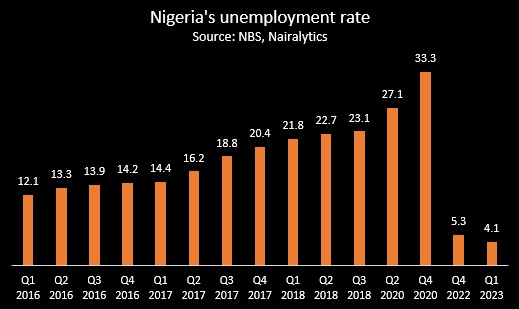

The National Bureau of Statistics (NBS) said Nigeria’s unemployment rate decreased to 4.1 percent during the first quarter (Q1) of 2023, down from the previous quarter’s 5.3 percent.

Back in the fourth quarter (Q4) of 2020, the bureau reported the country’s unemployment rate to be 33.3 percent.

In a statement released on Thursday, the NBS announced that the recent unemployment report employed a new methodology and provided a comprehensive examination of the labor market.

“The latest Nigeria Labour Force Survey (NLFS) report sheds light on the dynamics of labor market within the country,” the statement reads.

“This report covers the fourth quarter of 2022 and the first quarter of 2023, presenting an in-depth analysis of key labor market indicators such as employment, including unemployment rates, underemployment rates, hours worked, and informal employment.

“The revised methodology aligns with our contemporaries in Africa such as Ghana, Niger, Chad, Cameroon, Benin, Gambia etc, in line with international best practices.”

UNEMPLOYMENT RATE MOVED FROM 5.3% to 4.1% IN THREE MONTHS

The latest report from the NBS indicates that Nigeria’s unemployment rate stood at 5.3 percent during Q4 2022 and then declined to 4.1 percent in Q1 2023.

According to the agency, these figures are in line with rates seen in other developing nations where engaging in work, even in low-productivity roles for only a few hours, is vital to sustaining livelihoods, especially in the absence of any social safety nets for the unemployed.

The bureau also stated that the revised methodology now defines employed individuals as those who work for pay or profit and have worked for a minimum of one hour within the past seven days, as opposed to the previous criterion of 40 hours.

“The old methodology placed a range on the working-age population- 15 – 64 years, while considering working hours between 20-39 hours as underemployment, 1-19 hrs as unemployment,” the statement reads.

“In addition, subsistence agriculture and temporary absentees from employment work were not properly represented as well as the absence of mutually exclusiveness of unemployment and employment.

“These improvements, among others, captured in the revised computations will make Nigeria’s Labour Force data comparable with other countries.”

UNDEREMPLOYMENT MOVED FROM 13.7% to 12.2% in THREE MONTHS

The NBS defines the underemployment rate as the proportion of employed individuals working fewer than 40 hours per week while expressing willingness and availability to work more. This rate was recorded at 13.7 percent in Q4 2022 and reduced to 12.2 percent in Q1 2023.

The report highlights that the rate of informal employment, which includes agricultural work among employed Nigerians, was 93.5 percent during Q4 2022 and decreased to 92.6 percent in Q1 2023.

The NBS’s NLFS also indicated that approximately three-quarters of Nigerians within working age were gainfully employed. In Q4 2022, this rate stood at 73.6 percent, and in Q1 2023, it rose to 76.7 percent. This underscores that a majority of individuals were engaged in some form of job, involving at least one hour of work per week for compensation or profit.