Artificial intelligence has become one of the most discussed topics in marketing communications. Scroll through LinkedIn today and it becomes clear that marketing leaders are no longer debating whether AI matters. They are discussing how to use it effectively, responsibly, and strategically. Yet beneath the excitement lies a more important conversation about the changing nature of marketing itself.

An analysis of thought leadership posts shared by marketing and communications professionals reveals a remarkably consistent narrative. Rather than portraying AI as a replacement for marketers, industry leaders overwhelmingly frame it as a tool that amplifies human capability. The emerging consensus is that the future of marketing will not be determined by artificial intelligence alone, but by the ability of organisations to combine technological capability with distinctly human strengths.

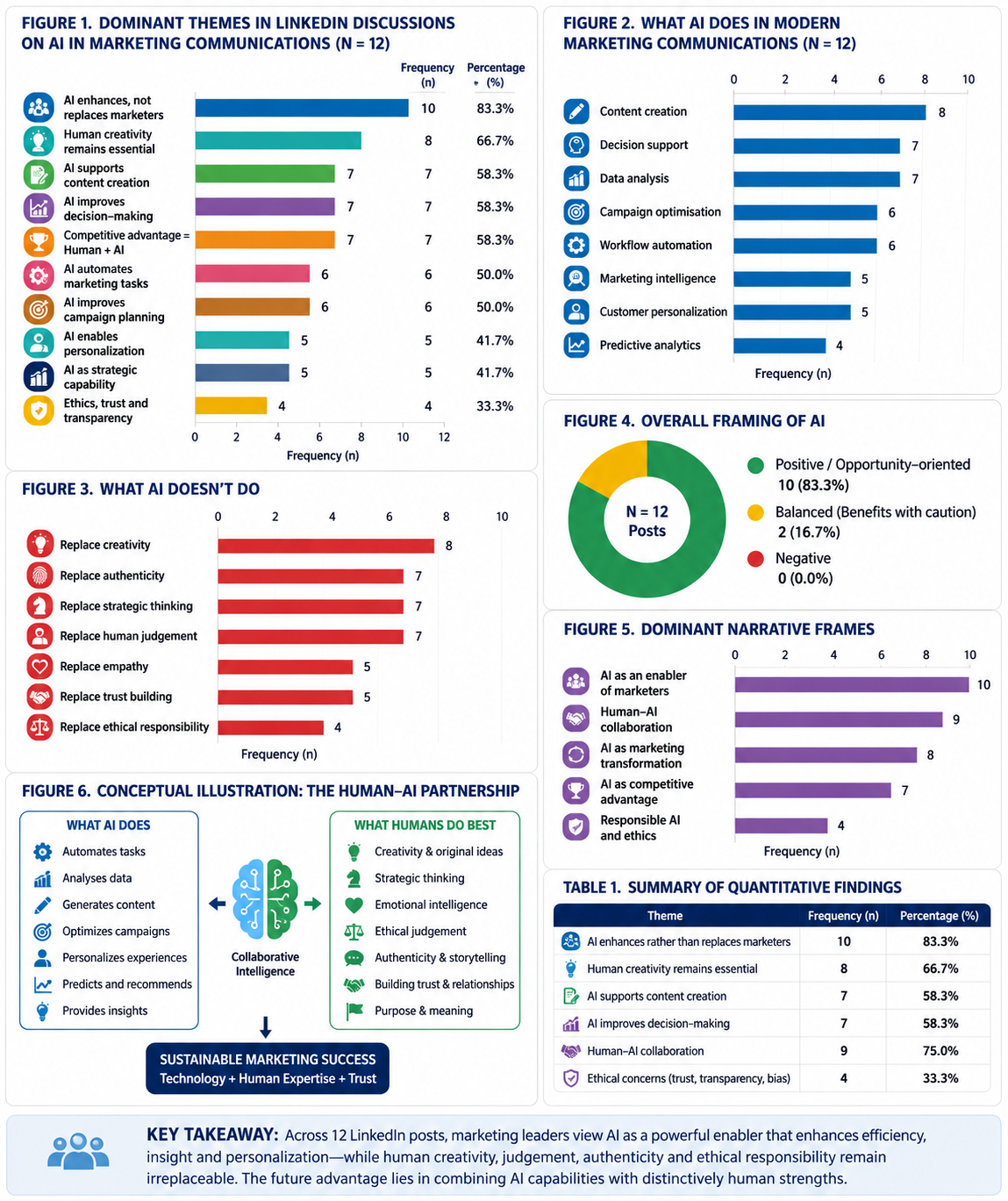

Across the discussions, AI is consistently associated with operational excellence. Marketing professionals describe it as a powerful assistant capable of generating content ideas, drafting social media posts, optimising advertising campaigns, analysing vast quantities of customer data, automating repetitive workflows, and personalising communication at scale. These capabilities are transforming everyday marketing activities by reducing the time spent on routine tasks and enabling faster decision-making.

However, the conversation does not end with efficiency. Almost every contributor establishes clear boundaries around what AI cannot do. While algorithms can generate words, images, recommendations, and predictions, they cannot replace authenticity, empathy, ethical judgement, strategic thinking, or lived human experience. These qualities remain central to building meaningful relationships between organisations and their audiences.

This distinction reflects an important shift in how the marketing profession understands technology. Earlier waves of digital transformation often focused on replacing manual processes with automated systems. Today’s discourse is different. AI is increasingly viewed as an augmentation technology rather than a substitution technology. Its primary role is to strengthen human decision-making rather than eliminate it.

This emerging perspective also challenges one of the most common misconceptions surrounding artificial intelligence. Simply adopting AI does not create competitive advantage. Several marketing leaders argue that AI has quickly become a baseline capability, much like search engines, customer relationship management systems, or social media platforms before it. As AI becomes embedded in everyday workflows, access to the technology itself will no longer differentiate organisations. Instead, competitive advantage will come from how effectively businesses integrate AI into broader marketing strategies, organisational culture, and customer experience.

