The year 2020 was challenging for the world not only because of the global pandemic but also due to a wide array of cybersecurity challenges we faced.

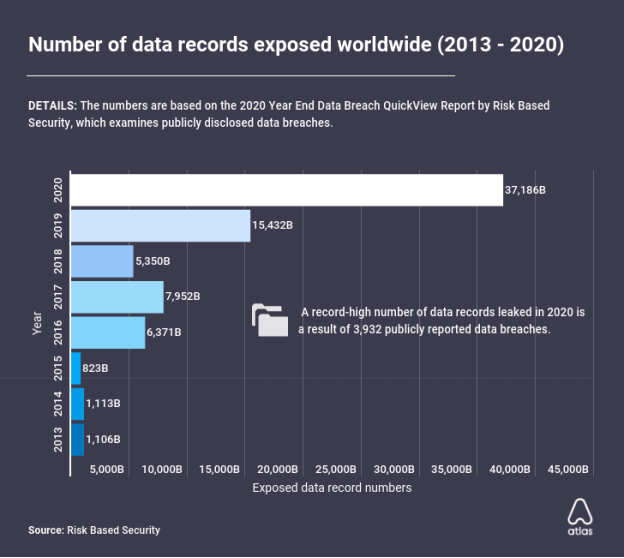

According to the data analyzed by the Atlas VPN team based on the 2020 Year End Data Breach QuickView Report by Risk Based Security, the number of leaked data records worldwide hit a whopping 37 billion in 2020. It is a 140% increase from 15 billion records in 2019.

The majority — 82% or over 30 billion of data records — were compromised in only five major breach incidents. All of them were a result of misconfigured databases or services.

The most commonly exposed type of data were names, leaked in 46% of data breaches last year. Next up are email addresses, which were compromised in 32% of incidents.

While leaked records reached never-before-seen highs in 2020, the number of actual data breaches shrank by 48%. It went down from 7,553 breaches in 2019 to 3,932 in 2020.

In total, 77% of data breaches last year were caused by outside actors, 16% by insider threats, while the rest is unknown. What is more, 676 breaches last year included ransomware as an attack element — a 100% rise compared to 2019.

The healthcare sector suffered the most

The year 2020 posed many cybersecurity challenges for companies around the world. However, some sectors were affected more than the others.

Last year was certainly hard on the healthcare industry, which dealt with more data breaches than any other sector. In 2020, the healthcare industry faced 484 hacks, which account for 12% of all last year’s breaches.

The information sector was also highly targeted. It suffered 429 hacks, which made up 11% of data breaches last year.

Rounding out the top three industries in terms of data breaches last year is the finance and insurance sector. In 2020, the industry faced 382 hacks — 10% of last year’s breaches.

Rachel Welch, COO of Atlas VPN, shares her thoughts on the rapidly evolving cybersecurity landscape:

“All in all, the year 2020 has taught us that it is hard to predict what the future holds for cybersecurity. In a single year, breached data files more than doubled, reaching record-high numbers, as did the number of hacks that included a ransomware component.

However, there were fewer actual data breaches reported. It suggests that data breaches are growing in severity, with fewer incidents exposing more personal information than ever before.”

Join me, the Governor of Central Bank of Nigeria (Godwin Emefiele), the Vice President of Federal Republic of Nigeria (Prof Yemi Osinbajo), Chairman of Afreximbank (Prof Okey Oramah), Prof Olawale Sulaiman, and Hon Abike Dabiri-Erewa, on March 06, as we discuss the new CBN policy and more.

Saturday, March 06, 2pm WAT – register free and join us.

Goldman Sachs anoints Bitcoin as it opens a cryptocurrency desk: “Goldman Sachs Group Inc has restarted its cryptocurrency trading desk and will begin dealing bitcoin futures and non-deliverable forwards for clients from next week, a person familiar with the matter said.” As the US banking giant readies the playbook, it is exploring a bitcoin exchange traded fund (ETF) and has issued a notice to explore digital asset custody, Reuters reports

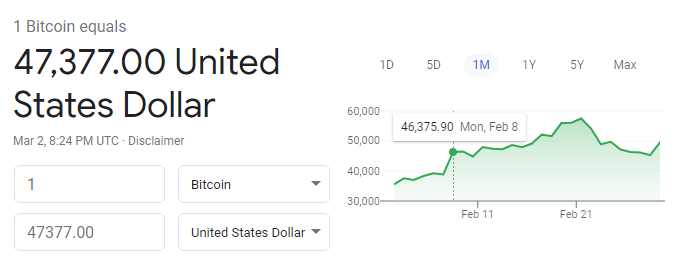

While its price has risen significantly over the past year, bitcoin remains highly volatile. The virtual currency smashed through $58,000 on February 21 then fell back by as much as 25% but has recovered some lost ground.

