Banks in Nigeria have received a directive from the Nigeria Interbank Settlement System Plc (NIBSS) to eliminate non-deposit-taking financial institutions from their NIP (NIBSS Instant Payment) fund transfer channels.

The affected entities include switching companies, payment solution service providers (PSSPs), and super agents. The NIP fund transfer channels encompass USSD, mobile banking apps, POS, ATMs, as well as web and internet platforms.

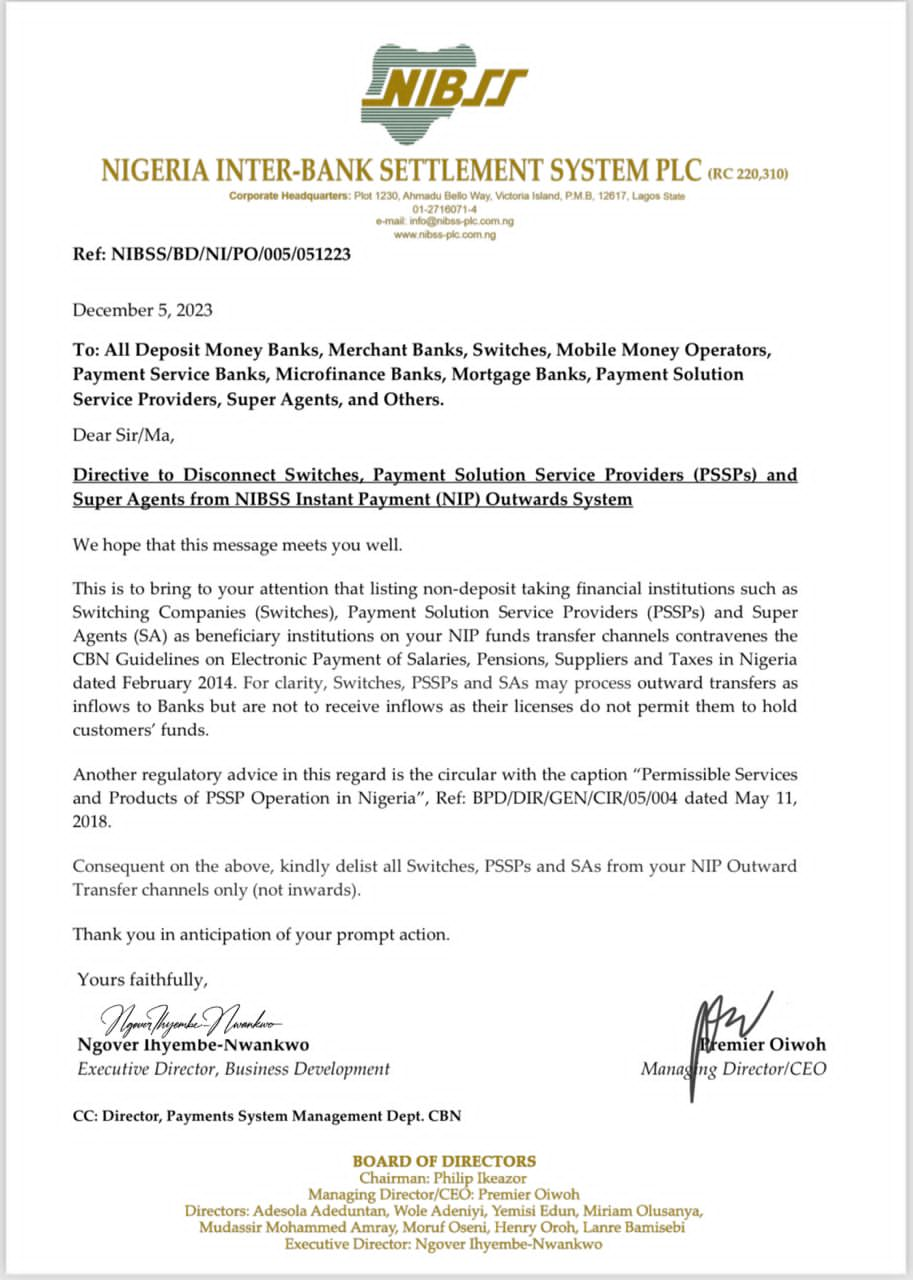

According to the circular issued by NIBSS, the inclusion of non-deposit-taking financial institutions as beneficiaries on NIP funds transfer channels violates the Central Bank of Nigeria (CBN) Guidelines on Electronic Payment of Salaries, Pensions, Suppliers, and Taxes dated February 2014.

