In Africa, I have learnt that big press release rarely moves growth. Growth is not a one-time event. That is where it becomes challenging. Yes, you have built the product, ran some press releases and now you are waiting for sales to take-off. Nothing happens. You have paid Google and Facebook for adverts, waiting for the bank accounts to respond, nothing happens. This part of the world is different; you cannot hack growth as they do in America because hacking the pockets of Nigerians (and Africans in general) is tough. Yes, when the average income per day is $2, it is harder to find money in that pocket even when you have hacked into it!

[…]

One way to make growth happen is to have a system that actually measures growth. Until you have a clear desired growth target, you would be unable to mobilize the required resources to make it happen. Without measurement and pursuit of targets, everything becomes guesswork, a simple pendulum or rollercoaster with no clear deliverable expectation.

[..]

Pulse: Facebook created a position for Vice President of User Growth, ran by Chamath Palihapitiya, now the CEO of Social Capital. According to Chamath, they realized at the early phase of Facebook that having many users in Facebook was the most important feature in the business. In other words, despite any engineered feature, if there were no people in Facebook, no one would have cared. So, to give users the best feature – having their friends, families, etc there – Facebook formed a growth group which does nothing but work out mechanisms to bring people to use Facebook. Until you can measure and work on things that matter, top-grade execution will not happen.

When you are growing, you are executing well, and one key thing here is that more people will like to come and work with you. In a big company, your unit will begin to attract top talent and in a start-up, more quality talent will begin to apply. Where there is no momentum – i.e. the execution is stunted – visions fade and paralyses emerge: a tribe of believers is lost, not just in the firm but also in the market. If the workers do not see any momentum, doubts set in and customer relationships will become secondary as everyone will be updating his or her CV more. Suddenly, the business that was attracting great talent is now struggling to keep those it wants to keep in-house.

Growth happens when there is a great product to sell. No other trick can work, and anything else will fade over time. So, the summary is this: Make Great Products That Wow Customers.

Culled from Week 2 of Tekedia Mini-MBA Lecture Materials. You can still join us here by registering via the options provided here.

We are happy to note that all partners we have qualified can now place bulk orders to serve their retail customers for the following products: Zenvus Loci Mini, Zenvus Loci Max, Zenvus mLoci, and Zenvus Loci Harmony. We welcome intending new partners; email here to learn more. For intending partners, if we qualify you, we will send our price list.

Zenvus is a partner-first company. We have won many global awards on designs. In 2019, ZKM | Center for Art and Media Karlsruhe Germany displayed our works in their museum, recognizing “creativity and imagination”.

Zenvus Loci is a disposable or reusable package GPS that you can put in a briefcase, cargo, personnel, etc and monitor in real time its location. We see opportunities in tracking the specific cargoes (not just the trucks), ecommerce shipments, security guards, equipment on transit, law enforcement (police, army, etc), human (child, oil workers, etc), luggage (individuals shipping via buses, personal air travel luggage, etc), vehicles (no installation), etc. It is cheaper than anything in the market and it is rechargeable with USB. It has two versions: Zenvus Loci Mini and Zenvus Loci Max. Loci Max (up to 7 days of tracking, hourly reporting on full battery charge). Loci Mini (up to 3 days).

Zenvus mLoci: This works by tracking the phone of the driver using QR code and requires connectivity on the phone with GPS. The user (say a driver) must install the app. For every trip, a new QR code is generated. The driver scans it with his phone and clicks “begin trip”. That driver will be tracked until he clicks again in the app that ”trip is completed”. On a map, the driver location will be shown. Updates and notification via email and SMS. One code per trip sequence.

Zenvus Loci Harmony: Zenvus Loci Harmony is a solution for indoor property asset tracking. We will put a GSM- or WIFI- supported Zenvus receiver to pick location data from Zenvus chip stickers. You can have many of those stickers. Any device where you stick one (memos, files, phones, tables, chairs, TVs, bundle of cash, important assets, etc), and from our dashboard, you will know where it is. Each sticker has an 18-month battery life. Have Receivers and Tags(i.e. the trackers with beacons).