This makes the coin and related derivatives attractive for investors willing to take riskier long or short positions as they hunt for yield in a record-low interest rate environment.

Non-deliverable forwards are a type of derivative that allows investors to take a view on bitcoin’s future price.

Watch out, with the freezing of this asset class in Nigeria, and the government making sure that its young people, who are already ecosystem players, become spectators, and in five years, Nigeria will ask GS to manage a part of our foreign earnings within its cryptocurrency desk. The reason would be: no company in Nigeria can do that for Nigeria and we have to hire Goldman Sachs.

Yet, I expect the government to reverse course before the end of Q3 after they have studied the sector. What will happen is that Nigeria will regulate it but allow young people to participate in the sector.

In 2018, the Association of Facilities Management Practitioners of Nigeria (AFMPN) birthed after several years of consultation with the key stakeholders in the industry and government officials at the Federal level. It was on Wednesday 27th June, 2018 at Onikan City Mall that practitioners and key players gathered for the announcement of the association.

Analysing the event, the gathering indicates that the rapid growth of the industry valued at less than $1 billion is no longer far, but near. While introducing the association, Paul Erubami one of the Chief Executive Officers of key players in the industry says: “This association will work with the various stakeholders, affiliate associations, similar bodies, associated international bodies among others to achieve the core purpose. We will liaise with similar professional bodies and academic institutions towards the development of the right skills and knowledge for the industry’s growth.”

Collins OsayamwenPaul Erubami

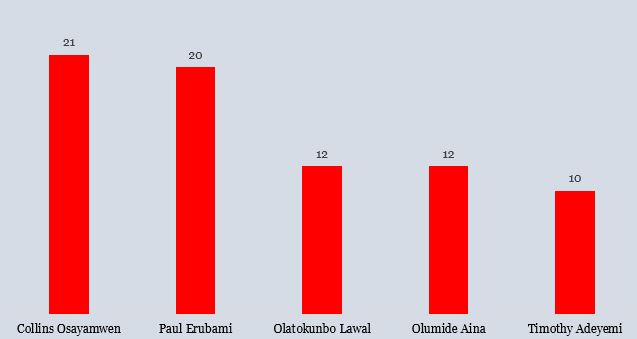

Some days ago, Mr Collins Osayamwen was elected as the first president of the young association. Mr Paul Erubami became the deputy president while Mrs Olatokunbo Lawal, Mr Olumide Aina and Mr Timothy Adeyemi were elected as Directors of Finance and Administration, Membership and Professional Development, and Marketing Communication & Public Relations respectively.

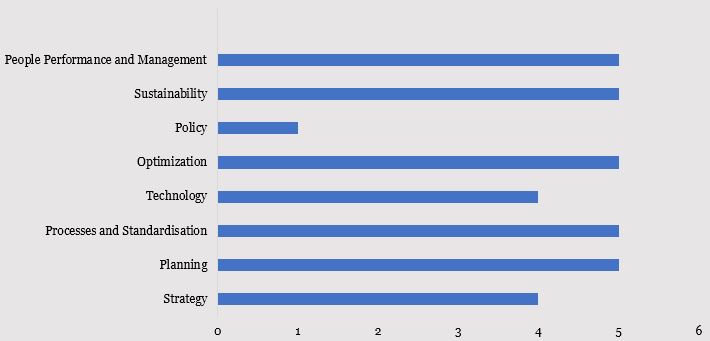

These executive members have varied years of experience from different positions. Analysis of the years of experience indicates that they have 15 years as average, while they have 75 cumulative years of experience. Our analyst notes that this is laudable for an emerging industry that needs radical development with sustainable innovations in the areas of collaboration, knowledge acqusition and development.