The circular explicitly states, “listing non-deposit taking financial institutions such as switching companies (switches), Payment Solution Service Providers (PSSP), and Super Agents (SA) as beneficiary institutions on your NIP funds transfer channels contravenes the CBN Guidelines.”

However, the circular clarifies that while these financial institutions will be prevented from receiving inflows, they are permitted to process outflows as inflows to banks. It emphasizes that switches, PSSPs, and SAs may process outward transfers as inflows to banks but cannot receive inflows, as their licenses do not permit them to hold customers’ funds.

“For clarity, Switches, PSSPs, and SAs may process outward transfers as inflows to Banks but are not to receive inflows as their licenses do not permit to hold customers’ funds,” the NIBSS stated.

This action aligns with the New License Categorization of the Nigerian Payment System, which specifies that among various payment licensing categories—such as Switching and Processing, Payment Solutions Services encompassing Super Agent, PTSP, and PSSP—only MMOs, standing for Mobile Money Operators, are authorized to hold customer funds.

The enforcement of this policy will impact fintechs without banking licenses, requiring their removal from banks’ fund transfer channels. These platforms will still be able to facilitate outward transfers to banks but won’t be able to receive fund inflows.

While the directive is geared towards regulatory compliance and adherence to CBN guidelines, it may have consequences for small business owners who heavily rely on these fintech platforms for their financial transactions.

The expectation is that affected fintechs will swiftly pursue banking licenses to continue their operations without interruptions. Hence, fintech companies aiming to provide specific deposit-taking services may opt for Microfinance Banks (MfBs), while larger entities such as telecommunications companies choose Payment Service Banks (PSBs) if they intend to offer such capabilities.

Several fintech companies such as Opay, PiggyVest, and Flutterwave, who are not affected by the new directive, have quickly issued statements to allay the fears of their customers.

OPay: “We wish to state that OPay is not affected by the recent circular published by NIBSS. The focus is on Payment Service Solution Providers, Switches and Super Agents. OPay is a Mobile Money Operator (MMO) licensed by the CBN and insured by the NDIC. Your funds are safe and secure with OPay.”

We wish to state that OPay is not affected by the recent circular published by NIBSS.

The focus is on Payment Service Solution Providers, Switches and Super Agents.

OPay is a Mobile Money Operator (MMO) licensed by the CBN and insured by the NDIC.

Your funds are safe and…

— OPay (@OPay_NG) December 7, 2023

Piggyvest: “Hi guys! Kindly note that Piggyvest is not affected by the recent NIBSS circular. Please disregard the misinformation. All Piggyvest virtual account numbers are provided by our licensed partners and do not fall into any of the listed categories. Your funds remain safe.”

Hi guys!

Kindly note that Piggyvest is not affected by the recent NIBSS circular. Please disregard the misinformation.

All Piggyvest virtual account numbers are provided by our licensed partners and do not fall into any of the listed categories.

Your funds remain safe. ?

— PiggyVest (@PiggyBankNG) December 7, 2023

Paystack: “Hi team, we wanted to reassure you that the recent NIBSS circular does not impact Paystack-Titan or any other Paystack services. We developed Paystack-Titan in partnership with Titan Trust Bank in a way that allows the service to operate compliantly, and it passed review from NIBSS.”

Hi team, we wanted to reassure you that the recent NIBSS circular does not impact Paystack-Titan or any other Paystack services.