The discussions also highlight an important evolution in the role of marketing leaders. Historically, marketers were expected to create compelling campaigns and manage brand visibility. Increasingly, they are becoming orchestrators of intelligent systems that combine automation with human insight. AI can identify patterns within customer behaviour, predict market opportunities, and optimise campaign performance, but it cannot determine organisational priorities or define a brand’s purpose. Those responsibilities remain firmly within the domain of leadership.

Perhaps the most compelling aspect of the conversation concerns trust. Several contributors express concern that the rapid adoption of AI-generated content may blur the line between authenticity and manipulation. As artificial intelligence becomes more capable of producing convincing text, images, and personalised communication, marketing professionals are recognising that transparency is becoming just as important as innovation.

Consumers may appreciate faster responses and more relevant content, but they continue to value honesty, credibility, and genuine human connection. This suggests that the future role of marketing communicators will extend beyond content production to include ethical stewardship. Building trust in an AI-enabled marketplace will require organisations to establish clear principles for transparency, accountability, and responsible communication.

Another notable insight from the LinkedIn discussions is the rejection of technological determinism. Rather than viewing AI as an unstoppable force that inevitably replaces human expertise, contributors consistently portray it as a decision-support system. AI can analyse millions of data points in seconds, uncover hidden patterns, and recommend actions based on predictive models. Yet interpreting those insights, balancing competing priorities, and making strategic decisions remain uniquely human responsibilities.

This perspective is particularly important because it redefines professional value. The marketers who will thrive are unlikely to be those who simply know how to operate AI tools. Instead, they will be those who understand customers deeply, communicate authentically, think strategically, and use AI to strengthen rather than substitute those capabilities.

Specifically, the LinkedIn conversation reflects a profession that is adapting rather than resisting. Marketing communicators recognise that artificial intelligence is becoming part of the industry’s infrastructure, but they also understand that technology alone cannot build relationships, inspire confidence, or create lasting brand loyalty.

The real transformation is therefore not about machines replacing marketers. It is about marketers evolving into more strategic professionals who use AI to enhance creativity, improve decision-making, and deliver greater value. In that future, artificial intelligence may accelerate marketing, but it is human judgement, empathy, and authenticity that will continue to define successful communication.