Exhibit 1: Years of Experience

Source: Infoprations Analysis, 2021

Mapping and analysis of the core features in experiences of the elected members indicate that people performance and management, processes and standardization, planning, sustainability and optimization are likely to be the early core benefits the members and players in the industry would derive from the elected executives.

Available information reveals that Mr Collins Osayamwen have cognate experience in the areas of processes and procedures standardisation. This was gleaned from his fellowship and membership of national and international organisations responsible for institutionalisation of best local and global practices. His strengths, according to our analyst, would be further strengthened with over 20 years of experience in consulting and training across multiple sectors and across many countries in Africa of Mr Paul Erubami,a licensed IFMA instructor on FMP, CFM, SFP and other programmes.

Process and people transformation prowess of Mrs Olatokunbo Lawal, the Chief Executive Officer of Wilco, would be a great addition. Industry and academic teaching experience of Mr Olumide Aina are expected to be added value to the association. With his election, our analyst notes that the association should be able to have a number of strategic partnerships with academic institutions.

The evolution of bitcoin has created a new market in Africa. The biggest economies in the continent, Nigeria and South Africa are at the helm of the boom, which is showing a lot of young people a way out of unemployment.

It is more like a fulfillment of the 2018 United Nations’report, which predicted that Africa could be the next frontier for cryptocurrency due to poor governments’ fiscal policies and regulatory bottlenecks that pose a challenge to economic growth in the continent.

While Nigeria leads the African crypto market, South Africa is trailing with a ground-breaking volume of transactions.

Apart from its 32.5% unemployment rate, South Africa is a country where the majority of the population is unbanked, creating the opportunity for more people to embrace bitcoin not only as a way of transaction, but also as means of employment.

For the past five years, the South African cryptocurrency market has evolved to become one of the leading peer-to-peer marketplaces in the world. South Africa processednearly $100 million in P2P bitcoin exchange in 2020, opening opportunity for further investment in 2021.

BTC has been volatile recently

The growth has been spurred by many factors, including flexible payment systems, cross border trade, currency fluctuation and fair regulation.

Before now in South Africa, cross-border financial transactions were expensive, rigorous and unreliable, even within the Southern African Development Community (SADC) bloc. Across the continent, the complexity was limiting business transactions and frustrating Small & Medium Enterprises (SMEs) and other markets.

Then there’s currency fluctuation. The South African rand is one of the most volatile major currencies in the world. Since 2014,it has lost 30% of its value as the economy wobbles.

Another factor fueling the surge of bitcoin in South Africa is theAfrican Continental Free Trade Area (AfCFTA), a bloc idea born in 2012 and signed in July 2019 to facilitate intra-African trade. So far, more than 30 countries have ratified their instrument, which means there is anticipation of increased cross-border trade within Africa that will need flexible means of financial transactions.

In addition, seeing where the world is headed with digital payments, the South African Reserve Bank has established a team of players from the financial sector, including stakeholders in the cryptocurrency industry, tasked to develop a regulatory framework for the industry.

These factors have spurred significant growth in the South African bitcoin market, stoking the interest of many who are joining the trend daily.

However, as interest grows in the South African Cryptocurrency market, challenges remain. In January, South African financial sector regulator, the Financial Sector Conduct Authority (FSCA)requested more oversight power to regulate cryptocurrencies in order to be able to prosecute fraudsters in the industry.

FSCA made the request after Mirror Trading International (MTI), a bitcoin trading club, was accused of a $740 million bitcoin scam, conducting operations illegally and lying to investors. The regulator shut MTI down in December due to the enormity of the fraud allegations leveled against it. The club was, among other acts of fraud, accused of falsifying trade statements and did not declare losses after promising customers daily returns of 0.5% for $100 deposit.

It has been the biggest scandal in the South African cryptocurrency market, and set a trajectory that would have scared traders off the market if not that many exchanges have established good reputations that withstood the scandal.

“Mirror Trading International is another example of why the industry must spread the word that algorithmic trading platforms promising unrealistically high returns are nearly always scams,” data firm, Chainalysissaid.

“When cryptocurrency exchanges and other services learn of these scams and receive their cryptocurrency addresses, they should discourage users from sending funds to those addresses or at least warn them that financial losses are highly likely,” it added.