We developed Paystack-Titan in partnership with Titan Trust Bank in a way that allows the service to operate compliantly, and it passed review from…

— Paystack (@paystack) December 7, 2023

PocketApp: “Hello, Following the recent NIBSS circular, kindly note that PocketApp is a Mobile Money Operator duly licensed by the CBN under Abeg technologies. Our virtual account numbers are provided by licensed bank partners and they do not fall into any of the categories listed by NIBSS. Rest assured, your funds remain safe.”

Hello,

Following the recent NIBSS circular, kindly note that PocketApp is a Mobile Money Operator duly licensed by the CBN under Abeg technologies.

Our virtual account numbers are provided by licensed bank partners and they do not fall into any of the categories listed by…

— PocketApp (@getpocketapp) December 7, 2023

Flutterwave: “The recent NIBSS circular has ZERO impact on our services because we are not deposit-taking like a bank. We are a licensed Switching and Processing company & an International Money Transfer Operator – this means our services remain unaffected, and we will continue to deliver best-in-class excellence to you, our customers. We are connected to NIBSS for the purpose of outward money transfer in Nigeria. Rest assured, we are open for business as usual!”

The recent NIBSS circular has ZERO impact on our services because we are not deposit taking like a bank.

We are a licensed Switching and Processing company & an International Money Transfer Operator – this means our services remain unaffected, and we will continue to deliver…

— Flutterwave (@theflutterwave) December 7, 2023

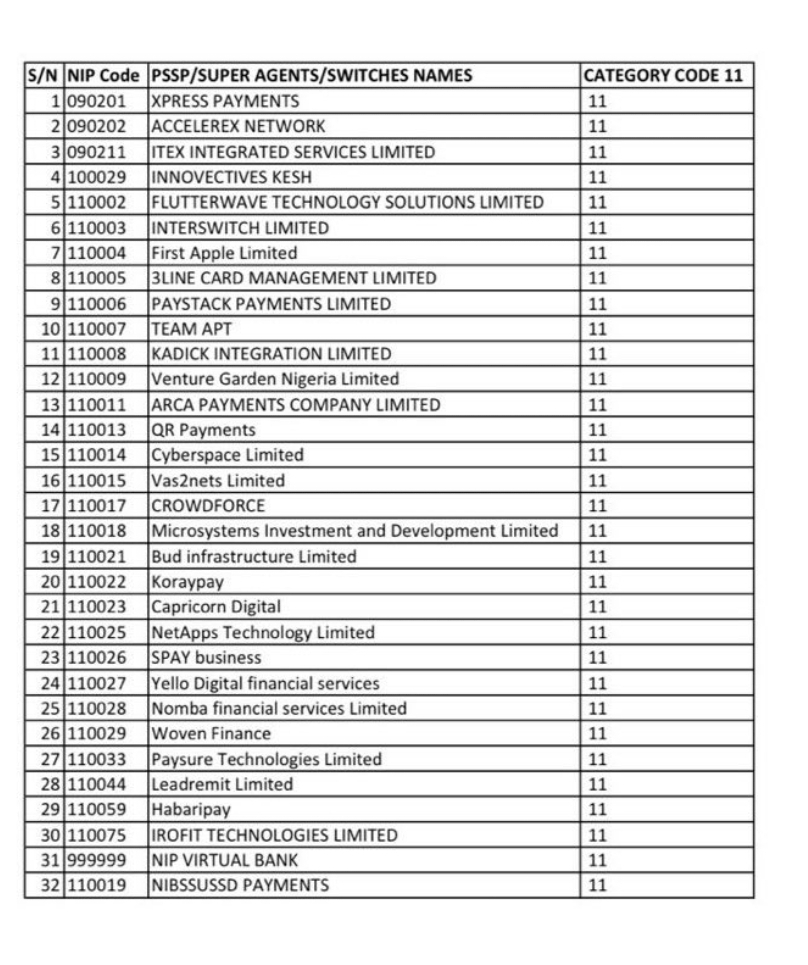

The affected fintechs are listed below: