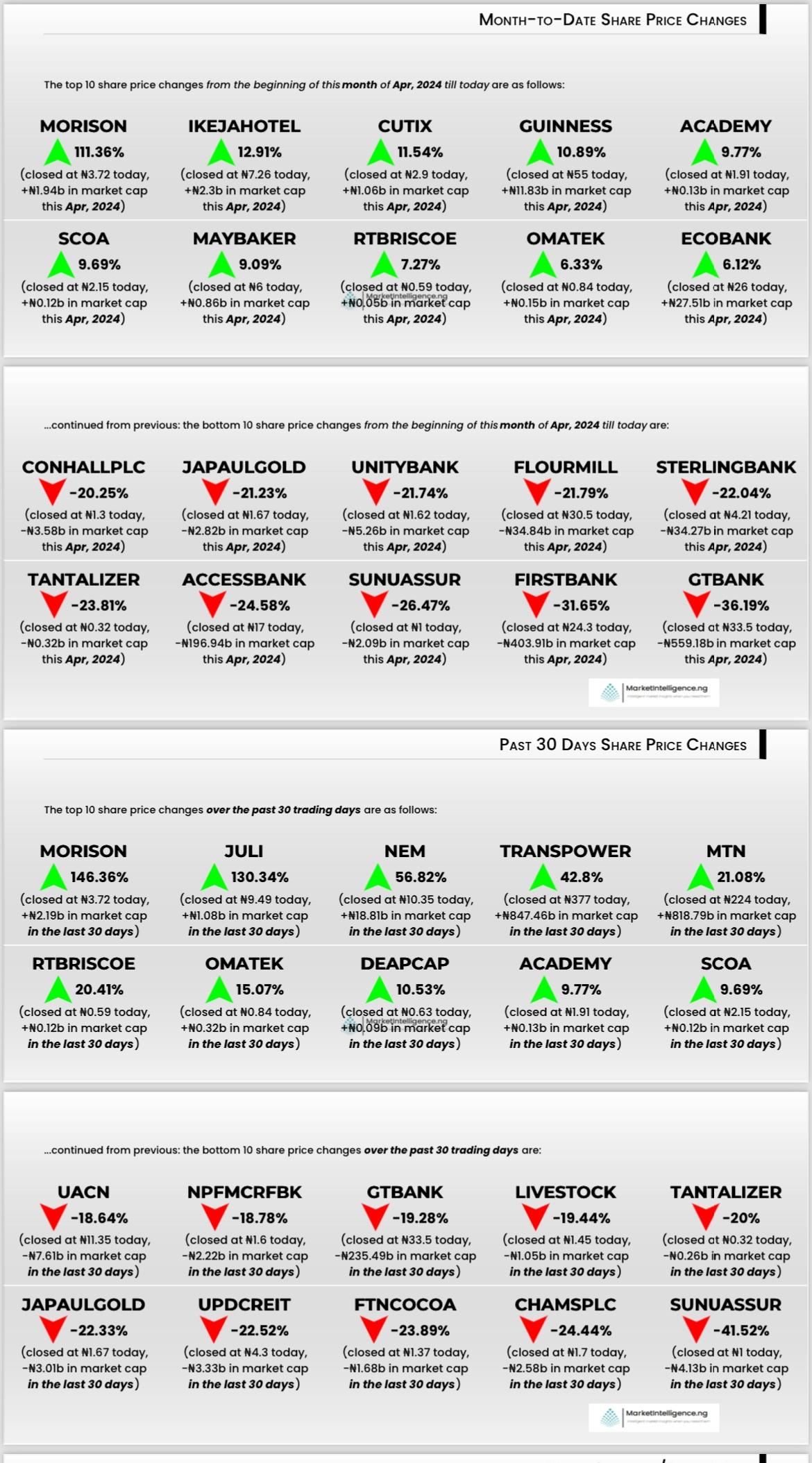

Full report here (PDF)

That said, if Naira remains STABLE irrespective of the exchange rate with US dollars, global investors will come. The instability of the Naira is more challenging to investors than its actual value in the mid- and long-terms. In the short-term, you focus on the exchange rate, but later, it is about stability. If Nigeria can get through Q3 2024 with a stable Naira, it will begin to rain again, not just for NGX players, but also startups!

Finally Nigeria needs to do all possible to ensure all the banks survive. Merging them does not really serve customers at the bottom that much, even as they support corporations which need banks with more capacities for loans. When Hallmark Bank, Citizens Bank and other regional banks folded in the Southeast, I have not seen replacements in what they were doing. So, my point is that we still need “small” commercial banks as their services remain catalytic.

When the Central Bank of Nigeria (CBN) announced the policy of recapitalization of Nigerian banks, I noted that if these banks should go through rights issues, existing shareholders would lose value, as they would be diluted: “Rights issue will increase the number of outstanding… pic.twitter.com/qOfS79qD1I

— Ndubuisi Ekekwe (@ndekekwe) April 21, 2024