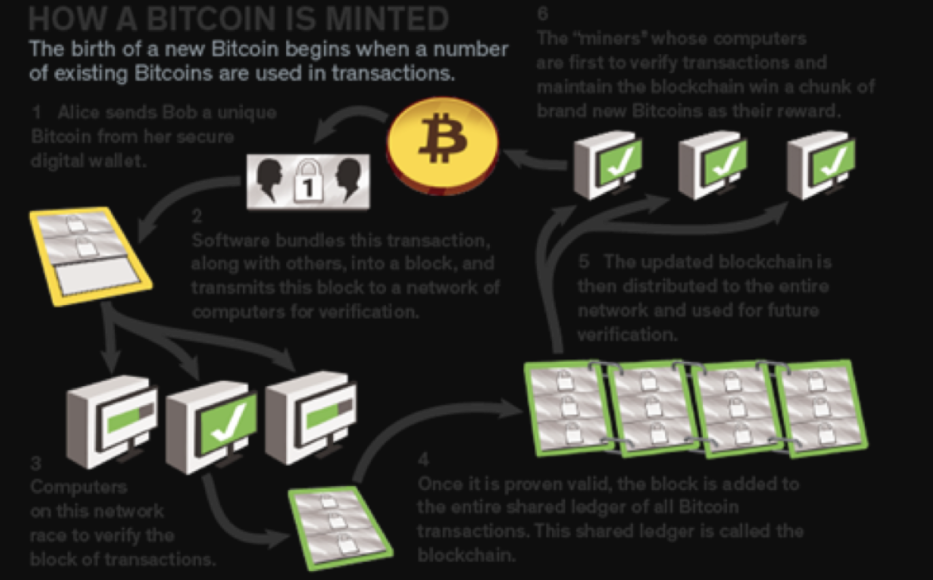

How Bitcoin is minted

Despite these pitfalls, the South African authorities have taken a different approach from their Nigerian counterparts, who inFebruary 5 announced the ban of cryptocurrency exchanges’ operations. The South African regulators are poised on regulating existing exchanges to give credibility to the industry.

But due to the scandal, the exchanges, including peer-to-peer (P2P), a decentralized platform whereby two individuals interact and transact directly with each other, without the need of a middleman to broker the deal, have come under the radar of both regulators and traders.

Against this backdrop, the South African bitcoin market is set for full regulation aimed at curtailing fraud practices. This means that all the exchanges including P2P platforms being used in South Africa will have to undergo credibility verification.

The FSCA has proposed stringent regulations that will mandate crypto startups to obtain a financial services provider (FSP) or cease operations. But there is more to it that has thrown the market into disarray. Under the proposed regulation, taxpayers are required to disclose all crypto-related transactions to South African Revenue Service (SARS), or face a penalty that may involve a two-year jail term.

As a result of this proposed regulation, the South Africa’s daily bitcoin transaction volume plunged 10%, from $258,783 to $235,470 in January; as many traders began to withdraw their investment.

The proposed tax rule will undermine the autonomy of cryptocurrency in South Africa, spooking investors as they wouldn’t want to operate in a market where the government is interfering with transaction autonomy.

Although the South African authorities claim their aim is to sanitize the cryptocurrency market through regulation, the proposal is suggesting that the government wants a share of the bitcoin boom.

SARS had earlier proposed capital gains tax (CGT) on crypto investments that would require traders paying from 7% to 18% tax on profits made, another development crypto traders don’t want to reckon with.

Generally, the growth of the cryptocurrency market both in Nigeria and South Africa appears partially dependent on the regulatory policies of both governments. For this reason, exchanges have been innovating to keep the market flow going through P2P platforms where the authorities have no control.

Local Bitcoin, a Finland-based exchange is among the many stepping up to fill the void that would be created by the South African regulatory proposal if approved.

With a P2P platform that supports hundreds of different payment methods, Local Bitcoin has become one of the most established crypto exchanges in the world; offering escrow-secure P2P services that gives traders a sense of security. It also wades in when there is dispute between traders and provides all parties with deserving resolution.

Although recent happenings have thrown the South African bitcoin market into a state of distrust, resulting in government’s intervention that is currently slowing the market’s growth, credible exchanges are fighting through secure and transparent transactions to protect the market.