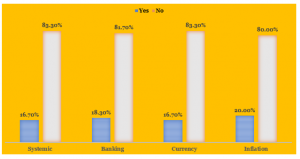

In every decade, the Nigerian banking sector does not experience less than two crises. According to experts, banking crisis evolves when two conditions emerge. The first condition is the significant signs of financial distress in the banking system such as bank runs, losses and liquidations must evolve. The second condition has been premised within the banking policy intervention measures in response to significant losses in the banking system.

Our analyst is interested in understanding these conditions further with special attention to the Nigeria’s data on crises in the banking industry from 1954 to 2014. During the period, existing data show that country experienced 11 systemic crises followed by 10 currency crises in addition 9 sovereign external debt defaults and 12 inflation crises, which could be described as a mixture of ups and downs for the economy. For instance, systemic crisis started from 1987 to 1994. It resurfaced between 2004 and 2005.

Exhibit 1: Category of Crisis between 1954 and 2014

Source: World Bank, 2014; Infoprations Analysis, 2020

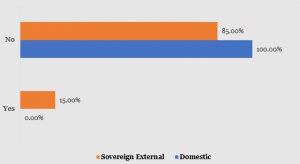

Exhibit 2: Debt Default between 1954 and 2014

Source: World Bank, 2014; Infoprations Analysis, 2020

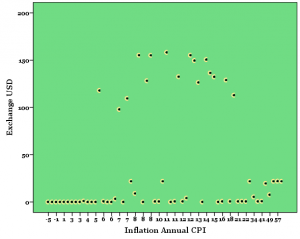

What Effect Do Exchange Rates Have on Nigeria’s Inflation Rates in 30 Years?

On a specific note, our analyst explored the impact of the exchange rate of US dollars on inflation annual (Consumer Price Index) rates in 30 years (out of the 60 years covered in the analysis), which in turn caused banking crises during the period. Analysis reveals -5.3% connection for the exchange rate and CPI. We also found that 0.3% of the fluctuation in the exchange rate could be understood from the CPI [see Exhibit 3].

These results align with the experts’ position that “When the exchange rate of its currency falls against multiple other currencies and the country imports goods from all these countries, the combined effect leads to economy-wide inflation in the country, even if its partner countries don’t raise their prices.” Going forward, our analysis suggests 21.8% increase in CPI for 2020 if the current exchange rate continues without adequate measures to checkmate it. Our analysis specifically indicates that one dollar increase in the exchange of Naira to Dollar would lead to a 21.8% increase in Inflation Annual CPI [see Exhibit 4].

Exhibit 3: Link between Exchange USD and Inflation Annual (Consumer Price Index) in 30 years

Source: World Bank, 2014; Infoprations Analysis, 2020

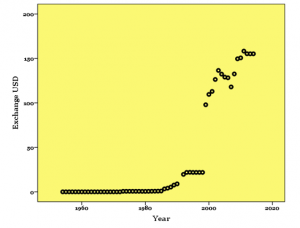

Bailout Sustainability and the Need for Stable Exchange Rates

Exhibit 4: Exchange USD per Year

Source: World Bank, 2014; Infoprations Analysis, 2020

According to our checks, during the period, government officials and experts agreed and disagreed on the rationales for bailout funds given to some banks. They also had divergent views on the policy interventions of the Central Bank of Nigeria and other regulatory authorities. In 2009, Lamido Sanusi, former governor of the CBN hinted that N620 billion was injected into the troubled banks due to non-performing and unsecured loans of the banks which led to tight credit in the economy. Checks have also shown that “Nigeria’s all-share index fell 2.5%, with financial stocks the heaviest losers after a 400 billion-naira ($2.6 billion) bailout of five banks knocked investor confidence in the sector.”

Having seen the gravity of unsecured loans and the cost of bailout on the government, in 2018 the Nigerian government through the Special Presidential Panel for the Recovery of Public Property announced its commitment to recover the $7 billion bailout fund granted to embattled commercial banks between 2006 and 2008 by the Federal Government. A year later, the Federal Government reinforced the need for the banks to revisit the risk management strategy because the use of huge bailout funds may not be sustainable in the financial system.

According to Professor Yemi Osibanjo, the Vice President, “First is the number of institutions, and implicit and explicit tools in our safety system and their sustainability. Perhaps the most significant challenge to the financial system that we have experienced so far was that bank crisis of 2009. “Going by the manner of resolution, it appears that the preferred option was the establishment of Asset Management Corporation of Nigeria – an option that cost something in the order of N5tn. Since then we have also seen the use of a mixture of bailouts and bridge banks.

“The problem, of course, is that the most reliable studies show that overly generous financial safety nets or system have generally tended to increase bank risks and systemic fragility. “My respectful view is that there must be some rethinking of the short and long- term implications of the use of these tools and their sustainability in the coming years. A reference was made in the past that we may not even have that option of the AMCON-type bailout given the sheer amount of money that will be involved.”

Beyond looking at the possibility of readdressing the bailout approach to rescue troubled banks, concerned stakeholders also need to devise the right policy interventions that would solve the exchange rate fluctuation in 2020 and coming years. This is imperative as the World Bank’s Global Economic Prospects report says, “There have been four waves of debt accumulation in the last 50 years. The latest wave, which started in 2010, has seen the largest, fastest, and most broad-based increase in debt among the four. While current low levels of interest rates mitigate some of the risks associated with high debt, previous waves of broad-based debt accumulation ended with widespread financial crises. Policy options to reduce the likelihood of crises and lessen their impact should they materialize include building resilient monetary and fiscal frameworks, instituting robust supervisory and regulatory regimes, and following transparent debt management practices.”

I wrote a few days ago that the World Bankshould allow the African Development Bank the freedom to run its playbook.

The African Development Bank (AfDB) which I hope empties its vault to help develop Africa rebuts World Bank whose president dropped those unfortunate lines: you have a tendency to lend too quickly and in the process, add to the continent’s debt problems. The World Bank president is wrong and he should be told that: AfDB is not adding to any problem.

Africa needs to incur debts over the next two decades to have any chance of advancement because its tax credits are so small to organically fund developments. Largely, the problem is not the debt BUT what the politicians do with the borrowed money. World Bank should focus on that second part, helping to ensure there is an improved governance.

We appreciate the World Bank; it wrote a cheque of US $20.2 billion for Africa in 2018. But that is nothing and at that rate, nothing will happen. Dangote raised close to $15 billion only for his empire a few years earlier. Time has come for respect and I expect the World Bank president to show that: AfDB is as important as the World Bank on this mission of developing Africa, and should be respected as it runs its own playbook!

But that does not mean Africa should not be concerned about the debt we are packing from China. I personally do not have much issues with AfDB, but I do have concerns when it comes to China. Yet, that does not mean that the World Bank should be the police. The reason we have China in African capitals is largely due to decades-long failures of IMF and World Bank, along with the African leaders, to fix the continent.

So when the World Bank president writes, “One of the practical problems we’re dealing with right now is some of the new lenders, the non-Paris Club lenders—and so I guess when we say that, people should sometimes read China into that.. They’ve escalated their lending, which is good in a way. We want more lending into developing countries. But…oftentimes their contracts have a nondisclosure clause that prohibits the World Bank or private sector from seeing what the terms of the contract are,” you will feel the pains arising from the disintermediation China is causing. But China did not get into Africa uninvited: the West created the vacuum which China is mining!

Both institutions [Word Bank and IMF] are also worried about the impact of China which, while still not the largest lender, has become a hugely influential source of capital in African countries that have few options due to their weak economic balance sheet. This is particularly true because China offers a convenient package of funding and execution through its state-owned enterprises for much-needed infrastructure projects across the continent. The problem, said World Bank president David Malpass, is the lack of transparency.

“One of the practical problems we’re dealing with right now is some of the new lenders, the non-Paris Club lenders—and so I guess when we say that, people should sometimes read China into that,” said Malpass. “They’ve escalated their lending, which is good in a way. We want more lending into developing countries. But…oftentimes their contracts have a nondisclosure clause that prohibits the World Bank or private sector from seeing what the terms of the contract are.”

The World Bank will not have any luck here as the politicians prefer the Chinese playbook, as less transparency breeds the spirit of corruption, which many of them hold multiple captain-ships. My only recommendation to the World Bank is thus: boost your private sector investment in Africa via IFC, your private investment arm, to $200 billion risk capital. If you do that over ten years, China may not have valuable things to fund. But if you stay around the current $20 billion yearly number, nothing will change. China gives cash and projects, most times, the World Bank gives lines of credits; African politicians prefer cash!

Carbon has set up a $100,000 Pan-African fund to address the lack of funding and support holding back budding tech entrepreneurs on the continent.

Carbon’s mission is to empower opportunity globally through frictionless finance. that empowers individuals and businesses with access to credit, simple payments solutions, high-yield investment opportunities and easy-to-use tools for personal financial management. We are a global company of over 100 employees with operations in Nigeria, England and Kenya.

Carbon’s Disrupt fund, the first of its kind by an African fintech startup, will invest up to $10,000 per startup (for 5 percent equity) and give access to Carbon’s API, allowing investees to leverage Carbon’s growing customer base and innovative technology platform, to get to market faster. Acknowledging that its success is dependent on the growth of the tech ecosystem, Carbon expects the initiative to spark more collaboration and further investment that should drive growth across the ecosystem. It’s not all altruistic, unfortunately!

Carbon is now accepting applications from companies with operations in Uganda, Kenya, Nigeria, Ghana, Cote d’Ivoire and Egypt. Startups looking to apply for the fund must have a functioning product, post revenue and looking to operate in multiple countries. The fund has a wide investment mandate but target sectors include insurance, health, education which have not seen as much investment as the fintech space.

More than 50 percent of startup funding on the continent in 2019 went to fintech firms1, despite the abundance of opportunities that exist in other sectors. Carbon’s Disrupt fund has been developed to tackle this head on, making it easier for entrepreneurs across all sectors to access the funds and support they need to establish their solutions and achieve their business objectives. The fund will also provide mentorship, access to Carbon’s customers and payment platform, as well as office space in Carbon’s Lagos offices.

According to Chijioke Dozie, CEO and co-founder of Carbon, “Common investor wisdom is to stay in your market and dominate. This assumes that you are expanding on your own but we believe that by collaborating and partnering deliberately, Carbon and other tech companies can scale faster and build more enduring platforms. There are many excellent companies across the continent looking for the kind of scale Nigeria offers and we are excited to partner with them to provide the support and financial investment they need. We are equally excited to expand beyond Nigeria and Kenya by working with a new generation of innovators across the continent and sharing our experience to tackle common obstacles to growth”

Ngozi Dozie, co-founder of Carbon, added “The investing environment for early stage startups has improved in recent years. However, a key issue for most startups that has not been addressed is the cost of customer acquisition. A lot of money is spent on acquiring customers, mainly via social media, when a more collaborative approach among tech companies could be more efficient. Our fund will enable this collaboration, allowing others to market to our customer base and vice versa – a win-win for everyone. As the saying goes, ‘if you want to go fast, go alone. If you want to go far, go together’”.

Since launching in 2016, Carbon has amassed 2.1 million users. The company disbursed more than $63.7 million in loans in 2019 and processed more than $140 million in transactions. In December 2019, the company announced its expansion into the Kenyan market, as well as its Carbon for Business platform which provides startups, small and medium-sized enterprises (SMEs) and FinTechs with access to uncollateralized credit, secure online payments, reliable funds transfer and fast KYC (know your customer) compliance obligations.

Interested entrepreneurs can apply to access the fund via https://getcarbon.co/disrupt-fund.